In September, we published an introductory report on the CRDMO sector in India. In Part II of this series, we analyse why India may be poised to benefit from a structural shift taking place, where the CRDMO work is flowing, and what makes for a good CRDMO partner.

While India’s pharmaceutical sector benefits from government PLI schemes promoting API self-reliance and attracting foreign investment, the real game-changer for the CRDMO space could lie in the China+1 opportunity—a structural shift that could change the growth trajectory of the sector for the better.

A birds’ eye view of the global CRDMO landscape

The US leads in global CRDMO work, as it is home to major pharmaceutical companies, and has conducive regulatory infrastructure and a sophisticated drug development ecosystem. But as we highlighted in part I of this series, the case for outsourcing is strong thanks to many factors that include cost pressures, slim success rates, lengthy and capital intensive process and more new drugs coming from smaller biotech firms.

For now, China commands the lion’s share of outsourced CRDMO work—second only to the US. China’s dominance stems from advantages that have been hard to match: API production at unmatched scale and cost, a vast talent pool, abundant capacity, and years of favorable regulatory support. US clients rely heavily on Chinese CRDMO firms, especially the large players. Wuxi Biologics, the leading CRDMO company in China and part of the Wuxi group, saw 57% of its $ 2,623 million revenue come from the US and another 23% from the EU in 2024. It signed on 151 new projects during the year with over half from the US. The cost dominance too is apparent – Wuxi Biologics steadily reports gross margins in excess of 40% with most Indian CRDMO players reporting EBITDA margins between 30% and 40%.

What’s changing

While the ‘China+1’ theme isn’t new, it came into prominence thanks to the pandemic. Supply chain vulnerabilities exposed during this time, combined with escalating geopolitical tensions, forced countries and companies to diversify their supply sources beyond China and the pharma sector is no exception.

Indian CRDMO players are naturally well-positioned to benefit from this with their cost advantages and availability of talent. Jefferies estimates the China+1 opportunity for India at $ 700 million annually in base case scenarios, with potential to reach $ 1.4 billion per annum.

The US Biosecure Act, which bars federally-funded biotech firms in the US from using certain Chinese manufacturers, could further accelerate this shift considering that the Chinese CRDMO firms derive over 50% of their revenue from the US.

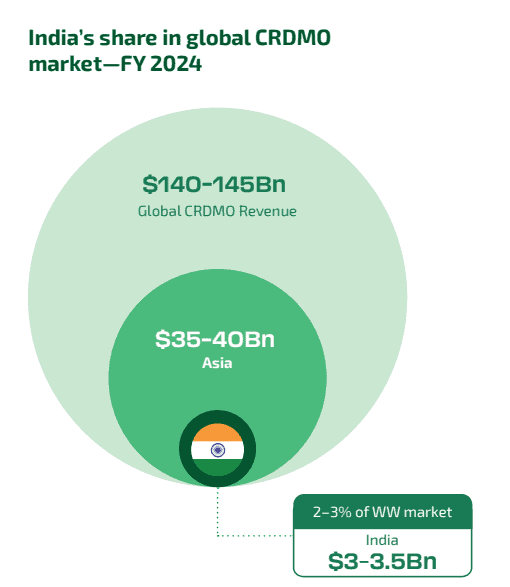

India’s CRDMO sector currently represents just 2-3% of the global market. It is however expected to grow at a faster clip than the CRDMO sector in the rest of the APAC. For example, Wuxi Biologics and Samsung Biologics, a leading player in the APAC with revenues higher than Wuxi both reported revenues in excess of $ 2,500 million. In contrast, the CDMO portion of the total revenue of Divi’s Laboratories would only be approximately $ 500 – 600 million.

Source: BCG report

With China+1 representing a long-term structural realignment rather than a temporary trend, the headroom for growth is significant.

Key success factors for a CRDMO player

While the opportunity may be clear and present, not all CRDMO players are equally capable of cashing in. The key success factors that set apart players are:

#1 Past track record

The business of researching and bringing new drugs to the market calls for adhering to high compliance requirements. Here are some of the key ones.

- Compliance with Good Clinical Practice (GCP) and Good Manufacturing Practice (GMP) standards in order to access regulated markets like the US and EU and meet the requirements of the US FDA, EMA and WHO.

- Adherence to GMP guidelines issued by Indian regulators (CDSCO).

- International Council for Harmonisation – Good Clinical Practice (ICH-GCP) a global regulatory standard that ensures ethical, high-quality clinical trials to protect patient rights and enhance data integrity.

- Data Integrity and IP right protection requirements.

- While the regulations surrounding clinical trials in India were once considered unconducive and unclear, that has been changing for the better with the advent of the New Drugs & Clinical Trials Rules, 2019 and hence these requirements have to be met too.

- Ethics committee approvals, informed consent procedures, and clinical trial registrations via Clinical Trials Registry – India (CTRI) for trials in India.

- Other and newer regulations that come up from time to time such as the ‘The EU AI Act’ that introduced a risk-based framework for AI systems, including high-risk categories that include medical devices.

For a CRDMO player, a clear understanding of these compliance requirements is essential to compete at the global market. A clean track record of successfully meeting all of these regulatory requirements is critical for a CRDMO player to not only retain existing clients but also onboard new ones.

#2 Capabilities in New Modalities

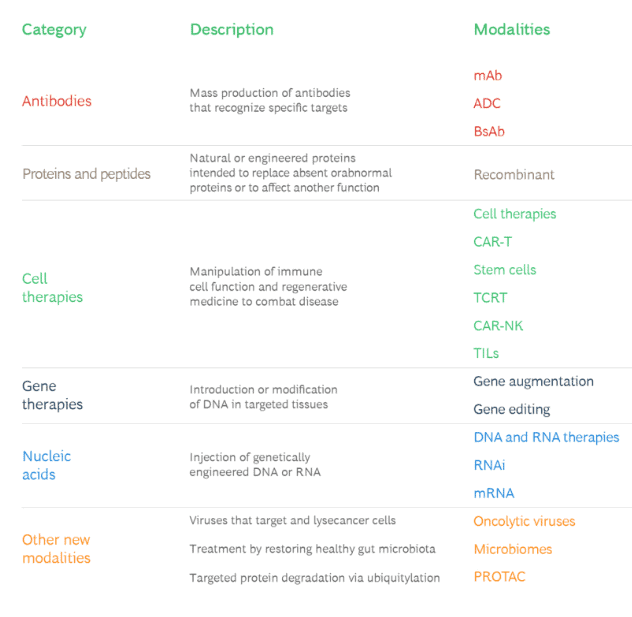

Industry reports and listing documents indicate a growing prevalence of newer and innovative modalities.

New modalities are a broad umbrella that includes innovative approaches to developing and delivering drugs. You might remember the mRNA-based Covid vaccine that was the topic of much discussion. More recently, GLP-1 weight-loss medications are all the rage. Both fall under the ambit of new modalities.

New modalities offer several benefits such as treating conditions that were till now hard to treat, treating diseases in a more targeted manner with minimal collateral damage and more. Born out of the biotech industry, these new modalities are slowly taking over and as per this BCG report, new modalities now account for 60% of the total pharma projected pipeline value, up from 57% in 2024. The study also notes that eight of the ten best-selling biopharma products in 2025 are new-modality drugs.

Broadly these new modalities fall under the following categories.

Source: BCG report

While Indian CRDMOs have a proven track record as far as simple small molecules are concerned, biologics and new modalities are a different ball game. They require a quick upgrade in skills and facilities. Some Indian CRDMO players are already upping their game.

- The CRDMO platform of Anthem Biosciences already comprises RNAi, ADC, Peptides, Lipids and Oligonucleotides.

- In Q1 FY 26, Sai Lifesciences inaugurated its Peptide Research Center at its Hyderabad R&D campus. The company also focuses on strengthening capabilities in complex peptides and emerging modalities and expanding capabilities in ADCs, TPDs, Peptides, CGTs, Oligos, and more. The share of these new modalities in revenue too went up from 4% in FY 22 to 7% in FY 25 for Sai Lifesciences.

- Divi’s Laboratories already supplies APIs that form the basis of these new modalities.

#3 Growing focus on ESG

‘Big Pharma’s’ sustainability commitments are cascading down the supply chain. Industry reports and earnings presentations of large players like Wuxi Biologics and Samsung Biologics reveal the growing importance of sustainability, and that this is one of the crucial aspects major pharmaceutical companies will look for in a CRDMO partner.

As a result, this is now emerging as a key success factor for CRDMOs. For this, pharma companies conduct sustainability audits in addition to those for compliance to GMP and similar checks that CRDMO partners have to undergo. These audits / inspections are either conducted by the pharma company themselves or by organisations such as the Pharmaceutical Supply Chain initiative (The Pharmaceutical Supply Chain Initiative (PSCI) or EcoVadis whose reports are in turn accessed by the pharmaceutical companies.

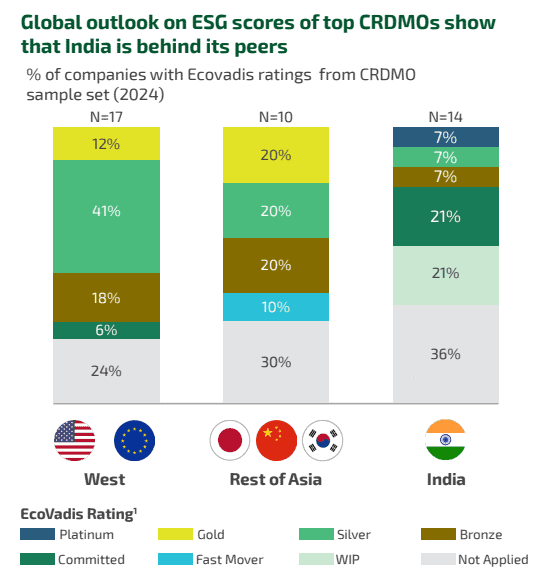

Complying with sustainability goals is not easy – they require capital investment and access to green utilities. A study by BCG in partnership with IPSO (Innovative Pharmaceutical Services Organisation – an industry body comprising 11 leading CRDMOs in India) indicates that Indian CRDMO firms lag behind their peers in the rest of the world in this area.

Source: BCG report

This is therefore naturally emerging as a priority for CRDMO players in India and the listed players showcase their efforts in this direction in their annual and other reports.

- Divi’s Laboratories lays out sustainability goals for 2030 that include specific measurable carbon footprint reduction, water conservation, energy conservation and waste management.

- Cohance Lifesciences highlights its efforts and investments in this direction including that its manufacturing sites operate advanced Effluent Treatment Plants with Zero Liquid Discharge capabilities and that waste is handled responsibly.

- Sai Lifesciences has a ‘GoGreen Plus’ logistics initiative with DHL for low-emission pharma shipments. This collaboration utilizes Sustainable Aviation Fuel (SAF) to reduce greenhouse gas emissions by up to 90% for the company’s shipments. This initiative uses an approach called ‘insetting’ where emissions are reduced directly within the logistics chain by using sustainable fuels and other methods, rather than relying on carbon offsetting.

CRDMO players that get their sustainability act on point, stand to have an edge.

What could come in the way?

#1 China +1 not easy

While the US Senate has endorsed the Biosecure Act, it is a watered down version. It seeks to prevent companies reliant on federal contracts and funding from working with certain Chinese biotechs of concern and also prevent select Chinese companies from accessing U.S. government funding.

It now adopts a broad definition of ‘companies of concern’ as those that are an extension of the Chinese military as well as firms that answer to a “foreign adversary” or otherwise pose a national security risk to the United States, as against the earlier version that specifically named players like Wuxi. This could leave a lot of wiggle room for Chinese players. A resumption of US-China trade talks and inking of a trade deal could also lead to a thaw in the relationship and further dilution of this Act.

China has grown its capabilities in new modalities rapidly and has positioned itself as a hub for new modality innovation. This BCG study states that more than 30% of assets in global antibody and cell therapy pipelines originate there. Further, several Chinese origin new modality assets are already on the market. While innovators do seek to diversify away from China, it would be naive to assume that this would happen overnight. Challengers such as India have some way to go before they can replicate the robust ecosystem that China has in place for the CRDMO sector including targeted talent development and favourable regulations.

Further, there are long timelines for ongoing projects with funding already tied up. Indian CRDMO players are still at the early stage of this transition (enquiry stage), with the shift likely to be gradual.

#2 Not all new modalities are taking off

Company annual reports and earnings calls, all indicate that significant investments are being made toward ramping up capacities in new modalities. However, not all of these are taking off.

BCG analysis reveals that some established new modalities like mAbs, ADCs, BsAbs, recombinants, and CAR-T show growth, whereas others like gene, mRNA, and other cell therapies, have stalled. Where a CRDMO player is ramping up capacity will be key to determining if it will be a hit or a miss.

#3 Biotech funding winter

A large part of the new modalities has their roots in smaller biotech companies that have been the beneficiary of the biotech funding boom that peaked in 2021 thanks to the pandemic. Since then things have not been so rosy and these firms are increasingly facing funding challenges.

What should a stock investor consider?

While the Indian CRDMO sector has come a long way from being just a low-cost supplier to a key partner, picking a stock to bet on is far from straightforward.

- While we may have all heard about Divi’s Laboratories, the industry is fragmented and has many small players. It is important to identify established players with proven models and scale.

- Each organisation can also have a different business model by virtue of the segment of the value chain they focus on. Some focus on the research end of the spectrum whereas others focus on the more volume driven manufacturing end.

- Revenue models too can vary from client to client. Predetermined fees are common in early-stage projects. In some cases, the fee payments are tied to specific milestones. Sometimes, the CRDMO partner sets up or runs a dedicated facility where the fee is a combination of fixed and variable. Contracts could also be end to end spanning over several years / decades or involve sharing risks / rewards. This means revenue streams are not steady or predictable.

- Given slim overall success rates, there is no guarantee that a project will make it to the end of the drug development life cycle. For instance, in the case of Wuxi Biologics, cancellation of a 20-year vaccine project caused a YoY decline in service backlog in 2024.

- The nature of the CRDMO business is such that confidentiality is key and the company cannot share too much detail around individual client contracts and pipeline visibility. Aspects such as client concentration get difficult to assess for investors. This is further amplified with smaller players who have concentrated clients. This means investing in these companies involves a little bit of shooting in the dark and relying on past track records.

- The business requires CRDMO partners to proactively build capabilities first and then generate revenue from them. This capacity build up also has to be done swiftly. This means an upfront capex with minimal details on revenue visibility. This is combined with the lumpy nature of revenue and long project lead times.

- Compliance issues arising out of inspections could very easily throw a spanner in the works.

- Stock prices for CDMO players can be volatile. To give an indication of how much, the standard deviation of a few of the well-known names is upwards of 2 (except Divi’s Laboratories and Syngene International that are above 1.5); the Nifty Pharma Index has a standard deviation of just 1.06. The stock price of Piramal Pharma went from a 1-year high of Rs. 307 in November 2024 to a low of Rs. 181 in February 2025. That’s a decline of over 40% in less than a year! Similarly, with Syngene International too.

Given the above, it is clear that the CRDMO space is not one where the companies are all homogenous. Picking a candidate here would require a bottom-up approach. We believe that the following would be the qualities that one should look for in spotting a CRDMO company to consider investing in.

- A large, diversified player: While this is not a hard and fast rule, a large player with a wider range of business and clients would deserve more points than a niche player focussing on a narrow modality or therapy area or set of clients. This is especially important given that the business tends to be confidential and only limited information is available on clients, contracts and end use-cases of projects being worked on. This is also important given that not all projects will make it from lab to pharmacy. Companies with diversified products and clients will help mitigate concentration risk.

- Capabilities in new modalities: Given the emergence of new modalities, a company with capabilities in these areas (especially the ones that are showing favourable signs) would ensure that it stays relevant in the future.

- Positive compliance track record: A close look at the regulatory compliance history to assess the compliance culture of the organisation is crucial as any negatives in this aspect can derail progress of projects. A good investment candidate would have a clean track record.

- Geographical diversification: While CDMO businesses are generally insulated from US tariffs on pharmaceuticals, given recent geopolitical events, diversification of revenue by geography too would be a plus.

- Financial health: Favourable metrics that demonstrate financial and operating leverage and non-negotiables like balance sheet strength are essential. Given the requirement of upfront investments, balance sheet strength and capital allocation track record of management are paramount.

Considering the nature of stock price volatility, CRDMO stocks are not for the faint of heart nor do they all lend themselves to a buy-and-hold strategy for long term compounding. Most of them are better used as tactical additions to a portfolio with limited exposure.

The securities quoted are for illustration purposes only and are not recommendatory.

Please refer to Prime Stocks for our stock recommendations.