In the consumption space, consumer durables are a natural sector to spot opportunities. However, the tale of the durables sector is more a cyclical play than a stable growth trend. A cooler summer, delayed monsoon, a tweak in regulations, spike in copper prices all affect the demand scenario for durables such as air conditioners, fans and refrigerators.

This sensitivity to weather and discretionary spending has played out in the past two years, reflecting in earnings for durables players and in their stock market prices. However, as companies work through their inventory overhang now and as the demand environment is shaping up well for this summer, it may be time to look at this sector once more.

In this report, we take a detailed look at the recent earnings performance of key consumer durables and electricals companies, the factors currently shaping demand and margins, and how investors may approach opportunities within the sector.

Demand fluctuations

In the listed space, the majority players are in cooling products such as air conditioners, fans, and refrigerators. The primary season for these is the summer. A harsh summer in Apr-Jun 2024 saw strong sales growth for consumer durables companies, ranging from 14% to as high as 33%, for the Apr-Sep 2024 period.

Buoyed by this momentum, most leading brands built aggressive inventory positions ahead of the Apr-Jun 2025 season as well. However, the summer proved far weaker than anticipated. Extended monsoons and cooler temperatures across several regions dampened demand, resulting in inventory offtake well below expectations. Consequently, the April-September 2025 earnings performance was muted, with most companies posting low single-digit sales growth or even a fall.

For example, Voltas saw declines as steep as 17%. Consumer electricals players such as Crompton Greaves Consumer Electricals, V-Guard Industries, Bajaj Electricals and Orient Electric witnessed a similar, albeit less severe, trend. While these companies posted a median sales growth of 11% in H1 FY25, growth decelerated to a median of -1% in H1 FY26.

This apart, regulatory moves temporarily squeezed demand. In August 2025, the government announced GST 2.0, reducing the tax rate on consumer durables from 28% to 18%. This translated into a 7.8% price reduction—an air conditioner previously priced at ₹35,000, for instance, became available at ₹32,366. Consumers thus deferred purchases until the new rates took effect in September 2025.

This apart, channel inventory from the weak summer season left companies and distribution channels with higher-than-usual stock levels by the end of the September 2025 quarter. Both together weighed on sales.

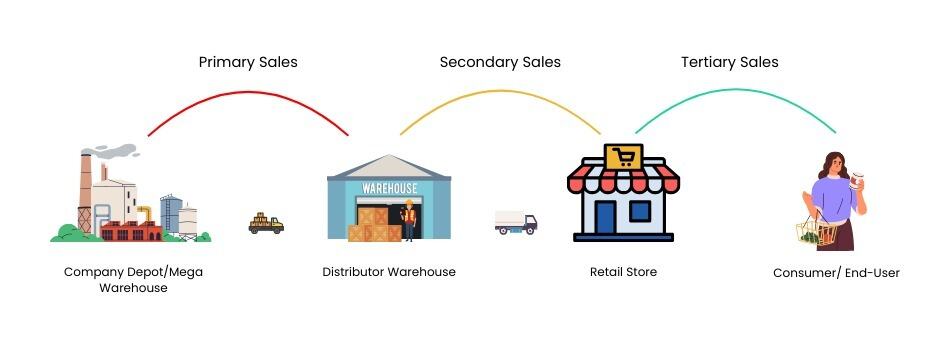

Why is understanding channel inventory important?

Understanding channel inventory for consumer goods companies is critical because it helps determine whether reported revenues are backed by genuine consumer demand or simply reflect inventory being pushed into the distribution system. For consumer brands, success lies in ensuring products reach customers at the right place and time through a well-managed supply chain.

Let us take Voltas as an example to understand this journey.

Primary sales: After manufacturing, air conditioners are stored in the company’s warehouses and recorded as inventory on its balance sheet. Primary sales occur when the company sells these units in bulk to regional distributors, channel partners, modern trade or e-commerce partners. Revenue is recognized by Voltas at this stage, irrespective of whether the product is ultimately purchased by the end consumer.

Secondary sales: This represents the movement of goods from regional distributors to retailers such as Aditya Vision, Electronics Mart, or Vasanth & Co, as well as replenishment of inventory by online platforms.

Tertiary sales: This is the final sell-through to end consumers, when a customer purchases the AC from a physical retail store or places an order on an online marketplace. Tertiary sales reflect the actual consumer demand.

Therefore, strong primary sales do not necessarily imply healthy end consumer demand. Companies can push excess inventory into the channel by offering higher trade discounts. If consumer offtake (tertiary sales) does not match this supply, intermediaries are left holding elevated stock. This leads to lower primary sales in subsequent periods and forces brands to introduce promotions, cashback schemes or price cuts to liquidate inventory, putting pressure on margins.

While investors can track primary sales from reported revenues, secondary and tertiary data are far less transparent. Hence, management commentary on channel inventory, dealer checks and signals around seasonality become essential to judge the true demand environment.

Current earnings picture

Elevated channel inventory and muted demand in cooling categories weighed on the industry’s overall growth trajectory during the December quarter quarter. Performance across companies was largely shaped by their product portfolio mix.

Appliances like air conditioners, fans and refrigerators remained subdued, with Q3 being seasonally weak for these categories. On the other hand, players like Crompton Greaves, V-Guard, and Orient Electric reported reasonable growth, driven by their exposure to heating products. Havells also delivered strong revenue growth and margin expansion, led by a robust 33% increase in its cables segment. Here’s a glimpse into Q3 FY26 performance of different companies:

The earnings picture and management commentary indicate a few trends:

#1 High Inventory Overhang in Q2

The industry entered the third quarter facing elevated stock levels in its books and its channel; as explained above, this comes from the weak summer of 2025 where companies failed to liquidate the aggressive inventory positions built up earlier in the year. For example, by September 2025, Blue Star reported channel inventory levels as high as 65 days, well above their target 45-day cycle.

The elevated inventory levels for consumer durables players is illustrated in the chart below:

As a result, brands prioritised destocking and improving channel hygiene during the December 2025 quarter. Bajaj Electricals was particularly aggressive, reporting a 25% revenue decline in consumer products as it deliberately reduced dealer inventory. Voltas, Havells and Blue Star also worked closely with dealers and stepped up support through enhanced sell-out schemes and consumer financing initiatives.

Retailers also leveraged attractive OEM discounts and promotional schemes offered to liquidate older models. For example, Aditya Vision deliberately built higher inventory levels of room air conditioners at lower pre-BEE transition prices to position themselves competitively for the upcoming 2026 summer season.

Most companies now expect the legacy stock in channels to be largely cleared by March 2026. As we approach summer of 2026, brands are preparing to refill the channel and intend to hold higher-than-usual inventory levels to capitalise on peak demand.

#2 Price Hikes

One of the key trends visible across brands is the round of price hikes already undertaken or lined up for the March 2026 quarter owing to revision in energy efficiency norms and input cost inflation. Among room AC players, Blue Star indicated a 10% increase during Q4, while Voltas plans to make calibrated hikes in the range of 5-15%, dynamically with new-table product rollouts.

Within the consumer electricals segment, Bajaj Electricals guided for increases of 2-5% starting February. Crompton Greaves had already implemented a 1-1.5% hike in January and signalled further revisions across Q4 and Q1. Orient Electric is raising fan prices by 3-3.5%, with additional hikes, if commodity prices stay elevated.

The key exception is LG Electronics and Havells. Their management commentary suggests that while headline price increases of 5-10% may be required, the benefit of GST reductions is expected to offset the impact, resulting in minimal effective change for end consumers.

The sharper-than-normal price revisions can largely be attributed to two key factors:

Shift in BEE Ratings norms: The Bureau of Energy Efficiency (BEE) is set to implement stricter star-rating norms for air conditioners and ceiling fans effective 1 January 2026. Under the revised framework, rating thresholds are being tightened, meaning a 5-star product under the old system would now be rated as 4-star (a 4-star would become 3-star and so on), even if the underlying product specifications remain unchanged.

To comply with the new norms, manufacturers will need to incorporate higher-efficiency compressors, motors, and heat-exchange systems. This will increase production costs, which will largely be passed on through price hikes; the price increase is expected to be higher for 5-star models compared to lower-rated products.

Manufacture of products compliant with the old BEE norms will not be permitted from January 2026. Manufacturers will only be allowed to supply existing inventory up to March 2026, and retailers can continue selling such inventory up to June 2026. In addition, star labelling which was previously voluntary for products such as refrigerators, televisions, LPG gas stoves, grid-connected solar inverters etc has now been made mandatory.

Commodity price inflation and Rupee depreciation: Copper and aluminium remain the key raw materials for the consumer durables industry, and their LME prices have risen sharply by 44% and 17%, respectively, during 2025. In addition, given the sector’s dependence on imported components, the rupee depreciation during 2025 further inflated input costs. For instance, LG Electronics India Ltd. sourced nearly 46% of its raw materials from outside India in FY25 (as per its DRHP).

In ceiling fans, price hikes in induction motor variants will be higher than in BLDC fans due to the higher copper content in induction models. Wires are also directly exposed to copper price volatility. The effect of commodity inflation and rupee depreciation is visible in the form of lower EBITDA margins reported by companies during 9M FY26, reflecting margin compression ahead of full pricing pass-through.

Looking ahead

These swings in demand and input pressures led to subdued market performance by durables stocks. During 2024, the median stock price rally of the durables pack was 31%. Stocks such as Voltas, Blue Star, and V-Guard rose 83%, 126%, and 45% respectively.

This was followed by a sharp sell-off on disappointing earnings. 2025 saw a median decline of 24%, with stocks like Whirlpool of India, Bajaj Electricals, and Crompton Greaves falling 51%, 38%, and 36% respectively.

With the inventory overhang now gradually normalizing, consumer durables players are resetting for the upcoming season. This is supported by expectations of improved demand and a stronger upcoming summer season. In the first two months of 2026, Voltas and Blue Star have risen 6% and 8%, suggesting that markets have begun factoring in a positive picture.

There are a few factors that indicate a strong demand scenario:

- Climate projections from Skymet Weather Services indicate early signs of a potential El Niño developing in the second half of 2026. An evolving El Niño typically delays the onset of the monsoon and disrupts its spatial and temporal distribution, often resulting in extended heat waves. This can boost demand for cooling products like room air conditioners and fans.

- The growth outlook is also supported by low penetration levels across product categories at around 13% for room air conditioners, 22% for washing machines, 35% for refrigerators, and 78% for televisions. Compared to global levels, there is substantial headroom for growth across these segments.

- Premiumisation trends continue for both large and small home appliances as consumers are increasingly upgrading to products like energy-efficient air conditioners, inverter technology models, BLDC motor fans and other feature-rich appliances.

The India Appliances & Electronics market (excluding mobile phones) is projected to grow at a CAGR of 14%, expanding from ₹3,245 bn in CY2025 to ₹6,190 bn by CY2029 (Source: LG Electronics DRHP). Confidence in the sector’s long term growth prospects is reflected in the plans announced by companies for new product launches, capacity expansion and backward integration:

- LG Electronics has plans to increase its AC compressor manufacturing facility from 1 million units to 3 million units by January 2027. They’ve also planned to double their capacities in ACs, washing machines and refrigerators by FY29. Overall capex outlay is around ₹5,000 Crs.

- Voltas is ramping up its recently-commissioned backward integrated Chennai facility, with plans to increase RAC manufacturing capacity from 1 million units to 1.5 million units and subsequently to 2 million units.

- Havells has earmarked ₹1,000 Cr in FY27 towards capacity expansion in cables and setting up of a new R&D centre.

- Bajaj Electricals announced the launch of wires this month, following its recent diversification into switchgear (Q2) and solar solutions (Q3), indicating a broader play across adjacencies.

- Crompton Greaves announced its entry into the residential wires segment, with a launch expected in the next six weeks across select markets, as part of its strategy to expand its addressable market.

- V-Guard has planned capex of ₹250 Crs over FY26 & FY27 for fan manufacturing facility and the second battery facility, to increase the share of its inhouse manufacturing.

How to play the sector

While the sector’s structural growth drivers remain intact, demand tends to be cyclical and largely influenced by strength of the summer season. As a result, the sector is best approached with a cyclical perspective. In addition, any further increase in commodity input prices owing to the West Asia conflict could lead to margin pressure or impact volumes.

Therefore, when evaluating companies in the sector, consider the following key factors during stock selection:

- Product portfolio – Companies with a more diversified product mix across categories are relatively less exposed to seasonality in demand.

- Household penetration – Categories with low household penetration, such as air conditioners, offer a larger runway for long-term growth.

- Market share and competitive positioning – Current market share in core categories and the company’s ability to expand it through product differentiation, advanced features, and premiumisation.

- Manufacturing strategy and backward integration – Companies with higher in-house manufacturing typically enjoy better margins than those relying on outsourced production. Current and planned backward integration of key components (like. AC compressors) can further improve margins and reduce external dependence.

- Distribution strength and brand recall – Depth of dealer network, efficiency of own and channel inventory management, and overall consumer perception of the brand.

On the valuation front, similar to other consumer-facing companies, durables and electricals players trade at relatively high P/E multiples. Depending on the product categories and market share, valuations typically range between 35–70x earnings. It’s important to note, however, that current P/E multiples may appear higher due to the depressed earnings cycle.

Another way to play the sector is through retailers such as Aditya Vision and Electronics Mart India who offer a relatively cleaner play on underlying industry growth without directly competing for product market share.