India has the reputation of being the “pharmacy to the world” and for good reason. Home to more US FDA-approved manufacturing sites than any other country outside America, India is a force to reckon with as far as the manufacture of generics and vaccines are concerned.

But there’s another powerful segment within the pharma sector that’s moving into the spotlight – Contract Research Organizations (CROs), Contract Development and Manufacturing Organizations (CDMOs), and Contract Research, Development and Manufacturing Organizations (CRDMOs).

Thanks to a combination of factors that include geopolitical shifts that have prompted client companies to look beyond China, and Indian companies emerging as trusted outsourcing partners, this sub-sector is expected to grow faster than the global CRDMO industry in the coming years. A recent report by Jefferies indicates that this could represent an opportunity to the tune of USD 700 million in sales per annum for Indian CRDMO players with the potential to reach USD 1.4 billion.

While this all hinges on a favourable policy framework being put in place and companies’ ability to scale up, what is clear is that investors can’t afford to ignore this space.

This pharma sub-sector leverages the same winning formula that made India a global outsourcing powerhouse – a skilled workforce combined with cost advantages. But things can get a lot more complicated with outsourcing in the pharmaceutical sector. In this two-part series we will understand the basics of the CRDMO industry, break down how it works and more importantly, look at how to play it as stock investors.

Molecules: Small vs. Large

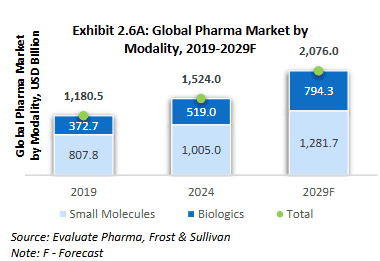

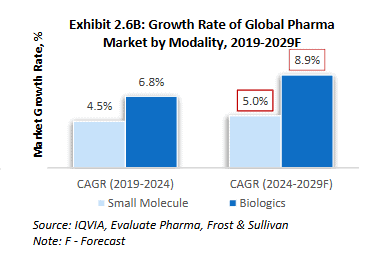

Pharmaceutical products are classified into two primary categories: small molecules and large molecules.

Small molecules: Small molecule drugs are low molecular weight organic compounds synthesized through chemical processes or extracted from natural sources. These drugs are usually administered orally. They are relatively easy to make and are stable, which means they are simple to handle in terms of packaging, storing and transporting.

Market potential: Small molecules represent the dominant segment of the pharmaceutical industry by volume, encompassing major therapeutic categories including analgesics (acetaminophen), antihistamines, anti-inflammatories (aspirin, ibuprofen), ACE inhibitors, antibiotics, and synthetic hormones. Their straightforward manufacturing processes and supply chain advantages make them the industry’s volume driver.

Source: RHP of Anthem Biosciences Limited

Large molecules: In contrast to small molecule drugs, large molecules or ‘biologics’ are complex and high molecular weight compounds. These are made from living cells or through biotechnology. These drugs need special manufacturing facilities and must be kept at specific temperatures during storage and shipping. They are typically administered through injections or infusions rather than via the oral route.

Biologics are more targeted than small molecule drugs and work particularly well for treating cancer. Apart from the very well-known example insulin, biologics include monoclonal antibodies (lab-engineered proteins to target specific antigens), recombinant proteins like insulin that replace or supplement naturally occurring proteins in the human body and enzyme replacement therapies to provide missing or deficient enzymes.

Because they are made in living cells, the manufacturing process is complex, they face challenges on replicating and is difficult to scale up consistently.

Market potential: While biologics make up a smaller portion of the overall drug market, they are growing much faster than traditional drugs. This growth is driven by their effectiveness in treating rare diseases, cancer, and autoimmune conditions. The trend is expected to accelerate over the next five years, with more biological drugs getting approved by regulators, indicating a major shift in how new medicines are developed.

Source: RHP of Anthem Biosciences Limited

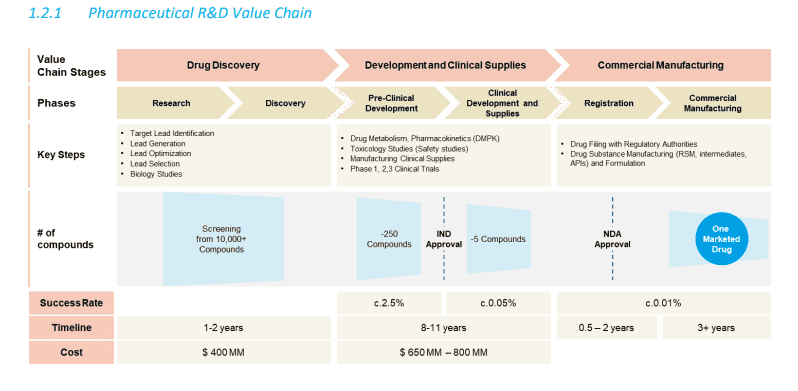

A Quick Look – Drug Development Life Cycle

Creating a new medicine takes a very long time and has many steps. Here’s how it works in the US:

Drug Discovery: This is where everything begins. Scientists look for new molecules that might help treat diseases. In order to do this, thousands of compounds are screened for therapeutic potential vis a vis a disease. They also figure out exactly what part of the body or disease they want to target.

Pre-clinical Testing: At this stage, the molecules identified are refined and optimised. They undergo laboratory (in vitro) and animal (in vivo) testing to assess safety, toxicity and initial efficacy. The outcome of this stage is critical for the application to the FDA to proceed to the human testing.

Clinical Testing: Once approval from the FDA has been obtained by submitting an ‘Investigational New Drug Application’, the molecule can be tested on humans and this happens in four stages:

Phase I: The medicine is tested in a very small group of healthy people (20 to 80 people) to assess safety, dosage range and how the drug is metabolised and excreted. This phase usually lasts up to a year.

Phase II: If Phase I goes well, the medicine is tested in more people (100 to 300) who actually have the disease it’s meant to treat. Here, the focus is on whether the medicine works and what the best dose is, while still watching for safety. This phase takes up to 2 years.

Phase III: This is the biggest and most important phase. The medicine is tested in hundreds to thousands of patients at many different sites for efficacy and adverse effects. It is also compared to placebos in this phase.

After all three phases are successful, companies submit either a “New Drug Application” (NDA) for regular medicines or a “Biologics License Application” (BLA) for biological medicines to the FDA. After a thorough review which can take 6 to 12 months or sometimes longer, if approved, the medicine can be sold.

Phase IV: Even after the medicine is commercialised, it is still monitored to assess efficacy and safety throughout its commercial life and this is known as Post-Market Safety Monitoring.

The whole process from discovering a new medicine to having it available in stores therefore takes 12 to 15 years, and sometimes even longer.

Innovator vs Generics

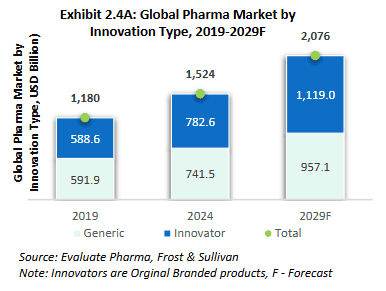

Another key distinction to note is that between innovator drugs and generic drugs.

Innovator drugs are the original versions of new medicines that are developed, approved and marketed. They are referred to as New Chemical Entities (NCE) in the case of small molecules or New Biological Entities (NBE) in the case of biologicals. These go through the extensive and stringent development and approval process before getting a patent approval.

Once approved, innovator drugs receive patent protection usually for 20 years (there are also avenues available to innovator companies to extend their exclusivity for limited periods of time in the US) from the filing date in the US. However, most of this time is spent on trials and regulatory requirements, leaving innovator companies with effectively around 7-10 years of exclusive sales to recover their research and development costs.

Generic drugs enter the market after patent protection expires for an innovator drug. These drugs contain the same active ingredients as the original and are equally safe and effective, but cost significantly less to produce since manufacturers don’t need to repeat the entire development exercise.

While generic drugs make up less than half of the pharmaceutical market by revenue, they dominate by volume due to their lower prices.

Source: RHP of Anthem Biosciences Limited

India market potential – why outsourcing is key

The above description goes to show that the drug discovery process until the point when it is commercialised is neither a simple nor straightforward one.

Addressing pain points

The following are some key pain points that an outsourcing partner addresses.

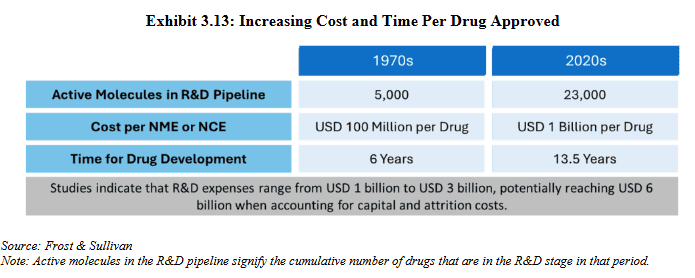

#1 Getting more expensive

The complex and lengthy process of drug discovery has become more capital intensive over the years. As the IPO documents of recently listed CRDMO players Anthem Biosciences Limited and Sai Lifesciences Limited indicate, the average cost to develop and commercialize a new drug today exceeds USD 1 billion, ten times what it was in the 1970s. More demanding research processes and increasing complexity of the drug candidates, have contributed to this.

Source: RHP of Anthem Biosciences Limited

#2 Success rates are slim

Only a very small percent of experimental drug candidates makes it from the lab to the market, after navigating the various stages in between. Estimates place this at one in 10,000 to 15,000 which means a success rate of sometimes less than 0.01%.

#3 Cost control in focus

Rising costs of R&D juxtaposed against slim success rates and limited years of exclusivity mean that R&D costs need to be optimised. Further, the upcoming patent cliff (with several innovator drugs going off patent over the coming years) will put pressure on margins for big pharma.

Regulatory requirements like the IRA (Inflation Reduction Act) introduced in 2022 that allows negotiation of some of the expensive drugs bought by the US national health insurance providers too curbs the pricing power of pharma companies. All of this reinforces the need for slimming down R&D costs.

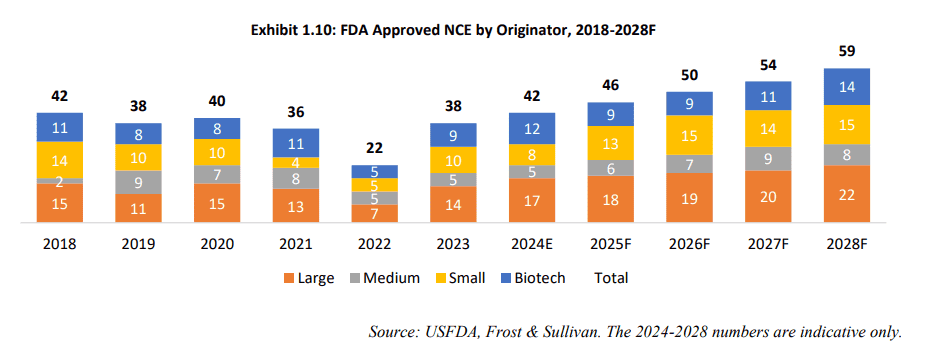

#4 More new drugs from small and biotech players

The global pharmaceutical market is dominated by large global pharmaceutical companies with revenues greater than USD 10 billion. But small pharma companies (with revenue lower than USD 500 million) and biotechnology companies (Biotechs) are growing at a rate faster than the large pharma players. These companies, especially biotechs, are usually startups focussed on developing new drugs.

The IPO documents of Sai Lifesciences Limited indicate a growing proportion of NCEs and NBEs originating from small pharma companies and biotechnology companies.

Source: RHP of Sai Lifesciences Limited

These companies generally have limited access to resources, infrastructure and may lack the breadth of experience needed to take a molecule from development to manufacture.

The shape and form of outsourcing

Outsourcing in the pharma sector is generally done by 3 types of players who cater to the innovator companies. The types of outsourcing partner can be mapped to the stage of the drug development lifecycle that they cater to.

Source: Frost and Sullivan Industry Report

- CROs are specialised companies that provide scientific research support across stages such as pre-clinical, clinical trials, data analysis etc.

- CDMOs focus on areas such as pre formulation and formulation development, API manufacture, commercial manufacture set up, packaging, quality assurance etc.

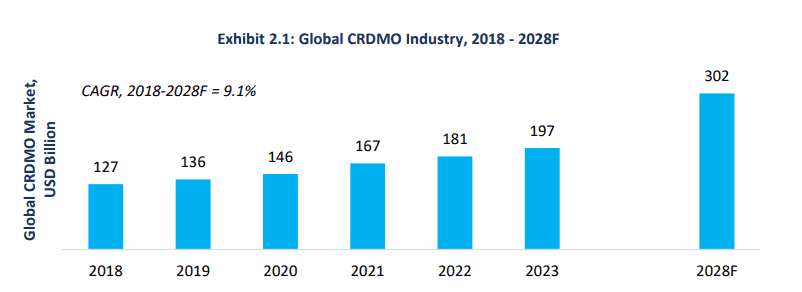

- While there are bound to be overlaps between what CROs and CDMOs offer, CRDMOs are integrated players that offer end-to-end services covering the entire drug development and manufacturing lifecycle. The services rendered by CROs and CDMOs are therefore essentially a subset of that offered by an integrated CRDMO player with the global CRDMO industry expected to grow at a CAGR of just under 10% till 2028 per this Frost & Sullivan industry report.

Source: Frost and Sullivan Industry Report

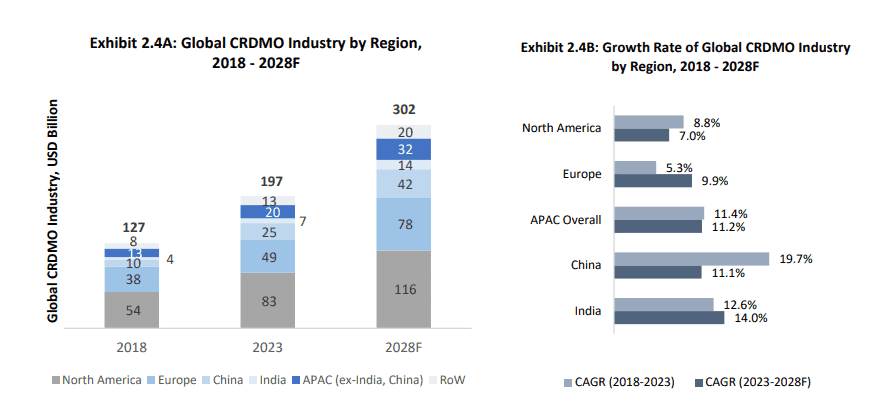

Where is the outsourcing going?

While geographically the industry is heavily skewed toward North America that is not only the largest consumer of the pharma industry but also the hub for innovation, the India and China CRDMO industries are growing at a faster clip than all of the others. This is thanks to the cost advantages, availability of skilled manpower and infrastructure.

Source: Frost and Sullivan Industry Report

While China dominates in API production, the India CRDMO space is expected to grow the fastest out of the APAC region thanks in part to the shift in geopolitical equations that has led to client companies looking for a China+1 option. The Biosecure Act in the US that prevents biotech firms receiving federal funding from using certain Chinese manufacturers could further accelerate the growth of the Indian CRDMO sector.

In part II we will take a look at the key CRDMO players in India, why it is not easy to pick a CRDMO player from an investor’s perspective, some of the new advancements in technology that will help set a CRDMO player apart, new opportunities coming up for the sector and most importantly how you as an investor can approach this space.

7 thoughts on “The CRDMO landscape in India: Part I – Understanding the lay of the land”

Madam,

When the part 2 of the series will be posted.

Thank you.

Hello Sir,

This will be in a couple of weeks.

Thanks,

Thanks for such a wonderful article in such simple language….I have a question- During entire drug development process of say 10-12 years, the crdmo/cdmo company will have a very low volume and revenue from a drug because only small batches will be needed during clinical trials and research. It is only when a drug gets approved and commercialized their volume/revenue will increase as now the drug can be administered to several patients…am i right in this?…in such a case how will we know which drug will be commercialised in say next few months and will this higher revenue continue for full 20 years till the drug is in patent…..Thanks in advance

Hello Sir,

Thank you for your comment. You are indeed right that in the early stages, contract values tend to be lower and become higher as the molecule progresses across the various stages. It is hard to know in advance which ones will get commercialised and which ones won’t. These contracts are also bound by confidentiality and this adds another element of complexity. We will be looking at these aspects in part II of the report.

Thanks,

Interesting! Thanks.

One observation, Samsung Biologics Co Ltd KRX: 207940 in this business has been multi bagger in last decade but isn’t there an equivalent growth engine in india ?

Hello Sir,

We will be getting into this in part II of the series.

Thank you.