We first took a look at the diagnostics sector in India in 2021 when pandemic fuelled business made the sector hard to ignore. But the prominence of the sector hasn’t faded with the pandemic. Structural drivers like improving awareness, greater preventive testing, higher prevalence of non-communicable diseases and greater focus on health care by the government have continued to boost it. The new Occupational Safety, Health and Working Conditions (OSH) Code, one of the four new consolidated Labour Codes implemented in November mandates that employers must provide all workers above the age of 40 years with a free annual health check-up, adding another potential revenue stream for diagnostics players to tap.

This imarc report estimates industry growth at a 9.2% CAGR from 2025 to 2033. With only 15% of the sector belonging to organised players, consolidation remains a key theme. It is expected that the organised players will grow at a faster clip than the unorganised going forward.

Diagnostics stands out among the other healthcare sub-sectors for faster growth, relatively lower capex requirement and better return on capital. It has also stood out for being more immune to tariff threats in recent times due to the domestic facing services business.

While structural tailwinds remain, not all players are taking the same path to growth. In this report, we take a look at the key listed players in the diagnostics space and the different playbooks they are following to deliver growth.

Dr Lal Pathlabs – The market leader’s calibrated expansion strategy

The undisputed leader among the listed players is Dr Lal Pathlabs (DLPL) by a large margin both in terms of market capitalisation as well as revenue. This pathology-focussed chain that offers basic radiology services as well, has its roots in Delhi NCR which till today remains its strong hold. It also boasts of the largest network of labs.

But 4-year revenue CAGR for DLPL at 11.4% has lagged smaller players like Vijaya, Krsnaa and Suraksha that have all clocked over 15%. Does this imply the industry leader has reached maturity? DLPL’s approach to geographical diversification and ramp up in specialised testing tells us otherwise.

Geographical diversification

Even as DLPL prioritises deepening its presence into Tier 2 and below in the North, the company is moving beyond its home turf both organically and inorganically. The West and especially the South are known to be more lucrative markets. The company is therefore ramping up its ecosystem in the South with a Bengaluru Reference Lab and a network of Hub & Satellite labs. It also commissioned a regional reference lab in Mumbai in 2023.

Its most notable acquisition was Suburban Diagnostics (2021), a strong player in the West where Metropolis Healthcare dominates. Other key acquisitions were Chan Re in Bangalore and Bindish in Jamnagar, both in 2020.

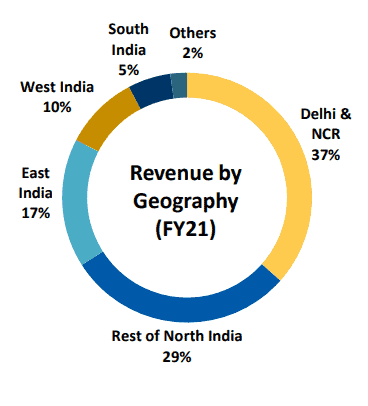

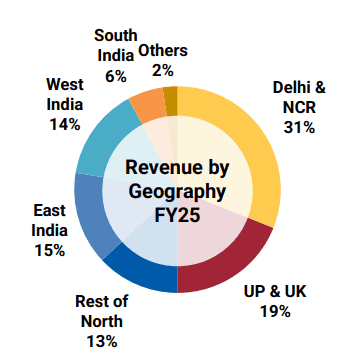

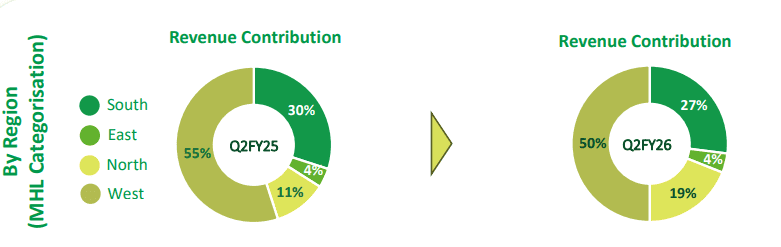

This is leading to less North-skewed revenue split (66% from the North in FY 21 versus 50% in Q2 FY 26).

Revenue split by geography FY 21 vs. Q2 FY 26

Source: Company presentations FY 21 vs. Q2 FY 26

While the pace of acquisitions may seem stalled, lately the focus has been on completing Suburban’s integration. The company sits on a healthy cash balance of Rs. 816 crores as of September 2025 and is scouting for a suitable acquisition candidate in the South. The healthy cash position will allow it to take the inorganic route without weighing on the balance sheet.

The right acquisition in the south (a region with greater awareness, affluence, preference for quality over price competitiveness and the highest density of doctors, nurses and beds per 10,000, per this CRISIL report) could mean a major boost offering scope for both growth and premiumisation.

Specialised testing boost

DLPL uses its bundled test offering ‘Swasthfit’ to drive growth volume, now accounting for 26% of revenue in Q2 FY 26 from 16.9% in Q4 FY 21. Specialised and super specialised testing has been Metropolis’ forte. However, Dr. Lal Pathlabs has ramped up its offerings here and extended bundling to these tests.

Latest milestones include:

- Establishment of specialty verticals: Genevolve (genomics), L-CoRD (reproductive diagnostics), L-ACE (auto-immune disorders).

- Being the first diagnostic chain in South Asia to offer amyloidosis testing

In FY 25 alone the company added 80 high end tests to its portfolio. The company has also been bitten by the AI bug and made an industry-first move in using AI in certain cancer screening tests.

Radiology pilot

While traditionally pathology focussed, the company is running a pilot offering high end radiology services (CT and MRI) at one center in Delhi NCR. Based on the outcome, it plans to expand to a few more centers though full scale up is not yet being considered.

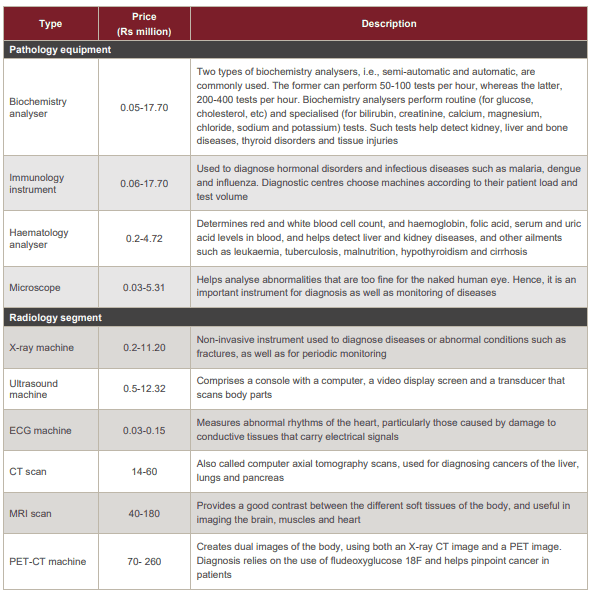

Radiology equipment costs far more than pathology equipment with even a refurbished PET CT Scan machine costing upwards of Rs. 1.5 crores and a new one costing upwards of Rs. 5 crores. Below is the indicative cost of equipment for pathology vs. radiology.

Source: CRISIL report referred to in RHP of Suraksha Diagnostic

A full rollout would therefore be far more capital intensive than DLPL’s current model potentially affecting margins and return ratios if utilisation rates and pricing are not high enough. What mitigates this risk is DLPL’s prudent capital allocation track record, healthy balance sheet and above all a carefully calibrated approach to such initiatives.

Metropolis Healthcare’s ‘string of pearls’

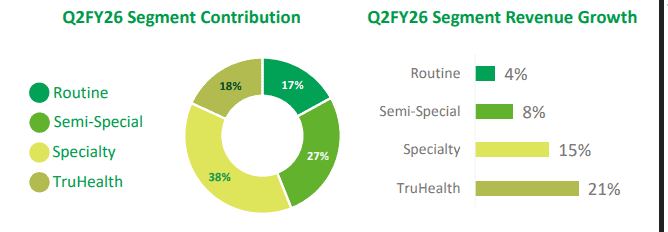

Metropolis Healthcare (Metropolis) has its roots and strength in the Western region. It is also known for its focus on specialised and super specialised testing which accounted for 58% of revenue in FY 21. While it is ramping up its bundled offering ‘TruHealth’, speciality and semi specialty still account for a bulk of revenue.

Metropolis has taken an approach to inorganic expansion that contrasts with DLPLs calibrated strategy, terming its own approach a ‘String of Pearls’.

At the end of FY 21, Metropolis was a zero debt company with a healthy cash position of Rs. 421 crores. In the ensuing years, the company took on debt of Rs. 300 crores to fund the Hitech acquisition (South focused chain that gave Metropolis a strong footing in TN and neighbouring states), which has since been repaid. The cash position however has been depleted to just Rs. 60 crores. Metropolis has been on an acquisition spree. The important acquisitions were:

- Core Diagnostics – an oncology‑focused company

- Ambika Pathology Laboratory – Kolhapur‑based chain

- Dr Ahuja’s Pathology and Imaging center – Dehradun

- Scientific Pathology – a leading diagnostics chain in Agra

With these acquisitions the share of the North in the revenue mix has jumped from 8% at the end of FY 22 to 19% in Q2 FY26.

Metropolis intends to build on this momentum and accelerate expansion across the North.

While this aggressive approach has driven growth, it has eaten into cash and chipped away at return ratios. RoCE, which was over 30% in FY 21 and ahead of DLPL, now stands at 14.7% as capex and integration costs have outpaced returns. Goodwill stands at Rs. 664.4 crores versus just 90 crores at the end of FY 21

Core broke even only in Q4 FY 25 and thereafter yielded low to high single digit margins in Q1 and Q2 FY 26. Metropolis aims to bring Core to its profitability level in about 3 years.

The company has also invested in ramping up its lab network and collection centers from 167 labs and 3,854 collection centers at the end of H1 FY 24 to 221 labs and over 4,600 centers today. Operating margins have been steadily declining from the FY 21 high, but the worst seems to be over with margins picking up in Q1 and Q2 FY 26.

Management stated that focus for the current year remains margin expansion and operating leverage with multiple levers for better cost controls, improved test mix, automation benefits and productivity gains. They are not planning new acquisitions over the next 6 to 9 months, giving the balance sheet some respite.

Basic radiology services (X-ray, ultrasound, 2D Echo and ECG, etc.) which are currently available at 35 centers across 5 cities are also going to be promoted to drive growth. Metropolis also participates in running clinical trials for pharma companies. Though a negligible portion of revenue at this point, could give a kicker to top line and margins as the clinical trials landscape in India matures.

Krsnaa – Pivot from B2G to B2C?

Krsnaa Diagnostics Limited (Krsnaa) listed in 2021 offering a unique business model with its distinct B2G focus. At the time of its IPO, Krsnaa derived 70% of its revenue from PPP contracts and this has grown to 75%.

The Government led PPP model involves diagnostics players entering into a public private partnership agreement with the Government after a tendering process. This agreement with Central /State or municipal governments is usually to provide specific diagnostic services (pathology, radiology, or both). Services are provided at government-fixed rates with escalation clauses.

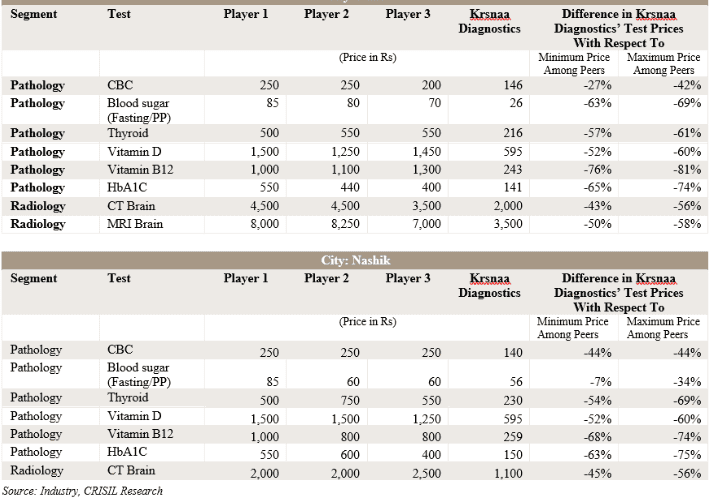

These PPP contracts cap the topline since the pricing is at a significant discount to what other players offer. Krsnaa’s RHP places this differential at upwards of 40% and recent company presentations place the differential at upwards of 70% in many cases.

Source: RHP page 135

However, it brings advantages like the government providing concessional/rent free space, capital infusion and financial concessions. Perhaps the biggest advantage is attachment to hospitals/health centers ensuring a captive customer base with minimal marketing spend (just 0.27% of sales versus 2-3% for peers).

Krsnaa also doesn’t spend on doctor referral fees and rentals, which helps maintain margins at par with peers despite significantly lower pricing.

PPP contracts usually have a 2- to 10-year tenure (longer for radiology, shorter for pathology) providing revenue visibility. Renewal at the end of tenure is not that challenging, due to existing investments which lets Krsnaa bid competitively.

The PPP opportunity was estimated at Rs. 9,500 crore per Krsnaa’s 2021 listing documents with Krsnaa being the dominant player. Krsnaa has a bid win ratio exceeding 70% and operates in 18 states and union territories, with penetration primarily in non-metros and tier-II and tier-III towns. This offers Krsnaa a measure of protection against price competition, which is most intense in the metros.

To support its far-flung operations, Krsnaa has a tele radiology reporting hub in Pune that processes large volumes of images and provides radiologist reports, ensuring a quick turnaround time.

But this model has challenges. Payments from government entities take longer than B2C and even B2B clients. Days receivable stood at 152 days at end of FY 25 versus all other listed peers’ far lower levels. The management also attributed this to new payment system implementation and natural disasters, and hopes to shrink it to 100 days by the end of FY 26.

Despite management’s assertion of zero bad debts, instances where Krsnaa halted operations due to unpaid receivables are concerning.

But this dynamic could change. Krsnaa is adding a ‘retail’ business layer using its existing infrastructure. Retail business contribution jumped from 1% of total revenue in Q2 FY 25 to 8% in Q2 FY 26. Management targets ramping to 15-20% in coming year with Rs. 200 crore revenue in 3 years, aspiring for 40% of revenue over 5 years. The retail segment, priced higher than PPP but around 20% lower than competitor rates, has better margins minus the receivables challenges.

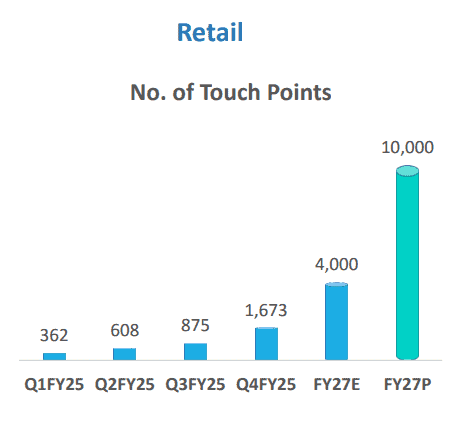

In the last year, Krsnaa rapidly expanded its retail footprint to over 2,800 touch points via asset light partnership strategy. As per Q2 FY 26 earnings call, this segment hasn’t broken even yet. This is expected at a Rs. 100 crore revenue, the target for the coming year. While Krsnaa had spoken of these plans in November 2022, we are only seeing a meaningful contribution from this segment in recent quarters. Currently Krsnaa is operationalising retail presence in 4 states where its brand recall is the best.

Krsnaa is not losing sight of PPP business—the Rajasthan PPP termed India’s largest diagnostic PPP project is being rolled out along with a Maharashtra radiology project implementing 15 MRI centers. Krsnaa is also exploring vendor-financed pay-per-use equipment models which could lift return ratios.

Vijaya – A premium regional player

Among India’s listed diagnostic chains, Vijaya Diagnostic Centre (Vijaya) stands out for choosing quality and margins over scale and speed. While peers race to build national footprints through aggressive acquisitions, Vijaya has quietly built a regional fortress that delivers industry-leading margins. Its business model is built around the following pillars.

Company-Owned, Company-Operated (COCO)

Vijaya owns and directly manages virtually all its diagnostic centers unlike competitors who use franchisees or asset-light partnerships to expand rapidly. (Viajaya too follows the hub and spoke model that the rest of the industry does). This naturally means higher capital requirements per centre, but it has also meant high quality standards. The company’s fixed asset turnover ratio of 0.67 (lowest among peers) reflects this capital intensity.

Radiology differentiation

Vijaya’s founder, Dr. Surendranath Reddy is a respected radiologist with 30+ years of credibility in the Andhra Pradesh and Telangana medical community. This translates into business through doctor referrals, ability to attract quality radiologists, and reputation for handling complex cases and also in its ability to command premium pricing. Marketing efficiency follows naturally. Vijaya spends just 1.11% of sales on advertising versus 2-3% for peers.

This has meant that Vijaya has a strong presence in radiology (roughly one-third of revenue) as against DLPL and Metropolis. Imaging commands higher prices and creates stickier doctor relationships. Vijaya also enjoys lower equipment costs than peers due to stronger bargaining power with manufacturers, an advantage considering the capital intensive model that the company follows.

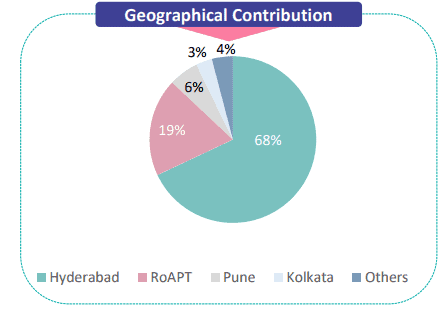

B2C & regional focus

Over 90% of Vijaya’s revenue comes directly from patients (B2C)Vijaya dominates in the Hyderabad market and is methodically expanding into Bangalore, Kolkata/West Bengal (3+ hubs in FY25, 2 more planned), Pune, and Tier-2 cities in Andhra Pradesh and Telangana. Acquisition of Medinova provided entry into East and West markets.

The combination of quality, premium pricing and founder’s reputation has resulted in Vijaya delivering 40%+ EBITDA margins consistently even during aggressive expansion phases. With zero debt on its balance sheet despite its asset heavy operations, Viajaya has managed a ROCE of 20.64% in FY 25 second only to DLPL.

The drawback is that Vijaya remains heavily dependent on South India, particularly Andhra Pradesh and Telangana. While diversification into Bangalore, Kolkata, and Pune is underway, these are still early-stage markets. The management commentary that Hyderabad is now “saturated” is telling. The company’s strongest market, where it has the deepest moat, has limited growth runway. Future growth must come from new geographies where Vijaya lacks Dr. Reddy’s personal network effects. Early signs in Kolkata are positive, but execution in markets without the founder’s relationships is key.

While 4-year revenue CAGR is over 16%, it could get more challenging to maintain this clip as Vijaya grows beyond its home turf where brand equity is strong. The COCO model too could ensure that growth only happens at a measured pace.

Suraksha – Integrated diagnostics in an underpenetrated market

Suraksha Diagnostic, which listed just a year ago in December 2024, has a business built around Eastern India – a significantly under-penetrated market. As a dominant player in Kolkata, the company gets an enviable growth runway. With a market cap of just Rs. 1,523 crores and FY25 sales of Rs. 276 crores, Suraksha is the smallest among listed diagnostic peers. The company operates 8 labs, 63 diagnostic centers, and 173 collection centers as of Q2 FY26, maintaining tight geographic focus.

What sets Suraksha apart is its integrated clinic model. Unlike pure-play diagnostic chains, Suraksha offers pathology, radiology, and doctor consultations under one roof. This means patients can get tested, receive results, and consult with a physician about next steps—all at Suraksha. This integrated approach drives higher revenue per patient and creates stickier customer relationships, though it also adds operational complexity compared to testing-only models.

The company is also making additional moves to differentiate. First, the July 2025 launch of Suraksha Genomics positions it in advanced genetic and molecular testing. Second, the Fetomat acquisition brings fetal medicine expertise, with plans to roll out these specialized services across existing Suraksha centers. Both moves aim to establish specialty niches that command premium pricing and create barriers to competition.

Management’s geographic strategy is to dominate the East and selectively expand into adjacent states and the “practically vacant” Northeast. Suraksha selectively takes on PPP contracts but the focus remains on higher-margin B2C business. Suraksha’s improving ROCE profile (from 7.6% in FY 21 to 18.4% in FY 25) shows that the business is maturing.

Valuation & Investment Considerations

The primary stand-out theme remains the fragmented nature of industry and an inevitable consolidation with players like Dr. Lalpath Labs and Metropolis leading the process. This is playing out through distinctly different strategic playbooks:

- DLPL – calibrated geographic diversification and specialty depth from a position of market leadership strength

- Metropolis – aggressive multi-regional consolidation

- Krsnaa – attempting a transformation from B2G to a more balanced B2G-B2C

- Vijaya – leverage premium positioning and operational excellence for controlled expansion

- Suraksha – builds regional dominance with selective geographic expansion

While this report covers the listed players, we have not delved into Thyrocare (also a listed player), which was acquired by Pharmeasy in the aftermath of Covid. Thyrocare is also thriving though it saw deteriorating numbers in the interim and is trying to get back on track. It is at a similar size of Krsnaa in revenue but revenue CAGR in the last 3 years has only been 5%. Promoter Pharmeasy recently sold 10% stake in Thyrocare in the open market (and pledged over 80%) due to its own financial woes, and to that extent the playbook for Thyrocare is not clear.

The market is gearing up for the debut of another diagnostic chain Neuberg Diagnostics, possibly in the new year. Agilus Diagnostics (formerly SRL Laboratories which then acquired DDRC to become DDRC SRL and was recently rebranded as Agilus) filed a DRHP but shelved its plans to list.

The sector’s 9.2% projected CAGR masks significant variance in individual company growth trajectories which range between 7%-15%. Key success factors will include:

- Execution on geographic expansion plans without margin dilution

- Ability to successfully integrate inorganic acquisitions

- Capital allocation discipline, balancing growth and returns

In our view Dr Lal Pathlabs commands a premium valuation with its industry dominant position, strong balance sheet and track record of prudent capital allocation all of which have resulted in an EPS CAGR of 42% in the last two years. ROCE too is back on an uptick after hitting a low in FY 23. A calibrated approach to expansion also assures us that growth will not come at the expense of margins.

In contrast, Metropolis with a slightly more aggressive approach bears watching – margin recovery remains key in the near term along with balance sheet impact as the company embarks on more acquisitions and expansions. A favourable execution history mitigates the risk that growth will compromise financials.

Below the line of these two are the players with distinct focus. Krsnaa is looking to make a major tweak to its business model and hence offers a tactical opportunity with its retail pivot showing encouraging signs. Its receivables heavy balance sheet is likely pulling valuations down to attractive levels provided the retail pivot materialises.

Vijaya with its resilient margins and focus on quality make it an attractive proposition but given challenges on replicating its model outside of its home turf, the PE of 68 may be stretched. Suraksha though much smaller in size offers a doorway to the under-penetrated Eastern market and even less penetrated North-East.

The sector’s structural tailwinds provide a favorable backdrop for multiple winners, though execution differentiation will be key. Check out Prime Stocks to know our pick in this space.

The securities quoted are for illustration purposes only and are not recommendatory.

8 thoughts on “India’s Diagnostics Sector – Five labs, five different playbooks!”

Your thoughts on how this industry will be affected by the entry of Amazon Diagnostics please? Because some of these stocks fell on this news.

Hello Sir,

Thanks for the query. Yes you are right that some of these stocks did correct when Amazon announced the launch of its diagnostics services in June. This is likely on account of the anticipated disruption potential that a player like Amazon could unleash. However, taking a closer look – first, Amazon offers only a subset of the services that any of the players we have covered in our report offers, catering primarily to the home collection services market with differentiation being speed (in both booking and getting the results).

It has also partnered with Orange Healthlabs ( a very promising player to watch – for this offering currently in limited geographies. This also means scalability is tied to Orange Healthlabs scalability. We have also seen how customers do tend to be brand loyal in home geographies (like DLPL in Delhi NCR, Metropolis in the West and Vijaya in its home turf of AP & Telangana). Expanding beyond their home turf has not been as simple as offering speed and convenience.

We have also seen in the past that price based competition is not sustainable.

A key point to note is that the diagnostics space has enough room for all the players to grow given the growth expectations and scope for consolidation by organised players. While we do not have revenue numbers to gauge how well Amazon Diagnostics has fared so far, we can see that the players whose stock prices did correct have since recovered. Key listed players also delivered a steady performance in the last quarter. So for now we don’t see this as a cause for concern for the listed players but will be watching it closely.

Thanks

Thanks ma’am for your detailed and quick response 😊

Hello Mam,

With this timely article, thanks for doubling down on your “Buy” call on Dr. Lal Pathlabs.

Dr Path labs in recommended stock list but down by approx 40 -50 % , does PI still maintain the buy signal

or if some one with high risk which among the 5 here seems promising

Hello Sir, The price movement reflects the broader correction we’ve seen across mid and small-cap segments. Our fundamental view on the stock remains consistent with the analysis shared on Prime Stocks.

Thanks

There are lot of unlisted players in the market but growing at a good pace – Neuberg Diagnostics, Aarthi Scans & Labs to be specific in Chennai. Have we considered unlisted players and platform players – Apollo diagnostics (both pharmacy and diagnostics) and Tata 1 mg and their growth rate. Can you please throw light on this as well ?

For the purposes of this report, we have considered only the listed players. – thanks, Bhavana

Comments are closed.