It is no small matter when the Chairman and Independent Director of India’s largest private sector bank by market capitalization resigns abruptly. It becomes more serious when the stated reason is that certain practices were not aligned with his ‘values and ethics’.

What followed only deepened investor unease. A series of developments kept governance concerns in focus, and more recently, a data security incident at HDFC AMC has added to worries around the broader HDFC group.

Given the number of queries we have received—from deposit safety to implications for shareholders and mutual fund investors—it is evident that confidence has been shaken.

In this report, we take a closer look at the issues the bank has faced in recent months and assess whether they warrant concerns around governance and, more importantly, the safety of your investments. We also examine the recent data security incident at HDFC AMC and its implications for investors.

The resignation that shook India’s largest private bank

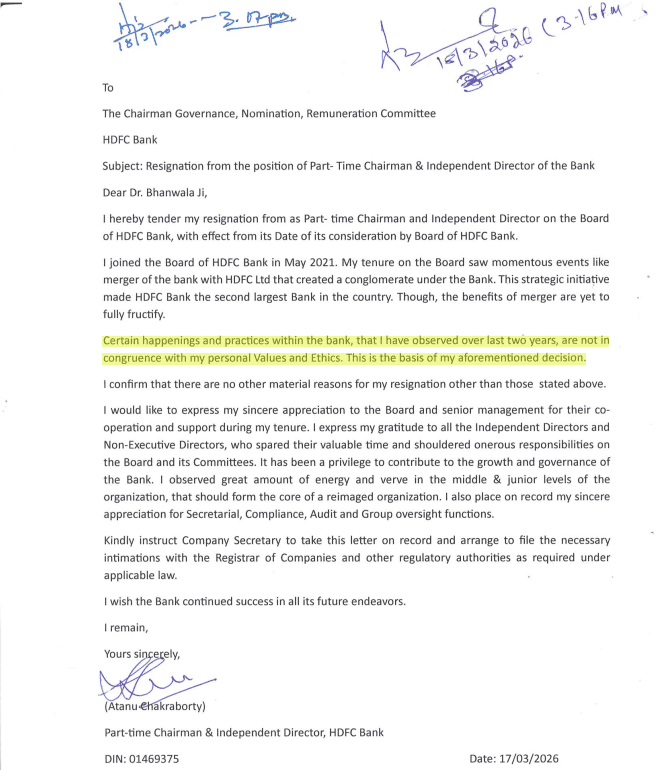

Atanu Chakraborty, a retired IAS officer, served as the Part time Chairman and Independent Director of HDFC Bank from his appointment by the RBI in May 2021 until he suddenly resigned on March 18. His resignation, specifically, his statement ‘Certain happenings and practices within the bank, that I have observed over the last two years, are not in congruence with my personal Values and Ethics. This is the basis of my aforementioned decision.’ implied that all was not well governance-wise and rattled investors. This was no ordinary exit.

The stock of HDFC Bank immediately fell over 5%. It continued to spiral in the days after even as mutual funds countered the sell off and bought the dip.

Damage control by the board and the RBI

Not to let matters get out of hand, key players quickly dived in to minimise the damage.

The RBI issued a reassuring statement on March 19, 2026, highlighting that the bank is ‘a Domestic Systemically Important Bank (which basically means the bank is too large and important to the economy to be allowed to collapse) with sound financials, professionally run board and competent management team’.

The board of HDFC Bank moved quickly to stabilise sentiment and reassure rattled investors by appointing veteran banker Keki Mistry who has been associated with the organisation for over four decades as interim chairman. Both the board of the bank as well as Keki Mistry quickly stepped in to state that governance concerns were unwarranted.

The Bank went a step further and appointed external law firms to determine whether there was any merit in the concerns flagged and to perhaps end up with an external ‘certificate’ giving them a independent validation of governance practices. While this report is yet to be finalised and is expected shortly, preliminary reports indicate that the bank will indeed end up with a clean chit.

Post this, the next steps on reappointment of MD & CEO, Sashidhar Jagadishan, whose term ends in October 2026, will be taken. Reports indicated that a power struggle between the two was the catalyst to the resignation. While the reappointment is still a couple of months away, it is late by banking industry standards and therefore has a cloud of uncertainty looming over HDFC Bank.

Were the governance concerns raised by the Chairman warranted?

In assessing governance concerns, it is important to distinguish between:

- structural governance failures

- execution lapses, and

- industry-wide practices

Let’s unpack the main concerns that cropped up.

#1 The AT1 bonds misselling allegation

One of the issues mentioned by Mr.Chakraborty during his interviews was the misselling of Additional Tier-1 (AT1) bonds. These instruments are best suited to sophisticated investors that understand how they work. The bank was accused of promoting these bonds as high yield instruments without adequately conveying the risks at the bank’s Dubai (DIFC) branch. This was subsequently termed as a ‘technical documentation lapse’.

The branch was consequently prohibited from onboarding new clients by the Dubai Financial Services Authority (DFSA) in September 2025. Following an internal investigation by the bank’s Disciplinary Committee, three employees were terminated from service on 9 March 2026, while 12 other senior-level individuals received penalties.

While the incident reflects gaps in oversight and suitability enforcement at the branch level, the actions taken (regulatory restriction, internal disciplinary measures) suggest containment rather than a systemic governance failure.

It also signals a broader industry challenge, rather than evidence of a bank specific corporate governance issue.

#2 Tech troubles

While this issue was further back in time, it came up soon after Jagadishan took over. The bank was faced with an RBI ban on HDFC Bank issuing new credit cards and digital launches following repeated power outages that came in the way of electronic banking services. RBI also asked the bank to fix accountability and resolve the issues.

This was the first action of its kind taken by the RBI against any private bank. This ban was subsequently lifted 8 months later following the issues being addressed. In our view this did not reflect a governance issue and has no longer cropped up after resolution in 2021 indicating that the issue is well and truly in the past.

Subsequently, similar issues were faced by other banks like Kotak Mahindra Bank in April 2024 (credit card issuance and digital onboarding ban) and Bank of Baroda in October 2023 (onboarding ban on its mobile app), which were eventually resolved in February 2025 and May 2024 respectively.

Neither of these issues fall under category 1 (structural governance failures) we mentioned earlier.

What all of this means for you

One of the key monitorables for investors is the reappointment of the current Managing Director, Sashidhar Jagadishan, whose term is due to end in October 2026. The outcome is likely to be closely watched by both domestic and foreign institutional investors.

In our view, non-reappointment of the current MD should not automatically be construed as a corporate governance concern. A recent example is Kotak Mahindra Bank – in January 2024 the board appointed Ashok Vaswani as MD & CEO following Uday Kotak’s exit, opting for an external candidate despite the presence of several experienced internal contenders. While the move sparked discussions around succession planning, it was not viewed as a governance issue.

Similarly, the RBI declined Federal Bank’s request for a one-year extension for its long-serving MD & CEO, Shyam Srinivasan, whose 14-year tenure ended in September 2024. The bank subsequently appointed KVS Manian, a veteran banker from Kotak Mahindra Bank, as his successor.

In the case of HDFC Bank, had there been clear governance lapses, there would have been other rumblings likely in the form of senior management exits, similar to what was witnessed at IndusInd Bank following the discovery of accounting discrepancies of nearly Rs. 2,000 crore in its derivatives portfolio.

For HDFC Bank deposit holders – No cause for alarm: HDFC Bank remains a safe banking institution in India. As a Domestic Systemically Important Bank (D-SIB), it is subject to higher regulatory oversight and capital requirements, making its deposits relatively safer than those of most other banks in the country.

For HDFC Bank shareholders – Fundamentals remain: The issues cited appear to stem from industry practices rather than any concerning HDFC Bank specific conduct. As such, we do not believe it constitutes evidence of corporate governance lapses at the bank.

The noise around HDFC AMC. What happened?

On May 16, 2026, HDFC Asset Management Company disclosed unauthorized digital activity within its IT infrastructure. Investigations revealed that approximately 680 GB of company and investor data was compromised.

Should investors worry?

The Indian mutual fund industry operates under a robust framework for managing investor assets, involving multiple independent entities such as Registrars and Transfer Agents (RTAs), custodians, and trustees. While the AMC maintains client-facing portals, the core ownership of the investment registry remains with the RTAs—specifically CAMS, in the case of HDFC AMC. Because of this architecture, the breached data, by itself, does not enable unauthorized redemption or transfer of investor assets.

However, because attackers may possess linked investor data (such as PANs, addresses, bank account details, and mobile numbers), there is a risk of targeted social engineering and phishing attempts. Investors must remain vigilant against these threats, though this risk is inherently no different from other personal data breaches.

While this incident has not directly impacted investor assets, a mass exodus of investors from a fund house or from specific funds can harm remaining unitholders. This dynamic can trigger performance concerns, as a fund manager’s focus shifts from identifying investment opportunities to managing continuous redemptions. In extreme cases, it can lead to a liquidity event where a fund house struggles to sell underlying assets to meet redemptions—a scenario to which debt funds are more vulnerable. We have verified the daily assets under management (AUM) across HDFC AMC’s funds and found no signs of panic selling as we write this. The firm’s AUM continues to move in line with the broader industry and comparable large AMCs.

In short, if you are an investor in HDFC Mutual funds, you don’t have to take any action based on this event, other than resetting your credentials to its online portals.

Should shareholders of HDFC AMC worry?

There is currently no evidence that the AMC’s daily operations or business volumes have suffered from this event. However, any subsequent regulatory actions could have some minor impacts, such as increased operational costs or monetary penalties. We do not anticipate any severe regulatory intervention that would halt the AMC’s core operations, as regulators are typically careful not to trigger panic selling among the investing public.

The bottom line

HDFC Bank has indeed faced a crisis of confidence in recent months. This has naturally meant it has been under far more scrutiny than ever before.But at this stage, the developments point more towards episodic issues and heightened scrutiny rather than evidence of systemic governance failure. That said, the upcoming board decisions—particularly around leadership continuity—will be critical in shaping investor confidence.

We will continue to monitor developments closely, especially the upcoming Board meeting.

Key contributors to this report: Chandrachoodamani NV, Pavithra Jaivant, Vishwanath A and Bipin Ramachandran

None of the stocks mentioned in this report should be construed as a recommendation on the respective stock. Please read our disclaimers and disclosures carefully.

3 thoughts on “HDFC Group’s Governance Concerns: Red Flag or Rough Patch?”

One other issue which cropped up in the last few weeks around disguising higher interest rates as marketing expenses – which attacks the very foundation of ethics. This issue hasn’t been considered in the above article. Is there any reason for the same?

I would like to know how this should be viewed in the overall context of HDFC Bank shares underperformance.

This pertains to the Rs 25,000 crore bulk deposit from MSRDC, with the alleged Rs 45 crore amount representing just 0.18% of the deposit value. The bank has denied any wrongdoing in this regard, but large deposits come with certain bargains. Regulations also prohibit banks from offering differential interest rates on such deposits.

From an investment perspective, we would be more concerned if there were any premature withdrawal of large deposits or bank is unable to mobilize deposits rather than these allegations, unless they are formally taken up by the RBI in their annual inspection.

IMO, HDFC is sorely in need of a fresh perspective and re-look at how to position itself, especially in the global markets — maybe bring in a new, dynamic face who can re-vitalise the group. Also encouraging young directors like Mr. Sandeep Parekh and Ms.Maheshwari to be more proactive might help— being the market leader for too long has led to “complacency” , I think.