Few sectors generate as much consensus optimism as Indian residential real estate — and few have a longer track record of disappointing investors who arrived late to the cycle. The tailwinds are genuine: demographics, urbanisation, and income growth provide a multi-decade demand runway. But the sector is cyclical, capital-intensive, and prone to periods where even the right long-term call produces the wrong short-term outcome. This note examines the market dynamics, the key risks, and three listed developers through that lens.

Market Structure & Current Dynamics

India’s real estate sector is currently a significant contributor to GDP and is projected to account for 14–20% of the economy by 2047, implying a market value of ~$6 trillion (Source: NDTV/Knight Frank). Listed developers are expected to capture a meaningful share of this growth, though the path is not without risk.

Segment Trends

The residential market is segmented into affordable, mid-segment, and luxury/premium. Mumbai leads in unit launches, followed by Bengaluru and Pune.

Mid-segment is the largest by volume, but is facing headwinds. Growth is slowing due to a combination of supply-side pressure and softer demand, particularly from the IT sector where AI-driven job uncertainty is dampening buyer sentiment.

The premium/luxury segment is absorbing demand that has shifted upward for two reasons:

- Post-pandemic preference shifts towards larger homes with amenities (gyms, pools, co-working spaces), and work-from home -driven need for dedicated office space.

- Elevated land prices and construction cost inflation (driven by pandemic-era supply shocks) have squeezed developer margins in affordable housing, pushing developers to focus on premium projects where margins are more sustainable. (Source: FRED — BIS residential property price data)

Geographic Expansion

New launches are concentrating in peripheral micro-markets — New Dwarka Expressway and New Gurgaon in Delhi NCR, extended eastern suburbs in Mumbai. This is being enabled by government investment in connectivity: highways, suburban rail, new airports. The result is a ring of satellite cities and integrated townships around existing metros.

Demand Drivers

These are the structural factors underpinning medium-to-long-term residential demand. Each comes with caveats.

Urbanisation

India’s urbanisation rate stands at 36%. By 2050, an estimated 950 million people will live in urban areas, requiring accommodation for an additional ~470 million people. (Source: Reuters/World Bank, July 2025)

To illustrate the scale: listed developers currently launch approximately 400,000 units per year. Over 25 years, that totals ~10 million units, housing roughly 40 million people — less than 10% of projected urban migration. This structural undersupply creates a long runway for development activity, though it also raises questions about affordability and which market segments will actually be served.

Demographics

India’s median age is 28.8. As this cohort ages into typical homebuying years (30s–40s), demand for first homes and upgrades should rise. Separately, the proportion of nuclear households has increased from 56% (2016) to 58.2% (2020) (Source: Policy Circle), requiring more units per capita.

Income & Affordability

India’s GDP per capita is ~USD 2,000, at a threshold associated with rising consumer spending. As incomes grow, so does access to home loans. However, affordability is already strained in metro markets. Rising land and input costs have pushed prices up faster than incomes in some segments. This tension is more acute in the affordable housing space than in premium.

Regulatory & Infrastructure Support

The government’s infrastructure push — metros, sea links, expressways, suburban rail — is enabling the geographic expansion of Indian cities. The industry has also sought tax relief, including an increase in home loan interest deduction under Section 24(b) of the IT Act (currently capped at ₹2 lakh for old regime taxpayers) and restoration of the Section 80-IBA housing tax holiday. (Source: Moneycontrol/NAREDCO)

Key Challenges

Macroeconomic & Interest Rate Risk

If sustained growth prompts inflationary pressure, the RBI may raise rates. Higher mortgage costs directly reduce affordability and dampen transaction volumes. Developers with high debt levels would face compressing interest coverage.

Affordable Housing Gap

Urban affordable housing remains in structural short supply. Developers have largely exited the segment due to thin margins. This gap widens as land and construction costs rise. As seen in markets like New York, once housing affordability becomes a political issue, policy fixes are slow and often create their own distortions.

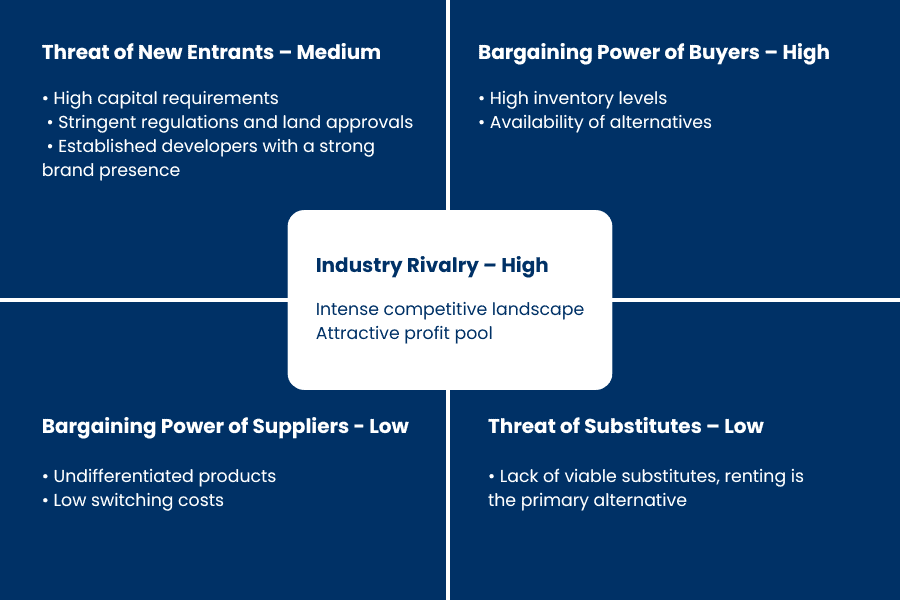

Competitive Intensity

Multiple large developers are competing in the same micro-markets, particularly in premium MMR, NCR, and Bengaluru. This concentrates supply in the same geographies and price points, giving buyers more negotiating power and compressing developer margins. Pricing discipline can be hard to maintain in a land-intensive, capital-locked business.

Market Downturn Risk

Real estate is inherently cyclical. Downturns lead to inventory buildup, falling realisations, and weakening buyer confidence. The Evergrande collapse in China provides an extreme case study of what over-leveraged developers can face when sentiment turns. India’s listed developers have strengthened their balance sheets, but the risk of a demand slowdown remains, particularly if job markets weaken.

ESG & Sustainability

Construction has a significant environmental footprint — energy, water, carbon, and waste. Most existing Indian residential stock was not built to energy-efficiency standards. As regulatory and investor scrutiny increases, retrofitting older assets and meeting green certification standards will add cost for developers.

Company Profiles

Three companies were shortlisted from the broader universe using the following quantitative criteria: minimum 15% revenue growth, 10% ROE and ROCE, PEG below 1.5, and a debt-to-equity ratio below

Godrej Properties

Godrej Properties is India’s largest listed developer by sales booking value (Rs 34,171 Cr). The company operates across all segments with a stated strategic focus on premium. It has developed 76 msf so far and has 84 msf currently under development.

A closer look at the financials reveals that reported profitability has been substantially supported by other income, primarily interest income and fair value gains. Excluding these items, the company reported losses across the last four years. This is a meaningful distinction for evaluating underlying operating performance.

Revenue recognition follows the project completion method, meaning revenue is booked only on receipt of an occupancy certificate. This creates lumpy revenues that may not reflect the pace of construction activity or collections. The company primarily acquires land outright rather than through joint development, which ties up more capital.

Oberoi Realty

Oberoi Realty is concentrated in MMR — primarily Mulund West, Goregaon East, and Thane — with a focus on premium and luxury residential projects and select mid-segment developments in the eastern suburbs. The company also holds rental-yielding commercial assets: Oberoi Mall and Sky City Mall, plus office spaces. It explicitly prioritises margin over market share.

Development Portfolio

Recent Financials

Revenue declined sequentially from ₹1,779 crore (Q2 FY26) to ₹1,493 crore (Q3 FY26), though it was up year-on-year from ₹1,411 crore in Q3 FY25. Profit fell from ₹760 crore in Q2 FY26 to ₹623 crore in Q3 FY26; on a YoY basis, it rose marginally from ₹618 crore. The company follows the percentage-of-completion method; upcoming completion milestones on projects like Jardin (Tower B) and Forrestville (Towers B & C) are expected to drive revenue recognition in coming quarters.

The company operates an asset-light model, employing architects and subcontractors rather than owning heavy construction capacity. It targets a minimum 20% ROE. Oberoi’s township model — integrating residential towers with schools, malls, and offices — supports pricing power in its target market. Total development potential stands at 34.4 msf across core and peripheral MMR, including planned developments in Worli (residential), Nepean Road, Borivali, Alibaug, Thane, and a luxury project in Gurgaon.

Lodha Developers

Lodha has delivered 60 msf to customers across Mumbai and Pune and is expanding into Bengaluru and Gurgaon. It holds a 10% market share in Mumbai and is the 3rd largest developer in Pune.

Recent Financials

Revenue increased sequentially from ₹3,879 crore (Q2 FY26) to ₹4,775 crore (Q3 FY26), and rose year-on-year from ₹4,147 crore in Q3 FY25. Profit was ₹958 crore in Q3 FY26, up from ₹945 crore in the same quarter last year. Pre-sales in Q3 FY26 reached ₹562 crore.

Revenue recognition policy is split: contracts signed on or before 31 March 2023 follow the project completion method; contracts from 1 April 2023 use percentage of completion. This creates a transitional hybrid that warrants attention when reading reported numbers.

The company’s balance sheet has improved materially — debt-to-equity fell from 4.36x in FY21 to 0.36x in FY25. Strategy prioritises joint development (JDA/JV) in core Mumbai and Bengaluru locations, with 19.9 msf under joint development and a target of 40% pre-sales through this route. Commercial diversification targets ₹1,500 crore in rental income by FY2031 across office, retail, and logistics. The company also holds a 400-acre land bank earmarked for data centres, with approvals in place.

Concerns

• Equity dilution: A QIP in March 2024 raised ₹3,290 crore; the board has since approved a further ₹6,000 crore raise. While proceeds have partially been used for deleveraging, repeated equity raises are uncommon among peers and signal ongoing capital intensity. They raise cost of capital over time.

• Short-term borrowings: The company carries a significant level of short-term debt, and the timing of inventory-to-cash conversion may not always align with repayment schedules.

• Governance: An executive director was found to have misused their position for personal land dealings at the company’s expense. A police complaint has been filed. While the company disclosed the incident, governance risk of this nature warrants ongoing attention.

• RERA compliance: The company altered a development plan after RERA approval without informing homebuyers, drawing regulatory complaints. This is a material issue given buyer protections are a cornerstone of the post-RERA framework.

Summary

India’s residential real estate sector has structural tailwinds — urbanisation, demographics, income growth — that are real and measurable. Equally real are the structural constraints: an affordable housing gap that is widening, competitive intensity in premium micro-markets, and governance risk that has surfaced even among listed players. The demand story is not uniform across segments.

Among the three profiled developers, Oberoi Realty stands out for balance sheet discipline and consistent margin delivery, though its MMR concentration limits geographic diversification. Godrej’s reported profitability has been heavily supported by non-operating income. Lodha has made significant progress on deleveraging but faces governance questions and balance sheet risks that require monitoring.

Investors should look through the headline pre-sales numbers to cash generation, debt profile, revenue recognition methodology, and governance track record before drawing conclusions.

The Cyclicality Caveat

The more fundamental caution is sectoral. Real estate is a cyclical industry, and the risks of a downturn do not appear at the moment of reversal — they build during the up-cycle. Key leading indicators to watch:

- Rising unsold inventory levels across micro-markets

- Softening absorption rates, particularly in mid-segment

- Stretched developer balance sheets relative to cash conversion timelines

- Weakening demand from IT-sector employees, who drive a disproportionate share of premium residential demand

By the time a downturn is visible in reported numbers whether revenues, margins or pre-sales — the damage to valuations is often already done. The factors that make the current cycle look attractive (high pre-sales velocity, pricing power, margin expansion) can reverse quickly.

Secular Theme, Cyclical Risk

Urbanisation and demographics are genuine long-run drivers. But a secular theme playing out over decades does not prevent a multi-year period of weak returns or capital destruction within that arc. The distinction matters:

- Long-term demand does not guarantee short-to-medium-term returns

- Entry and exit timing in a capital-intensive, illiquid sector can be as consequential as stock selection

- Buying at peak-cycle valuations, or holding through a downturn without the liquidity to average down, can destroy wealth even when the thirty-year thesis remains intact

- Unlike equities, real estate corrections tend to be drawn out — prices are sticky downward, volumes collapse first, and recovery can take years

What to Look At

- Cash generation vs. reported profit — revenue recognition methods (completion vs. percentage of completion) can significantly distort reported earnings

- Debt profile and short-term borrowing relative to inventory conversion timelines

- Leading indicators of cycle health: unsold inventory, new launch volumes, absorption rates

- Where current valuations sit relative to historical cycle peaks

- Governance track record — RERA compliance, related-party transactions, capital allocation discipline

The stocks mentioned above are for informational purposes only and should not be construed as recommendations.