N V Chandrachoodamani & Vidya Bala

As equity investors, we wish for certainty and high linear returns that beat every other asset class. But this happens only in a few good years — the remaining periods carry some or other uncertainty and volatility. The journey can never be black or white. It will always be under the shades of grey.

The Returns Are in the Timing — and the Staying Power

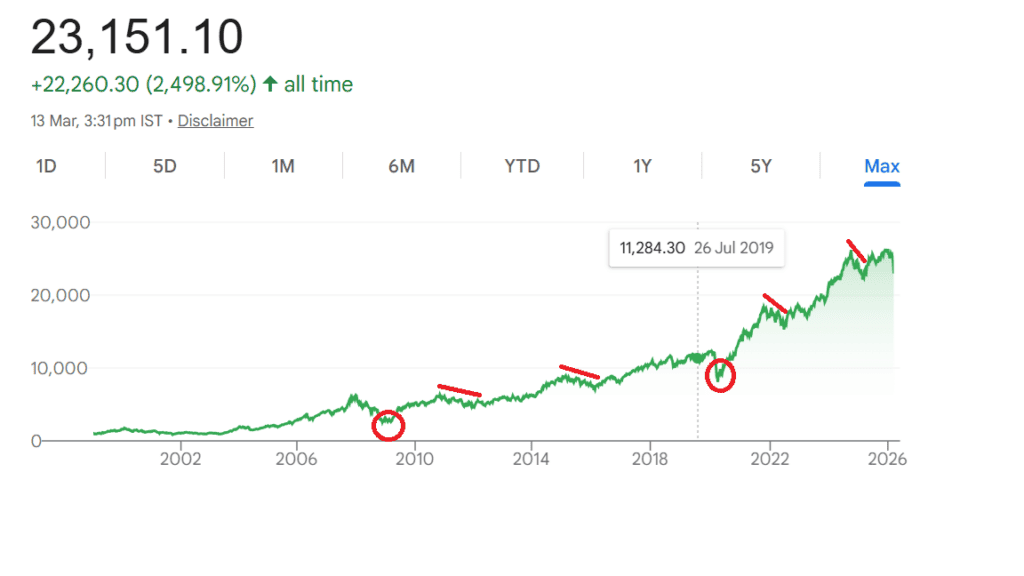

Consider the Nifty 50 over the last five years. An investor who entered in March 2021 and stayed through to March 2026 would have earned 54% in absolute terms, or approximately 9% CAGR. Had the same investor delayed entry by six or seven months to October 2021, those returns would have shrunk to 26% absolute and around 5.3% CAGR over 4.5 years. And only those who had the courage to invest a year earlier, in 2020, amid the extreme uncertainty of Covid, captured the full 15–20% equity premiums that equities are expected to deliver.

Source: Google

The lesson is not merely about entry timing — it is about behaviour during crises. Over the past five years, the market has navigated the Russia–Ukraine war, multiple general elections, and the US tariff saga, and there was sufficient panic around each of these events. Investors who stayed invested but utilised the sharp dips as opportunities would have meaningfully outperformed those who simply sat on their positions. This calls for a clear playbook: stay in the game, buy the dips with calculated conviction rather than fleeing in fear or allocating too much, too early.

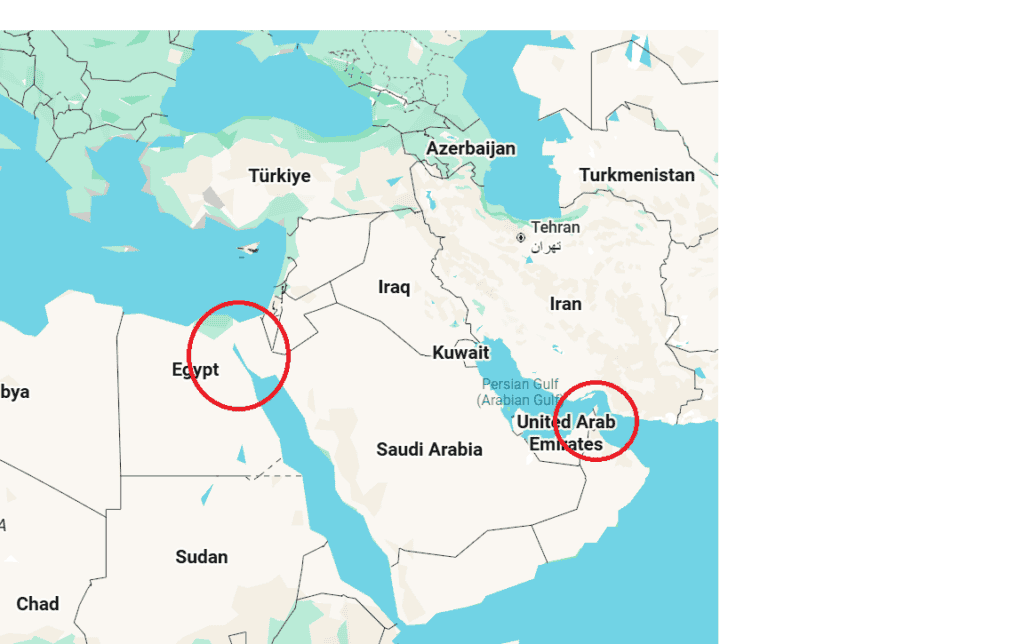

The Current Situation: US–Israel–Iran and the Strait of Hormuz

As it stands today, we are in the midst of another such uncertainty — the US–Israel–Iran conflict. The week just passed was one of panic and chaos, not just for equity investors but for common people as well. The Strait of Hormuz has become the talking point, and understandably so. The Gulf region has two critical narrow shipping routes that are vital to oil trade and general goods: the Strait of Hormuz and the Suez Canal (the latter was the site of the ship called Ever Given stranding not long ago). These are the arteries of global commerce.

Having said that, the world lived through a period of near-zero disruption for decades after the Gulf War — an era of flourishing trade, globalisation, and shared prosperity. The geopolitical tensions of the last few years are disturbing in the sense that major economies are now erecting significant tariff and non-tariff barriers to assert control over critical manufacturing sectors — defence, automobiles, pharmaceuticals, and electronics — and to strengthen their military posture. In other words, large nations are building strength for future conflicts.

What this means for equity investors is that the investing environment need not be “friction-less” as it was in past decades. But that does not diminish the prospects of earning great returns from equities. We do not need to guess when the war ends — what matters is understanding the order of impact on markets and developing a rational playbook.

(we already discussed various scenarios of the War and its impact in this article earlier)

Is It Different This Time? Probably Not

When crisis events of this nature break out, sell-offs tend to follow a recognisable sequence. This was true during the Russia–Ukraine war in 2022, and it is no different now. There are four distinct waves:

- Sensitive sectors sell first. One, companies directly exposed to the conflict zone. L&T, with its mammoth Middle East order book, and Voltas are examples of companies operating in or dealing directly with the conflict zone. Two,those with heavy dependence on crude-linked inputs — aviation, paints, tyres, and similar businesses. These face the most immediate profitability pressure.

- Second-order macro effects follow. Beyond a point, the broader macro equation is disrupted — interest rates, currency, and the trade balance all come under pressure, reversing earlier market assumptions. If NBFCs were rallying ahead of banks in anticipation of rate cuts, that thesis may be reversed in the market now. Sectors that benefited from a low-interest-rate environment get repriced. That is the sell-off you are seeing in such segments now.

- Small caps come under broad-based selling pressure. As investors flee to the safety of large-cap and established names, buying in the small-cap universe dries up. In bad times, the mere absence of buyers is sufficient to pull down stock prices sharply, and small caps are the most common victims of this dynamic.

- Defensive sectors receive the flows. Consumer staples, pharmaceuticals, and technology (although it is under pressure now for a different reason) typically serve as shelters. Occasionally, unexpected names join the sell-off list — Eternal, for instance, saw selling due to restaurant footfall concerns (delivery and dine-out drop due to fear-driven LPG demand), which is more a deferment of demand than any structural change in the business. Next time a similar crisis unfolds, Eternal may well join aviation and paints as a standard item in the sell-off template.

It is also worth reminding ourselves that the disruption right now is less about the war itself and more about the fear around vessel movement through the Strait of Hormuz. It is a disruption that is waiting to be solved by every stakeholder. Iran still needs to pump and sell oil — it is one of its primary economic lifelines. Even the rest of the Middle East has a strong economic incentive to see the US bring this conflict to a close. And the Russia–Ukraine war provides a relevant precedent: equity markets, including those in the EU that were most directly affected, largely detached from that ongoing conflict as the months passed.

The Investors’ Playbook

For equity investors, these sharp dips are precisely the moments that determine long-term returns. The important constraint to keep in mind is that there is a finite amount of capital available — how that capital is deployed now will determine the success rate. What follows is a template for thinking through the current opportunity, sector by sector.

(Please note: the examples below are for illustration only and should not be construed as investment recommendations. We may or may not hold positions in the stocks or sectors discussed.)

#1 Sensitive Sectors: Steer Clear vs. Hunt Selectively

For most individual investors, the first instinct in a crisis should be to avoid direct exposure to the most sensitive sectors — businesses deeply exposed to the conflict zone or those with heavy crude and energy dependence, especially where leverage is high and pricing power is weak. This group includes aviation, paints, tyres, and the second-order suspects such as cement, polymer processors, and tile and ceramic manufacturers. For retail investors and those who invest through mutual funds, it is best to stick to diversified funds rather than trying to time sectors unless you know the impact of this crisis on each sector.

For fund managers like us, however, these very pockets can throw up compelling opportunities. The lens through which we evaluate them:

- Aviation: A dominant carrier operating at 10% EBITDA margins is inherently sensitive to oil prices and load factors. In the current scenario, travel demand itself may dip, compounding the sensitivity. A debt-laden carrier in this environment should be avoided. But a cash-rich, dominant player is a different story — if this shock passes in three to six quarters, as most geopolitical episodes do, it may represent a meaningful entry point.

- Tyres and Polymer Processors: A tyre manufacturer or polymer processor with zero or manageable debt, and the ability to pass through input cost increases, can actually be an attractive buy in this kind of crisis. The input spike, if it materialises, is likely to be temporary; what matters is whether the business can sustain itself through it.

- Direct exposure: A company with a significant Middle East order book is exposed, but for a business like L&T, the valuation contribution from its IT subsidiaries provides a meaningful buffer. The sensitivity to the conflict may be no more than 20% of its stock price. In other words, understanding the composition of the underlying business in such companies will matter before deciding the downside.

#2 Switching from sensitive to defensives: Not always needed

While point 1 above was about entering into sensitive sectors with caution, what if you are already holding a company in such a space? By the time a crisis is in full swing, it is often too late to switch meaningfully from sensitive into defensive sectors — the damage to sensitive sectors has already been done and exiting such sectors would only deepen your losses. In our view, only the stocks with excess debt or leverage may be more sensitive beyond a point.

Hence, when you decide to exit the sensitive sectors, you might want to evaluate the exits based on whether the revenue/earnings is going to be temporarily deferred or whether a permanent shift is happening. If you are with mutual funds, the fund manager will take that call. If you are with stocks, it is best to wait it out, especially if you are with an otherwise high-quality company with a clean balance sheet.

#3 Small Caps: Broad Caution for Retail, Alpha Opportunity for Funds

Smaller companies are usually more sensitive to macro shocks and liquidity, so small caps often correct more sharply when fear takes over. For retail investors, the risk is compounded by the fact that flows to small-cap stocks can evaporate quickly in a crisis, removing a key source of buying support and accelerating the fall.

The Nifty Smallcap 250 index, however, is not a random set of illiquid names. It represents 250 companies ranked 251–500 by full market capitalisation from the Nifty 500 universe and is reasonably diversified. The largest sector weights today are in financial services, healthcare, and capital goods, with meaningful exposure to automobiles, chemicals, and consumer-oriented businesses.

The approach should differ based on the type of investor:

- Retail investors should treat the Nifty Smallcap 250 — accessed via an index fund or ETF — as a high-beta satellite allocation. It should be built gradually over three to six months by staggering purchases on dips, and it should remain meaningfully smaller than core large-cap or flexi-cap exposure.

- Fund managers can treat this universe as a fertile hunting ground during crises — selectively accumulating high-quality franchises with sound balance sheets and durable earnings at compressed valuations, particularly in financials, industrials, and engineering which is where this index offers unique companies.

#4 How Deep Can It Go? The Historical Playbook

Macro scares tend to trigger broad-based sell-offs, but history suggests that true “crisis-level” drawdowns are rare. During the global financial crisis in 2008, the Nifty 50 fell by more than 50% before staging a strong recovery. Covid-related shutdowns produced a similar scale of panic — all the Zudio and McDonald’s stores shut, hotels converted into Covid centres, and companies in consumption-oriented sectors reported 70–90% declines in quarterly revenues — before markets bounced back as earnings normalised.

By contrast, episodes such as the 2013 taper tantrum, demonetisation, the second taper tantrum of 2018, the Russia–Ukraine shock of 2022, or the recent 2025–26 “Trump tantrums” around US tariffs have so far resulted in corrections in the order of 10–25%, not systemic collapses. In both the deep crises — GFC and Covid — what amplified the fall was a specific structural factor: a mountain of domestic and overseas debt in 2008, and an almost complete blackout of business activity in 2020. Neither of those conditions applies today.

Source: Google

The current set-up is far more absorptive. A 10–20% market decline driven by war fears, oil prices, and trade tensions is a plausible and even useful scenario for long-term investors to gradually build equity exposure — whether through established companies, mutual funds, or ETFs — rather than a reason to exit in panic. The government also retains significant absorptive capacity on the fuel-price side, as demonstrated during the Russia–Ukraine crisis when windfall taxes on domestic oil and gas producers provided a meaningful policy buffer.

The Bright Spots Amid the Chaos

While the US–Israel–Iran conflict and renewed tariff frictions have made the last few weeks feel uncomfortable, we need to remind ourselves they coexist with powerful structural tailwinds for India. As Western economies seek to de-risk supply chains and raise defence spending, India is emerging as a beneficiary in engineering goods, electronics, and defence-linked exports, even as “Trump tantrums” on tariffs create short-term volatility.

As we wrote in our Equity Outlook 2026, trade deals with the US and EU combined with some openness to Chinese FDI represent a powerful combination. Exports to the US and EU provide revenue growth; Chinese FDI — largely in backward integration — creates manufacturing jobs, improves input competitiveness, and makes Indian companies more formidable in global markets. Together, they can solve for trade balance improvement, employment generation, and a structural leg-up to GDP growth. Significant increases in EU defence budgets add a further long-term tailwind for Indian engineering and electronics exporters.

Why a Roaring Bull Market Is Not What We Need

After being largely left out of the global AI-driven bull run and now dealing with the shock of the US–Israel–Iran war, there is understandable ill-feeling among domestic investors. But the post-Covid bull market taught us an important lesson: a roaring bull market is not necessarily good for secondary market investors.

That bull run primarily resulted in significant monetisation of stakes by PE investors and promoters, causing large-scale capital outflows from the market. The entire PE funding and exit cycle also intensified competition across sectors — low-ticket lending, consumer discretionary, fintech, consumer tech — with well-funded players crowding every space.

With our foreign reserves funded more by FDI and remittances than by earned trade surpluses, a bull market that primarily creates exits for early investors is not the kind of market we should be hoping for.

For secondary market investors, the goal need not be to chase a roaring liquidity-driven bull market. A moderately rising market that respects valuations and periodically offers sharp, sentiment-driven dips is often a far better environment to build positions in quality businesses — and that is exactly the kind of market that repeated geopolitical and trade scares tend to create.

Happy Investing!

P.S. If this report resonated with you and you have been thinking about a more structured approach to navigating markets like these, it may be worth exploring PrimeInvestor’s PMS offerings across stocks and MFs and a mix of both as well. Not just to time this particular moment, but to build the kind of disciplined, long-term equity practice that turns every shade of grey into an opportunity.

4 thoughts on “Shades of Grey: Investing When the Market Isn’t Black or White”

Would be interested to hear PI thoughts on positioning portfolios for a global recession marked by high inflation and prolonged fuel shortages alongwith the usual volatility and uncertainties. 🙂

Hi,

You are recommending Small Cap 250 index rather than Small Cap active funds. That’s something new. Any particular reason?

Thanks

Rajiv

The AUM sizes of large small-cap funds is causing disruption in investment (esp when investors want to invest in dips). This is an easier option but risky indeed. The quality of stocks in the index has also improved over the last 18-24 months. Thanks Vidya

on a different topic. your comments about MF were excellent.

Eg. Fpr “HDFC Balanced Advantage Fund(G)-Direct Plan” you had said in your old GUI that “while it scores poorly in containing volatility unlike its balanced advantage peers, it does a good job of delivering upside”

Things like these are gold and you should keep on doing such things. Ppl will pay for it if required.