As a mutual fund investor, most of you would have confronted this dilemma:

- your fund is underperforming or has received a Sell recommendation, but you’re sitting on substantial unrealized gains.

- The looming question is whether to cash out and face the tax implications and switch to another fund, or hold steady.

- Since you lose a good chunk on tax, you think the new investment has to make up for the entire loss of tax plus earn more. Is your concern overstated?

This article will equip you with a clear strategy for navigating this common yet challenging scenario, ensuring you’re prepared to make informed decisions when it matters most. A downloadable excel that we provide with this article will also help you make an impact analysis on the impact of switching funds or holding on.

Different scenarios with switching funds

When making financial decisions, we often focus on short-term outcomes, potentially overlooking crucial long-term implications. This tendency can cloud our judgement, especially when considering a fund switch. Let’s examine several scenarios to better understand and evaluate the extended consequences of such a move.

Case 1: Switching an Equity Fund

- You hold an equity fund with a market value of Rs.10 lakh.

- Your original cost was Rs.3 lakh. Unrealized capital gain is Rs.7 lakh.

- You’ve already used up the Rs.1.25 lakh exemption for equity capital gains, so any redemption will attract a 12.5% tax on gains.

You decide to move out of your poor performing fund to another fund (using lump sum). This switching will leave you with a tax bill of Rs.87,500 for the above scenario, shrinking your corpus by 8.75%. You invest this post-tax corpus into a new fund.

Now, let us see how this decision pans out 5 years from the new investment, as opposed to not making the switch at all and holding on to the old fund. We’ll assume:

- You plan to redeem the fund 5 years from now.

- The 12.5% tax rate and Rs.1.25 lakh exemption remain unchanged for equity capital gains.

- You expect to use up the Rs.1.25 lakh exemption by other investments, so future redemptions will be fully taxed.

- Both the old fund and the new fund you have switched into generate the same returns (11% per annum) over the next 5 years.

No Switch: If you had not moved out of the old fund in the first place, then your pre-tax corpus will be Rs.16.85 lakh, and after paying Rs.1.73 lakh in taxes, you’ll have Rs.15.12 lakh.

Post switch: You invested Rs.9.12 lakh (after Rs 87,500 taxes) into the new fund. In 5 years, your pre-tax corpus will be Rs.15.38 lakh if it grows at 11%. After paying Rs.78,000 in taxes, you’ll have Rs.14.59 lakh. This is about 3.5% lower than what you would have had you not switched in the first place. Please remember, in this case, we have assumed that the fund you switched into, earns the same return as your original fund (in reality you switch for better returns).

But if returns were unchanged, then you would have thought that your net loss is the tax paid the first time around – Rs 87,500 – or 8.75% lower corpus. But it turns out your corpus is lower by only 3.5%. Why is it so? This is because when you book out of the first fund and enter the new fund, your new investment cost (for tax purpose) is much higher at Rs 9.12 lakh, as opposed to the Rs 3 lakh in the case of no-switch. So since your cost base is higher, the tax you pay in the new fund is much lower. This partially makes up for the dent of tax outflow you had 5 years ago.

To summarise, in a scenario of switching to a new fund with the SAME returns, here’s what happens:

- Actual impact : Your market value of the new fund is lower by 3.5% on a post-tax basis. The corpus is lower simply because you had removed Rs 87,500 for paying tax (cash outflow) and reinvested only the rest. So this amount could not compound itself for 5 years, whereas it was comfortably seated in the corpus in the scenario of not switching at all.

- Tax efficiency : Since you paid 8.75% out of the corpus as taxes, you may have thought your new fund should make it up by earning that much more. However, even if the new fund delivers the same return, your corpus is lower by only 3.5% and not 8.75%. This is simply because of lower tax outflow in your new fund (higher cost base). So your loss is much lower than you feared.

- Break-even point : In reality, in this illustration, if your new fund earned just 11.85% (as opposed to 11% for the old fund), you would comfortably match the corpus of a ‘no switch’ scenario. Any return in the new fund over 11.85% means your switched corpus will be higher. In other words, the new fund has to generate just 0.85% more return per year to make up for the lost tax outflow.

Use the Excel sheet here to do your own numbers based on different scenarios

Case 2: Equity fund switch with different tax assumption

- You hold an equity fund with market value of Rs.10 lakh.

- Your investment was Rs.3 lakh. Unrealized capital gain is Rs.7 lakh.

- You’ve used Rs.75,000 of the capital gains exemption this year, leaving Rs.50,000 of the gains exempt from tax.

- You plan to redeem the fund 5 years from now.

- Assume the tax rate increases to 15% post (from 12.5% now) and you get an exemption of Rs.1.5 lakh (from Rs 1.25 lakh now) for equity capital gains in the future. Of this assume you have an unutilised amount of Rs 75,000.

- The current fund will generate 11% annually, and the new fund will generate 11.5%.

Use the excel sheet provided above for this scenario. You will see that switching will reduce your corpus by 8.13% today. However, in 5 years, your post tax corpus will be 0.43% more compared to holding the existing fund.

Case 3: Switching a Debt Fund

- You hold a debt fund worth Rs.10 lakh.

- Your investment was Rs.8 lakh. Unrealized capital gain is Rs.2 lakh.

- You’re planning to redeem this fund 5 years from now

- You’re in the 30% tax bracket now and expect to be in the same bracket in 5 years.

- You expect your current debt fund to generate 7% annual returns in the next 5 years

- You expect your new debt fund to generate 7.5% annual returns in the next 5 years

Switching will reduce your corpus by 6% today. However, your final post tax corpus will be 0.4% higher compared to holding the existing fund.

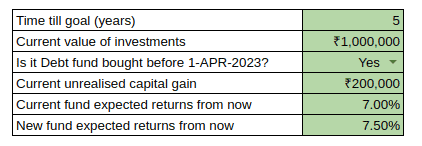

Case 4: Debt Fund Purchased Before April 2023

- You hold a debt fund worth Rs.10 lakh.

- Your investment was Rs.8 lakh. Unrealized capital gain is Rs.2 lakh.

- You’re planning to redeem this fund 5 years from now

- You bought this debt fund before April 1, 2023, making it eligible for a 12.5% capital gains tax.

- You’re in the 30% tax bracket now and expect to be in the same bracket in 5 years.

- You expect the current debt fund to generate 7% annual returns in the next 5 years

- You expect the new debt fund to generate 7.5% annual returns in the next 5 years

Switching will reduce your corpus by 2.5% today. Your final post tax corpus will be 4.14% lower compared to holding the current earlier fund without switching. In this case, the higher returns couldn’t make up for the losses, instead the losses expanded.

Case 5: Switching a Debt Fund while retirement is on the horizon

- You hold a debt fund worth Rs.10 lakh.

- Your investment was Rs.8 lakh. Unrealized capital gain is Rs.2 lakh.

- You’re in the 30% tax bracket now.

- You’re planning to redeem this fund 5 years from now

- To estimate tax slab and tax rates at the time of redemption:

- You’re planning to retire in 4 years

- You assume that your only taxable income will be interest income of Rs. 5 lakh 5 years from now.

- You expect maximum tax exempt income to be Rs.9 lakh (the slab up to which there is no tax) 5 years from now (this is Rs.7 lakh at present under New regime)

- Based on the above, you expect debt capital gains up to Rs.4 lakh will be tax free for you, rest to be taxed at 10%

- You expect your current debt fund to generate 7% annual returns in the next 5 years

- You expect your new debt fund to generate 7.5% annual returns in the next 5 years

Switching will reduce your corpus by 6% today. Your final post tax corpus will be 2.44% lower. The higher returns couldn’t make up for the tax lost in this case.

How to use the ‘Fund switch and tax impact analysis’ spreadsheet

If the calculations sound complicated, don’t worry—you can do this with minimal inputs using the spreadsheet we have mentioned earlier. Here’s a brief guide to using it:

Fund switch and tax impact analysis

1. Define Tax Estimates

- Enter the applicable exemptions and tax rates for your investment, both current and expected.

- For debt funds, if your income is taxable, enter the current exemption as 0 and input your income tax slab rate where the text capital gains tax rate is mentioned.

Notes:

Equity exemptions: Here, enter the capital gains exemption applicable to the particular investment in consideration. For example, currently exemption for equity capital gains is Rs.1.25 lakhs. If you already have Rs.1 lakh capital gains from selling stocks this financial year, enter Rs.25,000 that is available, as current exemption. Similarly, for future exemption also, you may enter a lower value to account for any other capital gains you may have.

Debt exemptions for retirement period: In the retirement period, if you think you will be in the 0% tax bracket; enter the exemption to capital gain as a value which is the estimated difference between tax free income and your taxable income at retirement. For example, if you estimate the income up to Rs.10 lakh will be having 0% tax payable at the time of your retirement and you expect to have an annuity income of Rs.7 lakh per year, and do not have any other taxable income, enter Rs.3 lakh as the exemption to capital gain.

If you think you’ll be in a specific tax bracket during the retirement period, enter exemption as 0 and enter the estimated tax slab in the tax rate.

Tax rates falling on multiple slabs: Sometimes, it is possible that the debt capital gains will push the marginal rate to the next slab; making parts of capital gains to be taxed at different rates. Accounting for this would further complicate the calculation, as a workaround, you may adjust the tax rate accordingly. For example, if you’re estimating the tax slabs applicable to you will be both 10 and 15%, you may enter 12% or 13% to account for that.

2. Define Investment Estimates

- Enter the holding period, current value, unrealized capital gains, and return estimates for both funds.

- For debt funds, purchased before April 1, 2023, select “Yes” in the dropdown. Set it as “No” for all other cases

The sheet will show the final post-tax corpuses and the change in corpus due to switching.

Conclusion

Switching triggers taxes, but in most cases, you’re paying part of the tax in advance, reducing future taxes. Whether to switch or not is a decision personal to you. It may seem that you’ll have to make a lot of assumptions to correctly estimate whether a switch is worth it and these assumptions may not materialise also. These assumptions broadly are:

- The capital gains tax rate or your own tax rate as applicable for different classes of funds

- The capital gains exemption available in future

- How much the new fund returns as opposed to the old fund

However, the key is not to make exact predictions, but to try various assumptions and arrive at a conclusion like “For this switch to be beneficial for me, the fund would likely have to generate 0.5% more!” Hope the method explained in this article will help you reach such conclusions.

31 thoughts on “How much do you lose by switching between funds?”

Thanks for this article. Switching from one fund to the other is easier said than done. One has to look at several factors, as has been pointed out in this article and in the comments too.

As a general strategy (not necessarily always), unless I need the money, I tend to hold on to the funds for ever. When I need the money, I redeem the amount first from the underperforming funds and then from the other funds, if required. I do not make fresh investments in the underperforming funds. If there is a management/product issue associated with an underperforming or even a performing fund, I redeem/ switch out quickly, irrespective of the tax implications.

There may not be any hard or fast rule on when to switch/ when not to switch. Had I switched out of ICICI Blue Chip fund in haste, I may have repented at leisure. Had I not switched out in haste from Franklin India ultra short bond fund in December 2019, I would have repented at leisure. There are quite a few funds that I switched out of, because of underperformance, but they subsequently started doing very well.

It all depends.

Thanks Bipin for sharing thoughts along with data and assumptions on this topic.

The biggest catch in the case of equity funds is that there’s no guarantee the new fund will do better. So this rebalancing exercise works best if your fund has underperformed over an extended period of time (say 2 or 3 years). Also, switching from your underperforming to the “best” performing fund, may actually be counter productive. The best performing fund has already had a good run and the fund picking strategy for the fund may got out of style (temporarily) in the market. Portfolio churn is the reason individual investors don’t see the high returns advertised by the funds.

Some years back ICICI Value Discovery Fund was underperforming a few years back after being top rated in the previous years, I exited the fund only to see the fund again start outperforming significantly. The style (value investing) was underperforming the market in general at the time, it wasn’t that the fund was not managed well.

In general, if my conviction a fund still holds I don’t exit, I just let my investment compound. For example, I still hold to my Mirae Asset Emerging BlueChip fund investments which have given me great returns over a decade or more even though Prime Investor has given a sell call. Instead, I just direct new investments to a recommended fund, this strategy works great especially if you’re regularly investing in SIPs.

Hi Bipin – this is a very helpful article. Thanks for the underlying efforts to create and share the excel file to compare scenarios. The key question in my mind in such scenarios is whether I am exiting the fund at a wrong time i.e. just when its strategy would reap benefit and if the current recommended funds would sustain to provide these returns in future as well. For instance, I could be holding a fund with a value strategy which would have underperformed in recent years but maybe it would do relatively better than growth oriented style going forward which I may miss out on by selling at this point and maybe buying growth oriented funds which may underperform going forward. Or maybe the fund’s under-performance was due to poor fund manager’s choice and there is a change in the fund manager which could revive its fortunes? Is there a way to attribute the fund’s outperformance or underperformance to different factors such as fund style/strategy and fund manager’s performance/calls? Any thoughts on addressing this dilemma would be welcome. Thanks.

Hello,

When a fund is underperforming due to an out-of-favour strategy, deciding whether to hold or switch can be complex. Here are two approaches to consider:

Simple follow Buy/Hold/Sell calls. Note that switching shouldn’t be based solely on performance or ratings. A sudden dip in performance might not immediately trigger a ‘Sell’ call, even if it affects the fund’s ratings. We take the fund’s strategy and market conditions into account before changing a call. This article explains the difference between ratings and calls.

Understand a fund’s strategy and be prepared to hold through periods of underperformance if they’re due to broader strategy trends rather than specific fund issues. In such cases, it’s beneficial for investors to diversify strategies or allocate more to broad markets, so the entire portfolio isn’t affected by a single strategy’s prolonged underperformance.

Hope this helps.

Thanks

The key sentence for me comes at the very end :

“Switching triggers taxes, but in most cases, you’re paying part of the tax in advance, reducing future taxes.”

Most people fail to understand this (from a majority of posts that I read on PI Community). This is like TDS from the salary – one should be happy paying every month from the in-hand salary, than to have to pay 1/3rd of the annual salary at the year end. I never worry about the taxes payable at the time of switch – as this is part of the taxes which I’ll be in any case having to pay to the Government at a later date.

The decision to switch should be based on strategy/rules and not on taxes – One wants to rebalance the asset allocation, one wants to move to debt for a goal that is approaching, one wants to move to a fund that is now performing better, one has to shuffle based on an registered investor advisor’s plan – or any other reason.

Thanks for a really good article!

Thank you for your feedback and sharing your views.

You’re right; taxes should not be the primary concern. Focusing solely on tax savings may lead to buying suboptimal products or avoiding necessary changes to the existing portfolio, even when the situation warrants it. There may be specific cases where taxes can unfavourably affect the outcome, as in example case 4. The article aims to encourage investors to make informed estimates rather than focusing solely on the tax aspect.

Thanks

Comments are closed.