Mutual funds have built more wealth for ordinary Indian investors than almost anything else. So, if you already invest through funds and someone tells you a PMS is the obvious next step up, it is natural that you pause to wonder if it is really right for you.

But the honest comparison isn’t “funds or PMS” in the abstract. It is really two questions. Do you keep managing your own fund portfolio, or have it managed for you? And is the right managed option a traditional, stocks-only PMS, or something built more sensibly around your risk?

In this article, we list out all the differences between a PMS and a mutual fund and then explain how you need to approach the question of PMS vs mutual funds.

Quick answer: who should choose what?

If you’re investing modest amounts and you’re early in the journey, the answer is easy. You stay with mutual funds, sensibly spread across equity and debt. Nothing more complicated is needed. Ideally, you need to invest in direct plans.

This is because a traditional stock-only PMS is a high-risk, single-asset product. It suits investors with a large corpus, a long horizon and a strong appetite for risk. When you’re early in your investment journey, such a high-risk product is not a good fit.

Therefore, a PMS is best suited for those who have already built sizeable wealth or who have a large investment portfolio. This is also the reason why the minimum investment in a PMS is set at Rs 50 lakh. Such portfolios require close care and constant management.

In fact, what PMS investors actually seek is someone to manage their portfolio: the allocation, the rebalancing, the discipline to act when it’s uncomfortable. That’s the gap a professionally managed PMS fills.

And at PrimeInvestor PMS, we have gone a step ahead. We’re not just stock-only, high-risk managers. We have instead approached PMS from a wealth management perspective, to reflect real portfolios and address different portfolio needs. PrimeInvestor PMS is built around mutual funds, stocks, or a blend of the two depending on your risk profile, rather than around equities alone.

The core difference: ownership model

With a mutual fund you own units of a pooled scheme, and the fund owns the underlying securities. With a PMS, the shares or mutual funds sit directly in your demat account in your name. A PMS is a product – the portfolio itself can be invested in stocks, mutual funds, and bonds.

Neither is better than the other – they are simply structured for different jobs. A pooled fund gives you instant diversification and simplicity. Direct stock ownership gives you control, customization and concentration.

How do minimum investment requirements differ?

Mutual funds are open to everyone, with SIPs starting as low as Rs 500. A PMS of any kind carries a SEBI-mandated minimum of Rs 50 lakh per PAN. With PrimeInvestor PMS, that Rs 50 lakh can be deployed across more than one strategy – so while the threshold may seem high, it still gives you a properly diversified, managed portfolio rather than a single concentrated wager on a single PMS strategy.

How much customization do PMS and mutual funds offer?

Since a mutual fund is a pooled structure, with all investor amounts pooled and then invested, all investors hold the same underlying portfolio. Each mutual fund follows a specific strategy – for example, an equity fund may follow a growth-at-reasonable-price approach, or a momentum strategy, or a value strategy and so on.

A PMS is different. While a PMS may have a set of stocks or funds that it considers investment-worthy at any point, individual PMS investor portfolios will be very different. This is because each investor enters the strategy at different points, and investments would have been made based on opportunities at that time. A call may be taken for some investors, but maybe not for others. Each PMS portfolio is monitored and acted on individually.

At PrimeInvestor PMS, we closely track all investor portfolios to spot opportunities to add, book profits, cut losses, or rebalance. Less about owning exotic things, more about someone doing the ongoing work most investors never find time for.

How are PMS and mutual fund fees different?

A mutual fund charges one expense ratio. All investors in the fund are charged the same expense. The NAV that you see is net of all expenses.

A traditional PMS can have a fixed fee as a percentage of the AUM, or a performance fee which takes a cut of your profits, or a mix of the two. The fee structure can vary between investors in the same PMS. PrimeInvestor PMS has only a fixed percentage fee on AUM and no profit sharing. This way, we ensure that your returns stay with you and the only way we grow is along with you.

Which is more tax-efficient: PMS or mutual funds?

Gains on listed equity and equity funds are taxed at 20% if held under a year, and 12.5% on gains above ₹1.25 lakh a year if held for more than 12 months.

The difference, though, is that in a mutual fund, the buying and selling activity within the fund is not a taxable event. You pay the tax only when you redeem the mutual fund.

In a PMS, the securities are owned in your name. therefore, any redemptions done in the portfolio will be subject to tax for you. In a high-churn stock PMS, the manager’s own trades can hand you short-term gains. Low turnover matters, which is why a disciplined portfolio keeps its core deliberately stable.

How does liquidity and exit work in each?

Open-ended mutual funds are highly liquid, with money usually back in a couple of working days. A PMS is a bit less liquid and more complicated. Since the securities are held individually, you will first need to place a redemption request with your PMS manager, who will then have to identify securities to exit and mobilize the amount. The whole process can take more than a few days. A PMS isn’t the place for money you might need next month!

Performance and returns: structural reasons they differ

It’s tempting to judge all this on returns alone, but most of the outcome comes from things people overlook. Returns between mutual funds and PMS aren’t directly comparable. Mutual funds are regulated much more closely, as they are meant for investors across all walks, and not just those with large portfolios. For example, regulations for mutual funds dictate include caps on sector and stock exposures, market cap allocations, credit risk allocations, duration calls they can take and much more. They are more diversified and take less high-risk bets.

A PMS on the other hand do not have regulations governing portfolio structure – regulations in PMS typically address investor protection, disclosures, and the like and not PMS portfolio compositions. The idea is that investors in a PMS are more informed, and have the capacity to take on differentiated products in their portfolios.

Therefore, a PMS can generate by far higher returns than a mutual fund especially where these are stock-only PMS. But then, these can fall much more as well.

At PrimeInvestor, we believe asset allocation drives results at least as much as which fund or stock you picked. Protecting the downside matters, since a portfolio that falls 50% has to double just to get back to where it started. And “buy and hold” was never meant to mean “buy and forget.”

Therefore, even with mutual funds, left alone, self-managed portfolios drift from their intended mix, accumulate overlapping funds, and rarely get rebalanced. A traditional stock PMS errs the other way, concentrated and high-risk. A managed, multi-asset portfolio sits between the two: active oversight, sensible spread across equity, debt and gold, and rebalancing that takes the emotion out of the call. That is what we do at PrimeInvestor PMS.

Which one makes sense for you?

Now that you know the differences between a mutual fund and a PMS, let’s get to the question of which one you should have. The dividing line is capital and intent. Simply put, below ₹50 lakh, build with mutual funds. At ₹50 lakh and above, a well-run PMS is a good portfolio choice.

The ₹10 lakh investor

Stay with mutual funds. Direct plans, a reasonable split across equity and debt, and patience will do more for you than any premium product. Disciplined investing and growing your corpus is your focus here, not fancy products.

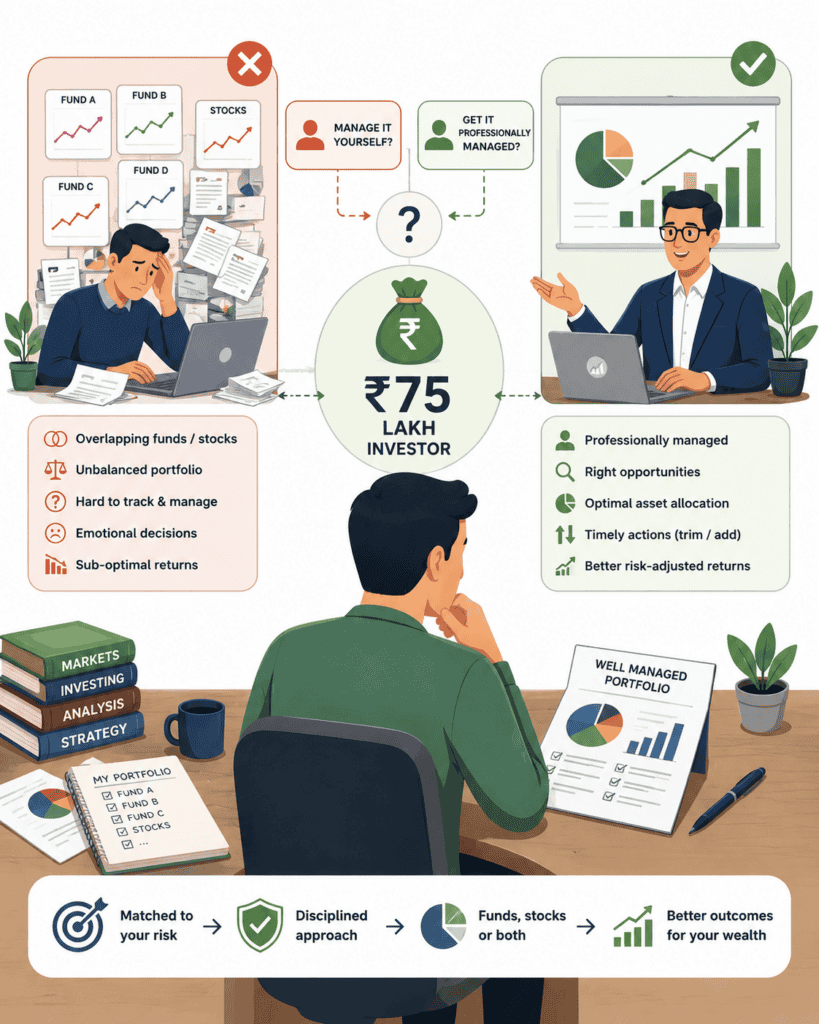

The ₹75 lakh investor

You now qualify for a PMS, but the right question isn’t “should I swap funds for stocks.” It’s whether you want the portfolio actively managed instead of doing it yourself or letting it drift. If your funds have multiplied into an overlapping, unbalanced pile with several funds or stocks, then it needs a professional hand.

When portfolios get large, finding the righ opportunities, deciding weights, knowing when to trim or add, are all complicated questions. Unless you have the time and expertise, it would be tough to answer these and the result would be a sub-optimal portfolio that earns less than it should. Professional management, built around funds, stocks or both and matched to your risk, usually serves you better than trying to handle it all yourself.

The ₹2 Cr+ investor

Here a PMS can be your core wealth solution rather than a side bet. This is especially when a PMS (like PrimeInvestor 😊) can offer multiple solutions that address all your portfolio needs, instead of a particular slice. A professionally managed portfolio across equity, debt and gold, calibrated to your goals and watched continuously would work well. You can split the corpus across more than one strategy under a single relationship. For most investors at this level, the value isn’t in owning the riskiest equity portfolio on offer. It’s in having serious money managed with discipline.