With the Iran war creating uncertainty around equity returns in the near term, many investors are now fans of multi-asset funds. Instead of taking a risk with equities right now, they think, why not buy a multi-asset fund (MAF) which can get me a return in any kind of market?

They seem to believe that MAFs are an all-weather product and that AMCs have some kind of magic formula to figure out whether equities, debt or gold/silver will do well in any given period and max out allocation to that asset, in advance, in their MAF. This is an erroneous belief.

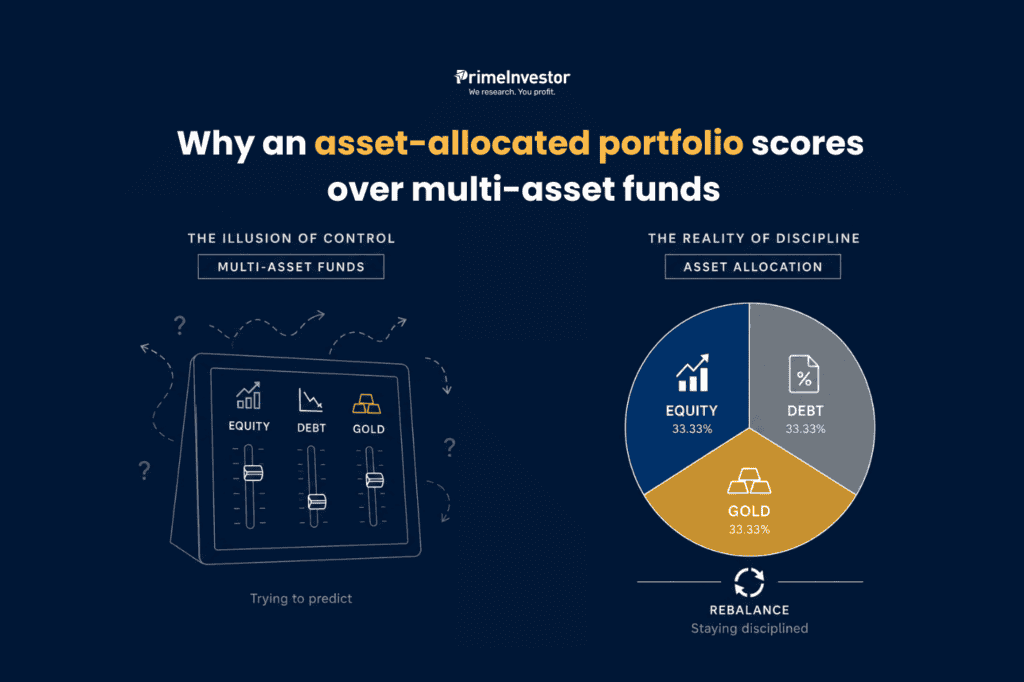

At Primeinvestor.in, we are diehard advocates of setting a fixed asset allocation between equities, debt and gold in your portfolio and sticking to it. This is the approach we follow in Prime Vision, our MF-based PMS strategy.

Here are five good reasons why we think multi-asset funds can’t beat this approach.

#1 No crystal ball

Many investors assume that in multi-asset funds, the fund manager makes astute timing calls to invest only in outperforming asset classes. This is a wrong understanding of this category.

To max out allocations to outperforming assets, a fund manager will need to know in advance whether equity, debt or gold/silver will be the chart-topper in the coming months. This requires a crystal ball and not fund management skills.

In January 2021, the Nifty50 was taking a breather at 14K levels after rebounding 70% from its Covid lows. It traded at a PE of over 35 times on beaten-down earnings. At that point, no fund manager however seasoned, could have told you that it would shoot up by another 85% in the next three years to hit 26K, powered by a scorching earnings recovery. Yet, that’s what happened.

In May 2021 at the peak of Covid gloom, if you had asked bond market gurus the outlook for interest rates, they are likely to have predicted that rates would lie low for a while. Yet, the lowest point in the 10-year g-sec yield was in May 2021 at 5.8%. From there, it shot up to 7.5% in the next 12 months.

Everyone knows that gold is a hedge against Black Swan events such as wars and oil shocks. Yet, global gold prices delivered their biggest gains in 2026 in the month of January (up 25%) when there were no Black Swans visible. From the end of February, when the Iran war began, gold is down some 15%.

All this goes to show that predicting the performance of an asset class in advance is tough even for accomplished managers. This difference in market assessment is evident in the asset allocation patterns in the funds.

Consider the April 2026 portfolios of the MAF category. The highest debt allocation stands at 43% and the lowest at just about 1%. Half the category holds less than 10% in debt.

Funds such as Kotak Multi Asset Fund and Baroda BNP Paribas Multi Asset are more aggressive with equity allocation of around 70%. Others such as ICICI Pru Multi Asset and Tata Multi Asset are less so at about 62%. Those such as WhiteOak Multi Asset, SBI Multi Asset and Capitalmind Multi Asset are even lower at less than 45%. Commodity and REIT/InVIT exposure are similarly wide-ranging among the funds.

This divergence in views apart, MAFs are also not similar in basic construct. Some funds aim to specifically be equity-oriented (for tax purposes) by using derivative exposures – which means they are not truly ‘multi-asset’ and they just hedge equity when risks may be high. Others do a balancing act with a minimum 35% in equity and the rest in debt and commodities. Still others hold equity and debt steady while taking periodic punts on gold or silver for returns.

Therefore, all MAFs are not equal and cannot be viewed from the angle of providing your portfolio with asset allocation. Depending on each one’s strategy, the return potential and asset allocation will be different. If equity markets do outperform all other assets over the next 5 years, MAFs are unlikely to outdo an equity-oriented portfolio.

(Read this earlier article to know how MAFs really operate).

#2 Uncertain returns and taxation

Thanks to SEBI’s categorisation rules, selecting a specific from an equity or debt category is now straight-forward. You can compare the fund’s risk-return metrics to its peers in the category and to its benchmark, apply qualitative filters and make your choice.

However, with varying allocations to equity, debt and commodities, multi-asset funds cannot be clumped together as a category and compared. As of May 16, for instance, one-year returns on MAFs ranged all the way from 5% to 25%, their 3-year returns varied between 11% and 25% and 5-year returns ranged from 10% to 21% CAGR. To really understand why one multi-asset fund delivered only 10% CAGR while another managed 21%, you need to dive deep into its asset allocation mandate and how it managed them.

The varying equity proportions in MAFs also make them hard to pin down into a tax category – whether equity-oriented, debt-oriented or requiring fund-of-funds treatment.

#3 Jack of all trades

MAFs require you to bet on a single AMC for all your asset needs – whether in equity debt or commodities. The net result is that you end up compromising somewhere.

One, not all AMCs excel in both equity and debt calls. If you choose MAF from an AMC that excels at equities, its debt calls or gold calls may not be great. If you choose a debt expert, you may miss out on equity skills.

Two, by relying on a single fund for equity, debt and gold, you may be missing out on good outperformers in equity funds and debt funds. You may diluting the impact of different categories such as midcaps or smallcaps.

Therefore, maintaining your own asset allocation helps you own the best funds in the equity, debt and gold/silver ETFs from different AMCs excelling in each asset class.

Any sensible investor would also hesitate to entrust his entire portfolio to a single scheme and fund manager. Therefore, most folks end up owning MAFs as just one of their funds. This defeats the purpose of using them as an asset allocation product.

#4 FOF inefficiency

Adding to the disadvantage of a single AMC for all assets, some MAFs also operate on a Fund of Funds structure, where they simply invest in in-house funds. This also has two impacts. One, it adds on an additional layer of costs and subjects investors to inefficient FOF taxation which can be avoided by directly going for the funds themselves.

Two, it may force investors to hold underperforming funds because the FoF manager calls the shots here. The same problem as above – not all AMCs have above-average funds in equity and debt – holds here.

Blending your own equity, debt, and gold gives you much more flexibility.

#5 Behavioural overhang

One of the biggest advantages of disciplined asset allocation is that it works against the human tendency to chase rising assets and get out of underperforming ones. Maintaining a portfolio with fixed asset allocation puts a rule-based framework in place for making rebalancing calls, without requiring any skill. Once you decide to go with a steady-state allocation between equity, debt and commodities, you automatically get into the habit of selling assets that outperform and re-deploying that money into assets that have lagged.

Multi-asset funds are bound by no such rules. SEBI rules only require MAFs to maintain a minimum 10% in any three assets (usually equity, debt and commodities with REITs recently making an entry). With no rule-based rebalancing, human biases of the fund manager can very easily creep into asset allocation decisions, prompting them to chase outperforming assets and shun lagging ones.

Clearly therefore, owning a portfolio of mutual funds from different AMCs, with a steady-state asset allocation that suits your personal risk profile, is a far better approach.

Markets move in cycles. Asset allocation helps portfolios endure them.

Our Prime Vision PMS portfolios combine equity, debt, and gold in carefully calibrated allocations designed to create more resilient investing outcomes across different market environments.

Learn more about Prime Vision

6 thoughts on “Why an asset-allocated portfolio scores over multi-asset funds”

Why is static MAF funds like Zerodha Multi asset fund or Edelweiss-Nifty-LargeMidcap250-Plus-8-13-yr-G-Sec-7030-Index taken into consideration here?

This article is not complete without explaining about these funds 🙂

We have written a separate analysis of the hybrid passive fund. On static MAF there is still the problem of using a single AMC and fund for your entire asset allocation.

Good insights into this MF product which is in flavour today. Is a Balanced Advantage Fund a better bet than an MAF ?

A balanced advantage fund will have a equity oriented structure. But it still substitute for asset allocation at a portfolio level because you can’t put your entire portfolio in one scheme from one AMC.

Dear Aarati,

1. Have always followed your clear and simple asset allocation plan. No MAF. Risk assessment of self is always a crucial factor inspite of scientific methods available to arrive at a conclusion. An article analysing it may please be thought of; besides pointing out to everyone that how well your team manages and advises about it.

2. Thanks for providing more clarity on the issue.

Regards

Rajiv K Mendiratta

Thank you. Shall consider this article on risk profiling!