Exactly a year ago, we wrote about how rich stock market valuations drive capital allocation decisions by companies. The sentiment in the market was the same then as it is now—a red-hot primary market and a muted secondary market.

Within a year since then, history has started repeating itself. We’re witnessing Leverage Buy-Outs (LBOs—buy-outs funded by borrowing against the target company’s balance sheet) by Tata Motors and Tega Industries, swallowing mammoth assets abroad. It’s a popular trend from the pre-global financial crisis era, back when exuberant capital markets made anything seem possible.

The market over the last year has been nicely divided. On one side, the secondary market got hit—muted growth expectations from heavyweight sectors, US tariff woes, and relentless FPI selling. On the other side, the primary market was in a frenzy. New business models, strong narratives, and a never-ending parade of IPOs. Meesho, Groww, and ICICI AMC joined the lakh crore market cap club. Promoters and PE investors kept queuing up to exit at rich valuations at every market bounce, and the line never seems to end.

Then came another trend: companies returning to the market post-IPO to raise money for “business expansion,” and those QIPs (Qualified Institutional Placements—capital raises from institutional investors) were getting lapped up. When companies raise money following their IPO at these rich valuations, it just bloats their capital structure and builds impossibly tall asks on growth and return ratios.

Meanwhile, there were accidents too. Roaring sectors like EMS, after doing multiple rounds of fundraising post-IPO, are now seeing the market put their business economics under serious question.

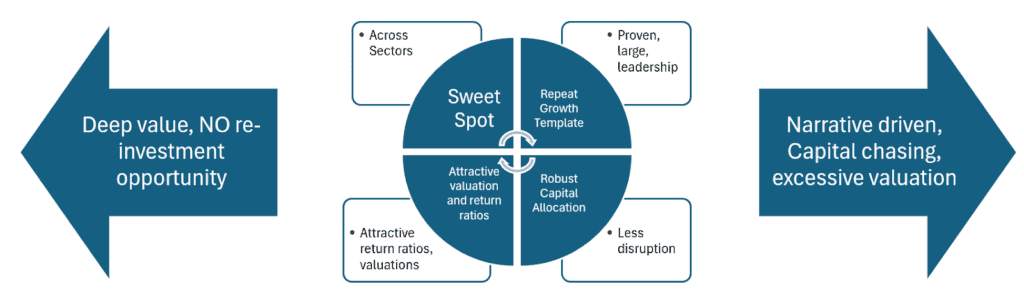

So, for those who don’t want to lap up what the PEs and promoters are spitting out—where poor business economics are buried under the glamour of narrative—the market itself is revealing a white space to hunt.

This white space exists between two extremes. On one end are great companies with little reinvestment opportunity for growth. On the other end are companies where capital is chasing narrative over numbers, with valuations completely divorced from any conventional wisdom.

The opportunity lies in between. It spreads across sectors and stocks. It is completely bottoms-up.

In this Part II, we examine this white space the market has thrown in front of us—where we can see a clear case of favourable risk-reward, where secondary market investors stand to win.

This space is occupied by companies that are profitable, have leadership, stand out for capital allocation, and where ownership and minority shareholders’ interests align. There’s no ready formula here, but let’s glide through what many of them did over time to arrive at a framework.

For this discussion, we’re mainly taking examples from the top 200 companies by market cap, though we’ll go beyond that wherever needed to highlight specific cases. We’re not discussing unrelated diversifications born from the compulsion to find opportunities to reinvest capital—like Reliance, ITC, L&T – and their outcomes.

#1 Disciplined Capital Allocation – Repeating the Same Thing

“Discipline is repeating the same boring thing” — Rajiv Bajaj

Whenever we talk about wealth creation, a handful of companies repeatedly top the list over time. One common thing with such companies is doing the same thing over a long period—reinvesting cash flows back in the same business at superior RoCE.

When we look at companies like Asian Paints, Pidilite Industries, Bajaj Auto, Eicher Motors, Maruti, Divis Lab, Cipla, Dr Reddy’s, PI Industries, Page Industries, MRF, Shree Cement, Supreme, Blue Star, Balkrishna Industries, Berger Paints, Schaeffler, Dr Lal PathLabs, Syngene, D Mart, Phoenix Mills, KPR Mills, etc., what is visible is a trend of doing the same thing for long.

Even the IT and consumer behemoths come here, but unfortunately, they are struggling with little reinvestment opportunities versus their cash flows.

The MRF template: Capital structure discipline

MRF provides a clear learning template as to how a company with Rs. 4 crore share capital generates Rs 30,000 crore in revenue and ~Rs. 2,000 crore in profits. There are many other great companies, but MRF has kept its capital structure as such to easily understand the essence of wealth creation—reinvesting its cash flows in the same business for a long period at superior RoCE.

Shree Cement’s growth template was also something mirroring that of MRF, and so for MRF’s counterpart Balkrishna Industries.

Resisting the diversification temptation

Divis could have thought of diversification into US generics, domestic branded formulations, etc., or even mammoth acquisitions. But it decided to stick to what it is good at.

HDFC Bank and Muthoot Finance add to this template from the financial space—doing the same thing repeatedly for long. Muthoot’s closest peer fell victim to diversification while our waiting is extending forever to see the next HDFC Bank.

Zero dilution, maximum reinvestment

Recently listed Korean automotive giant Hyundai is taking a mammoth capital allocation decision that would plough back its entire cash flows into product, R&D, engineering, and technology. This is a company that has never diluted its capital since its beginning in India in 1998. Same with its Korean counterpart, LG Electronics, where its new plant is being put up at an investment that is more than its existing gross block, for product expansion, backward integration, and new export opportunities.

We have also seen a stark divergence in the listed EV 2-Wheeler space between Ather and OLA, where the stock price of one has doubled and the other has halved. What separates the two is the promoters’ clarity of thought on capital allocation.

The profitability-first moat

In all these companies, it is about first being best in their business in terms of profitability and then reinvesting cash flows back into the business to build “gorillas” in their space. And being more profitable versus competition is what gives real “moat” to be ahead in terms of growth and market share with more free cash available to maintain lead.

It also boils down to DNA of promoters where they have immense clarity of thought as to what they will do and what they WILL NOT.

Beyond these top 200 are also a bunch of companies including the likes of Cera Sanitary, Hawkins Cookers, V Guard, Nesco, Asahi, Kovai Medical, LG Balakrishnan, Elgi Equipment, Hatsun Agro, CCL Products, Ahluwalia Contracts, TCI, etc., where you can find similar DNA with respect to capital allocation.

#2 Visible Enhancement of Competitive Positioning—Creating New S-Curves

“Only the paranoid survive” — Andy Grove

Beyond repeating the same thing, there are other capital allocation decisions that successful companies often take. These include acquisitions and related diversification that adds something clearly to their competitive positioning, creating new growth engines or S-Curves (new business cycles that drive the next phase of growth).

But these are NOT mammoth capital allocation decisions relative to their size or that cast uncertainty on their numbers or return ratios. They are generally funded through internal accruals rather than tapping capital markets, and hence such decisions are NOT triggered by a buoyant capital market.

Let’s discuss some companies here that have not only repeated what they were doing but also took bolder steps to significantly enhance their competitive positioning. TVS Motors, Marico, Godrej Consumer, Pidilite, Persistent Systems, Uno Minda, Endurance Tech, Bajaj Auto, Federal Bank, Solar Industries, Bharat Forge, Trent, Astral, Havells (Lloyd), Motilal Oswal, etc., are some such companies that turned a bit bolder to pursue related diversifications, stitch some acquisitions, or took a plunge to do accelerated investments in R&D to enhance their competitive positioning, but within the limits of what they can fund internally with discipline and long-term goals.

Product innovation as an S-Curve: The TVS story

TVS Motors has been the boldest of all 2-wheeler OEMs in the last decade, where it took a plunge to deliver sophisticated and feature-rich products to masses when others believed that time hasn’t come for such products in the Indian market. TVS N-Torq, the stylish but least fuel-efficient 125cc scooter, was a big winner amid petrol price hikes from Rs. 60 to 105, as the youth grabbed it for the features and performance it offered. Nothing could stop TVS since then to where it is now with sophisticated and feature-rich products until its rise to dominance in EVs as well.

Organic growth engines and strategic acquisitions

For Marico, D2C (Beardo, Plix, Just Herbs, True Elements) is the third S-Curve starting from a single engine, Parachute, and then its Saffola umbrella with which it even triumphed Quaker in Oats to become No. 1. Pidilite has turned multiple innovations like Dr. Fixit and Roff into new growth engines while it also made the acquisition of Araldite maker amid Covid in October 2020 for Rs. 2,100 crore. That was a time when a lot of companies were drawing credit lines or pausing capex to keep them afloat. For Trent, Zudio was an organic initiative that led to a big S-Curve, while Havells lapped up the business of Lloyd in a slump sale and made it work for itself.

Diversification into value-added products

Endurance Technologies, an auto ancillary player in die-casting, has created multiple S-curves with diversification into value-added (import substitute) products such as advanced suspension and braking systems for both 2-wheelers and 4-wheelers. Solar Industries and Bharat Forge are standout examples of companies that created new enviable S-curves in their business through persistent effort. For both these companies, defense is becoming a major growth engine, on domestic and exports.

Tech and fee income creation in financial services

Large private banks have created valuable capital market, asset management, and insurance subsidiaries through calibrated capital allocation and created meaningful fee income businesses. For Federal Bank, the decision to make accelerated investment in tech is what made it different from its six other regional counterparts to leapfrog—in turn an outcome of being disciplined and profitable to be able to do so when others were battling asset quality issues.

All these are cases of calibrated capital allocation decisions that brought visible competitive advantages without casting material uncertainty on numbers or return ratios. They created new S-Curves with good business economics and added to their profitable growth.

Again, the first point of being more profitable in their business was the key advantage that was freeing up capital for them and allowing them to take such capital allocation decisions. As explained previously, it also boils down to DNA of promoters where they are more likely to take calibrated and thoughtful capital allocation decisions over a period of time than chasing size or building empires.

“Build” versus “buy” and “how much you pay” is also a thought that lives through the minds of such promoters.

#3 Mammoth Capital Allocation Decisions and Evaluation Challenges

Beyond the first two points on repeating the same thing and doing calibrated allocations to improve competitive positioning comes the case of mammoth capital allocation decisions. They generally carry the nature of chasing size or dominance and could end up in a make-or-break kind of situation as well. These often happen when capital markets are buoyant enough to raise resources and so are often triggered by easy availability of capital.

(The separation between the decisions to improve competitive positioning versus chasing size or empire building may be very nuanced in some cases.)

Investors often find it challenging to evaluate mammoth capital allocation decisions.

The Cautionary Tale: Tata Steel’s Corus

Tata Steel’s acquisition of Corus to just go global still stands out as a disastrous capital allocation case. In two of our previous articles, we had given a math of how much would have been the value creation for Tata Steel shareholders in the last five years had it not pursued the acquisition of Corus.

Current Mammoth Deals: Tata Motors and Tega Industries

As we write this, Tata Motors and Tega Industries are two corporates pursuing mammoth M&As by taking significant leverage on their balance sheets, the magnitude clearly reminding us of the pre-global financial crisis period.

The recently listed Tata Motors Commercial Vehicles (CV), with a lean balance sheet (0.5X leverage) and a profitable and dominant CV business, would now go and buy Italy’s IVECO in a Rs. 38,000 crore deal. Tega Industries, with Rs. 1,500 crore net worth, is initiating a Rs. 15,000 crore buy-out by taking debt on the balance sheet of the acquiring company—a classic LBO only due to a buoyant capital market.

The Contrast: Titan and Bajaj Auto’s Smarter Approach

Let’s now look at these two M&As versus the other two deals at centre stage in 2025—Titan’s acquisition of Caratlane at Rs. 17,000 crore valuation and Bajaj Auto’s Rs. 7,800 crore acquisition of European motorcycle maker KTM.

In the case of both Titan and Bajaj Auto, they are assuming full ownership of businesses that are already part of them for an outflow that is less than a year’s EBITDA. Titan’s outflow on the Caratlane acquisition is only Rs. 4,621 crore in this deal valued at Rs. 17,000 crore as Titan already owned a majority stake. Bajaj Auto’s KTM acquisition at Rs. 7,765 crore was for a motorcycle brand that globally features in the top 3 and that Bajaj has been making and exporting from India for over a decade. The businesses, culture, strengths, and weaknesses are known in much greater detail for both Titan and Bajaj.

On the other hand, the mammoth M&A deals of Tata Motors and Tega come with mammoth financial commitments and large-scale integration needs and are an outcome of a buoyant global capital market. These transactions would not have been initiated by these companies if the capital market were not this buoyant.

Consumer Sector: The Mixed Bag of Results

Unilever’s acquisition of GSK Consumer Healthcare was a major capital allocation decision that happened in 2021 and was stitched out during a period of rich valuations that enabled that acquisition to happen. Barring the first-year adjustment, that mammoth Rs. 40,000 crore deal doesn’t seem to be moving the numbers much.

(HUL’s recent acquisition of Minimalist for Rs. 3,000 crore was a minor one, the one of the character of a calibrated capital allocation that is enhancing its competitive positioning in a fast-growing segment.)

Zydus Wellness, the owner of Sugarfree, initiated a similar deal to buy Heinz India (Complan and Glucon-D) at the same time and raised money via QIP later, but is still struggling with subpar growth and return ratios. The most recent one would be Tata Consumer’s Rs. 6,900 crore capital allocation decision to buy Ching’s Secret and Organic India, with combined revenue of Rs. 700-800 crore, funded through a fresh round of equity dilution. The outcome needed from this capital allocation is huge to move the RoE needle to double digits.

(Earlier, Tata Consumer did an M&A with Tata Chemicals to acquire its consumer business in 2020.)

When it comes to this part on mammoth capital allocation decisions versus the first two parts (repeating the same thing, calibrated capital allocation), there is more complexity related to the marriage, culture, integration, and long-term financial outcomes. Here, the chances of going wrong and firing back on profitability or balance sheet are of a bigger magnitude.

Other Sectors: Pharma, IT, Auto Ancillaries, and Q-Commerce

Beyond the examples cited above, there are also several other large capital allocation decisions that are in the nature of chasing size or dominance that have happened recently or are in the making.

Mankind Pharma’s recent decision of Bharat Serum and Biocon’s acquisition of Viatris to become one of the largest in the biosimilar space are mammoth capital allocation decisions that lay investors may find it extremely difficult to evaluate.

As we write this, the share-swap acquisition of Encore by Coforge is in the making, one of the largest that we have seen in our IT space.

Samvardhana Motherson, the auto ancillary giant, has a never-ending plan for acquisitions and is pursuing one as we are writing this—that of Nexus Auto Electric wiring for Rs. 2,171 crore. With too many acquisitions, material debt, geographical spread, and a lot of accounting for intangibles and amortizations, it is nearly impossible to research such a company for a lay investor. The kind of volatility in the stock versus what investors could have made in the last decade was completely unfavorable.

The ongoing Eternal versus Swiggy versus Zepto race in Q-Commerce is not different from the AI race in the US, where companies are fearing investing little and missing the bus, and Zepto is just speeding up its capital market debut to get it funded. There is a race for dominance, and the third or fourth player is clearly going to be left out with literally zero value creation. This puts investors in a dilemma as to how to evaluate the risk-reward profile of such investments.

The Bottom Line: Know What You Can Evaluate

Where evaluation becomes difficult, it is important to take a second thought on what to rely on for outcomes of such decisions. Sometimes, great promoters may make it work. Tatas, Unilever, Kiran Mazumdar Shaw, or the young Q-Commerce entrepreneurs may do it. They MAY NOT make it work also (as history shows). Mammoth capital allocation decisions can make or break companies, drag financial performance for long, lead to capital dilutions, subpar return on capital, and even permanent loss of capital for investors.

As investors, it pays to be candid about what we can evaluate and understand versus what we cannot and not be carried away by FOMO.

We will sum up the three points on capital allocation that we discussed above and put it in the form of a framework and then move to another critical aspect—ownership structure, which can determine whether even the best capital allocation plans serve minority shareholders.

#4 Ownership, Equity, and pouring ESOPs

The last decade has brought in plenty of FDI investments into the country with PE investors funding a large chunk of start-ups in fintech, consumer-tech, internet, lending, consumption, etc. The wave of IPOs since 2021 is a vindication of the kind of funding that happened over the last decade. But for a seasoned investor, one extraordinary trend that is visible is the change in business ownership structure.

Founders or promoters own little on most of these start-ups as aggressive capitalization for scale-building led to majority ownership in the hands of PE investors. Promoters were largely compensated through ESOPs, and it is a never-ending phenomenon. We often have to adjust the EBITDA or accept the adjusted EBITDA they put out when evaluating these companies. Even smaller consumer categories like luggage and mattress itself have 5-10 PE-funded start-ups each. The entire affordable housing finance space has been funded by PE players as if they found “gold” at the bottom of the pyramid.

The Prashant Jain question: Who will run these businesses?

In this backdrop, a question put forward by ex-HDFC MF fund manager Mr. Prashant Jain deserves special attention: Who is eventually going to run these businesses in the future? The hugely successful ones would be institutionalized and would be run, but the future of failed ones would definitely hang in balance with zero sign of persistence. We do have examples of institutionalized Infosys, HDFC, ICICI, L&T, etc., already. But this hunting ground that investors are dealing with today with a bunch of new listings with low promoter stakes is going to be more difficult. The sad state is that the same companies are again tapping the market to raise money for business expansion, diluting stakes of promoters/founders further.

The Sona BLW Case: PE Exit, Low Promoter Stake, and Family Battles The case of Sona BLW, where PE Blackstone sold its 67% stake for ~Rs. 15,000 crore, is one to point out. Even post this mammoth monetization by PE, the net worth of the company was just Rs. 2,000 crore and has tapped the capital market to raise Rs. 2,400 crore through QIP to fund an acquisition. Sadly, the promoter stake is 28% and is under a bitter family battle now post the demise of its Chairman, Mr. Sunjay Kapur.

The Binary Risk: Activist-Driven Capital Allocation

The risk-reward in these companies with little promoter ownership could be “binary” in the future and put investors in a spot in evaluating investing decisions. The capital allocation plans in such enterprises in the future could also be triggered by activist investors with little predictable templates versus a promoter-run enterprise with a certain DNA. Maybe we can defend by arguing that this culture exists in markets like the US and is not bad, but we don’t know whether it is easy for minority shareholders to invest and win in such a scenario.

PE-Driven M&As: The Coforge-Encora Example

As we write this, the share-swap acquisition of Coforge-Encora is in the making, one of the largest in the IT space—a classic case of activist/PE investors triggering an M&A. Here, Coforge is an entity owned by domestic institutions (NO Promoter) while Encora is one owned by two major PE investors (Advent and Warburg).

One obvious outcome here is that the PE investors would become owners of a company (Coforge) listed in India through which they can monetize their stake as early as in 2026. Crompton Greaves Consumer, one of India’s oldest consumer electrical companies, was lapped up by the same PE, Advent, that owns Encora. Advent exited Crompton Consumer fully a few years ago in the open market and is now owned by domestic institutions and run by professional management.

Scale Matters: Winners Get Institutionalized, Losers Get Orphaned

While this trend of institutionalized corporations is welcoming, only the scaled-up ones will be able to attract leadership and talent to run them in the interests of minority shareholders, and the ones that fail to attain scale or with weaker moats will be orphaned. In this scenario, investors need to ask the question of growth, survival, and value creation in the evaluation stage itself to avoid definite traps—not inheriting orphaned businesses.

10 thoughts on “When Markets Divide, Where Should Investors Hunt”

One of the best articles I have read on Prime Investor. Looked really long before I started but with the kind of examples it was so interesting to read it.

Hi Chandra, i have a doubt here. Such companies will always trade at higher valuations, now this is the pattern post covid. What is the valuation metric to be employed and how to know if the company is deviating.

Welcome your query sir,

You are right. Such Cos. will be generally trading at higher valuations.

But when looked at it in today’s context, this is a space where risk-reward is favourable Vs new listings/new themes (where Promoters, PE are sellers) or where many Cos. are not finding enough re-investment opportunities

Reasonably good investment opportunities are available at valuations that will not hurt/cause much damage, but returns will come with patience. So, the focus was to first identify the space where risk-reward is better, hunt in that space and then be patient.

Otherwise, overall market valuations should turn really cheap to make any meaningful returns, which is not the case. Ex of financials, commodities are trading upwards of 30-35 times now.

Hope this clarifies

Thank you

How to identify the S curves and the potential outcome.

Welcome your query sir,

Here are few steps that would help;

1. Fixed asset investments in cash flow statement will give a sense how much a Co. is re-investing. Then the Que boils down to where? – existing or new lines. Lot of examples have been discussed in the article

2. Based on what a Co. is good at, it will have optionalities as demand pattern changes or as new opportunities arises through premiumisation, product extensions, new brands, new category creation, etc

3. Choosing a good management with a good DNA of capital allocation decisions (calibrated, more organic) will ensure that outcomes can be more certain than in other cases – we have discussed about calibrated capital allocation Vs mammoth capital allocation decisions in the article

At last, it is again about creating a diversified portfolio from this space and there will obviously be failures. But may not hurt that badly as in spaces that offer little risk-reward

Hope this clarifies

Thank you

Well researched article.

Hi N V,

Excellent article. Hence our selection of products from – Hyndai, LG, Havells, Beardo, Pidilite etc giving meaning to the purchase. Thanks.

Rajiv

Thanks for the nice article, pl keep them coming!

Very well written and detailed article.

Excellent article. Kudos Chandra. You have dissected how capital allocation is a major driver, how it can expand or hinder the growth.

Comments are closed.