India is in the midst of a transformation driven by large-scale government spending on urban infrastructure, roads, railways and industrial development. This investment cycle is, in turn, creating a favourable environment for a sector that is closely tied to infrastructure development – the construction & material handling equipment industry.

This is currently in a structural growth phase and expanding at a CAGR of about 8% (Source: ACE annual report 2025). We expect the construction equipment industry to report healthy growth in FY27, supported by a favourable base effect, as it recorded a decline in sales in FY 26 (down 13%). This apart, rising project scale and complexity are driving increased mechanisation in construction, with manual tasks increasingly replaced by equipment such as cranes, backhoe loaders, and forklifts. This shift is reinforced by demographic trends, as younger workers move away from labour-intensive roles, supporting sustained demand for construction equipment.

Within this context, Action Construction Equipment (ACE) represents a potential proxy for India’s infrastructure build-out. This smallcap stock has a marketcap of about Rs 10,900 crore. In this report, we review this stock, list out its positives and its risks.

Background

ACE is an India-based manufacturer of construction and material handling equipment, with a portfolio spanning cranes, backhoe loaders, forklifts, graders, and rollers. The company derives the majority of its revenues from equipment sales rather than rental income, serving clients across infrastructure, manufacturing, and government enterprises.

The industry is characterised by high competitive intensity across product categories. Key competitors include JCB India in the backhoe loader segment, and Chinese manufacturers such as SANY and XCMG in the high tonnage crane segment.

Clientele:

The positives

#1 Government capex on infrastructure to drive demand

The Indian government is driving economic growth through significant capital expenditure. The key focus areas of this capex are:

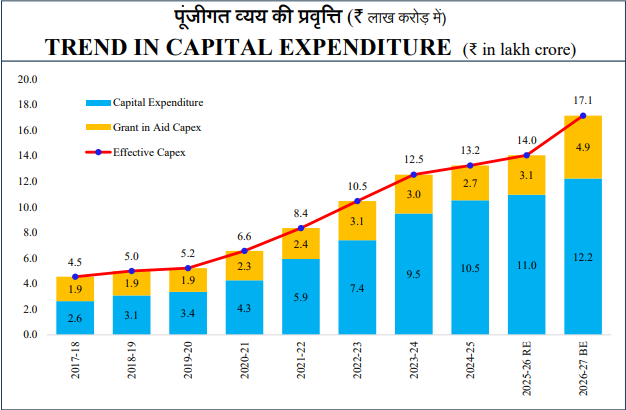

Govt capex: The Union Government has allocated ₹3.1 lakh crore toward road transport and highways (8% increase over FY26) and ₹2.8 lakh crore toward railways (10% increase over FY26) in FY27 (Source: indiabudget.gov.in).

Source: Indiabudget.gov.in

Urbanisation: Metro rail networks expanding across cities – connecting CBDs with airports, railway stations, and suburbs is driving demand for ACE’s products such as its flagship pick-and-carry cranes, which are widely used across construction sites. The table below shows some of the metro rail projects under works.

Housing: India’s urban population is expected to expand significantly over the coming decades, with an estimated 470 million additional people expected to move into cities. The following ACE products are positioned to serve this structural demand:

- Pick n carry cranes – Manoeuvrable in tight spaces and have moderate lifting capability

- Backhoe loaders are used heavily in the early stages of construction for activities such as digging, earthmoving, and heavy lifting. ACE has developed a cost-effective and robust product that can compete with JCB in less intensive applications, while also serving as a secondary or tertiary machine alongside equipment from foreign OEMs.

Industrial activity: Global and domestic companies are expanding manufacturing operations in India under initiatives such as Make in India, China+1 supply chain diversification, and the Production Linked Incentive (PLI) scheme. The Ministry of Defence has also cleared ACE as a supplier and placed an order for forklifts, indicating growing acceptance of the company’s product portfolio. This growth is driving demand for multi-purpose material handling equipment—such as forklifts, scissor lifts, aerial work platforms, pickers, stackers, and pallet trucks—which are widely used across factories, warehouses, data centres, and manufacturing units.

#2 Robust portfolio covering major mass construction applications

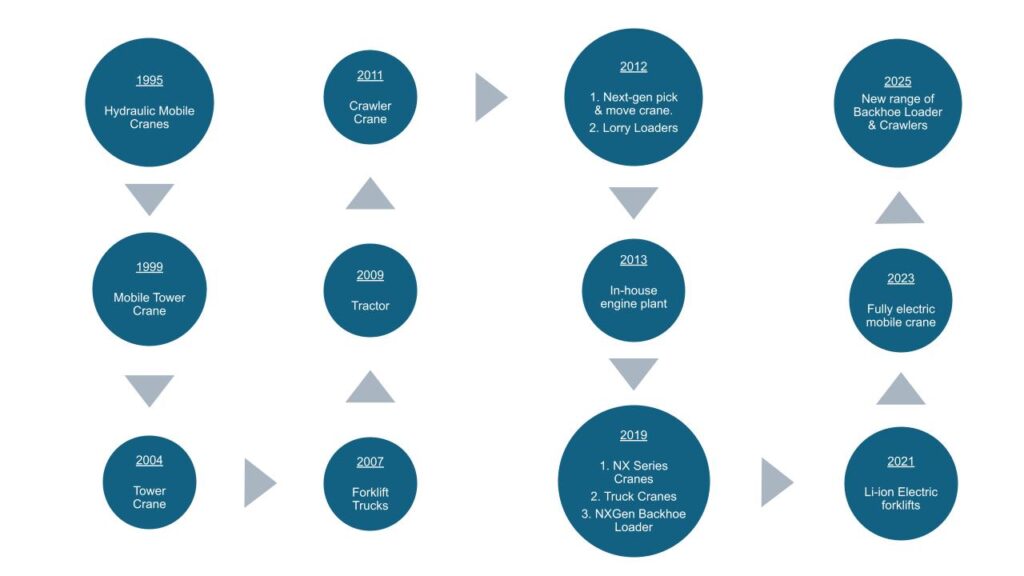

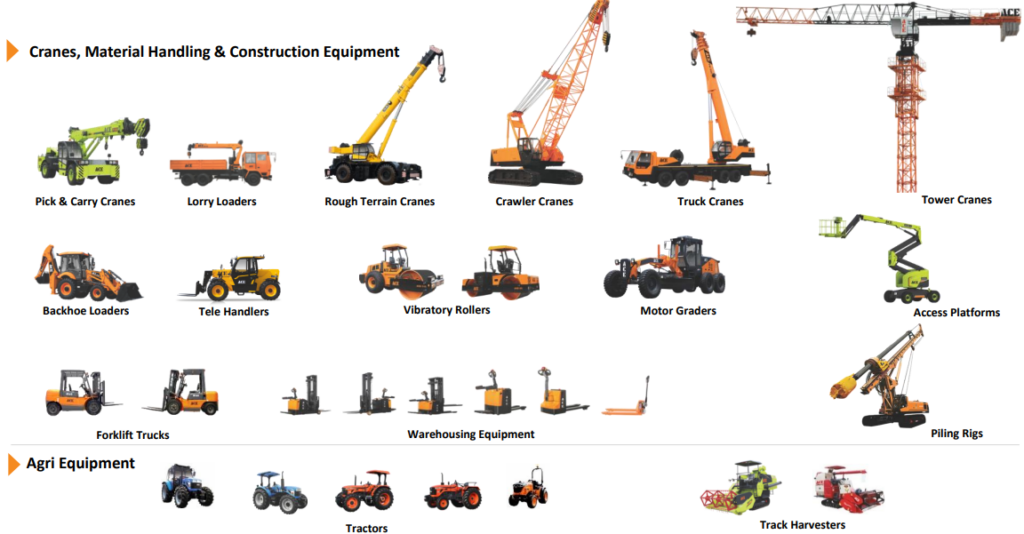

ACE has built a 30-year track record of product development and innovation. Below is a timeline of their product development as well as their key product portfolio:

Source: ACE Earnings presentation Q3-FY26

There are two reasons to be bullish on its product portfolio:

- ACE has established strong market positions in core categories. The company holds an estimated 63% market share in pick-and-carry cranes and approximately 60% share in tower cranes, demonstrating its ability to develop competitive products with wide construction applications. ACE’s market leadership is supported by a combination of factors. The company benefits from a first-mover advantage and has strengthened its position through an extensive network of sales, service partners, and dealers. Additionally, foreign competitors have largely focused on the high-tonnage segment, allowing ACE to consolidate its presence in other parts of the market.

- The company appears to be gradually moving up the value chain. Over time, ACE has introduced higher-tonnage equipment while incorporating advanced technologies such as AI-enabled safety systems, clutch-less transmission systems, and dual-use cranes. These developments suggest an effort to expand beyond entry-level equipment towards more technologically advanced offerings.

However, in some areas, ACE lags behind global competitors. For example, in the crawler crane segment, ACE currently operates below its peers in terms of maximum lifting capacity and lifting height. Similarly, in the truck crane segment, the company’s highest-capacity model is 55 tonnes, while competitors such as SANY offer models exceeding 100 tonnes.

ACE appears to be addressing this capability gap as well.

ACE has entered into a joint venture with Kato Works, a century-old Japanese construction equipment manufacturer known for its cranes and high-end engineering capabilities. Under this arrangement, ACE is expected to provide manufacturing facilities while Kato Works contributes technological expertise, including technology transfer and intellectual property.

The joint venture will focus on manufacturing higher-tonnage, technologically advanced cranes, allowing the company to participate in segments historically dominated by international manufacturers such as SANY, Kobelco, Escorts Kubota, and Zoomlion.

In another example, in the backhoe loader segment, JCB India stands out with a superior product, particularly in digging depth, breakout force, and the ability to deliver higher torque at lower RPMs. ACE has responded by launching the Phantom series, positioned as its premium backhoe loader offering.

#3 Healthy track record of financial performance

Over the last five years, the company has delivered a CAGR of 24% in sales, while profit has grown at a CAGR of 51%. The company reported healthy ROE at 28.7% and ROCE at 40.3% in FY25.

The primary driver of ROE expansion has been improving profitability (which has doubled). Asset turnover has remained consistent with their historical average, and the company operates with minimal financial leverage.

The improvement in profitability can be attributed to a combination of factors, including enhanced cost efficiencies, a favourable shift in product mix, and price increases—driven partly by the new emission norms and partly by inflation.

Capex plans and balance sheet health:

To support future growth, ACE has frontloaded the acquisition of freehold land (book value of approximately 250 Cr). Management has earmarked this land bank for the expansion of existing facilities or the development of new greenfield plants.

Additional capex of Rs 250 – 300 Cr is also being planned over FY 27 & FY 28 to be spent on facility upgradation, integrating robotics and expanding capacity.

The balance sheet remains relatively strong, as reflected in an interest coverage ratio of approximately 20x. It has negotiated better terms with customers, as evidenced by receivable days declining from 46 days in FY20 to 24 days in FY25. The company can comfortably take on fresh debt, whether for new facilities, research & development, or to develop the new JV with Kato Works.

Risk Factors

While ACE is positioned well as infrastructure capex picks up, a few key risks need close watching.

High competitive intensity: A recent example highlights the competitive environment in which ACE operates. When ACE was declared the L1 bidder by the Ministry of Defence for the order of 1,121 rough terrain forklifts. JCB India, the L2 bidder, agreed to match the quoted price. As a result, approximately 40% of the orders went to JCB India. ACE faces intense competition from well-capitalised and established players. To counter this competitive intensity, the company is prioritising cost efficiencies and innovation, such as creating electric forklifts. Therefore, how ACE manages the competitive intensity and whether it can grow its market share remains to be established.

Emissions Non-Compliance: The company received its largest-ever order from the Ministry of Defence (MoD) for 1,121 rough-terrain forklifts. However, during the transition between the testing/ordering phase and the execution phase, new emission norms came into effect, requiring the products to comply with the CEV-5 standards. As a result, a No Objection Certificate (NOC) is required for the company to deliver non-CEV-5-compliant forklifts under the original specifications. If the MoD does not grant the NOC, it could materially impact the execution of the order, the company’s order book, and its stated objective of generating 5–10% of revenue from the defence segment.

R&D Challenge: The company’s expenditure on R&D is low compared to its peers. It remains to be seen how the company intends to bridge the technological gap.

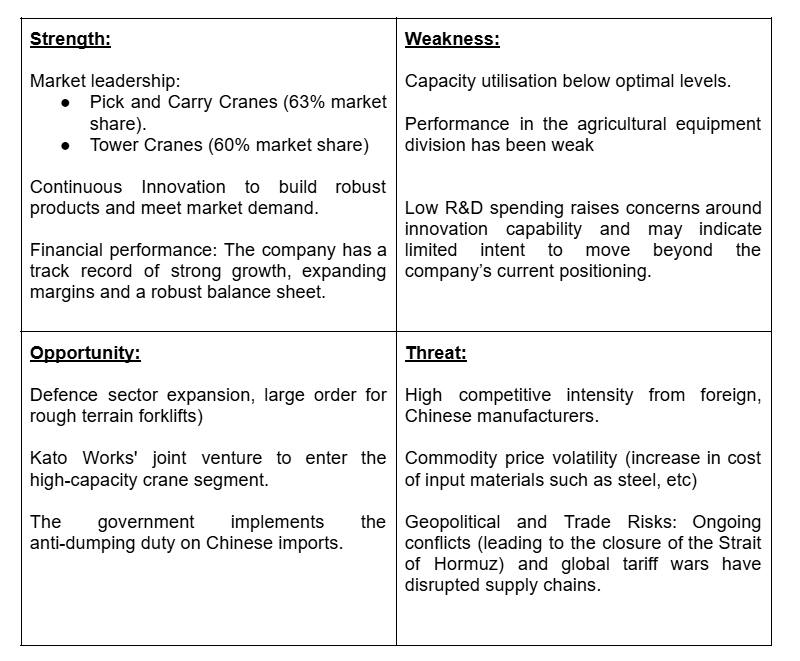

Where ACE stands today in terms of business positioning can be summarized as below.

SWOT Analysis:

Stock Price Performance and Valuation

ACE’s stock price has corrected a sharp 41% from its peak in April 2024, with the P/E multiple compressing from 67x to approximately 26x. This places the stock below its 10-year median P/E of 31x.

A potential re-rating could be supported by ACE’s shift towards a superior product mix (higher-tonnage, technologically advanced cranes), increasing exposure to more structural demand segments such as forklifts and warehousing equipment. Notably, operating margins, which were historically below 10%, have expanded to approximately 15%. Its new joint venture with Kato Works can further work in its favour.

However, all this hinges on ACE’s execution from here on — its ability to move firmly beyond entry-level equipment, the success of its JV with Kato Works, eking out presence in higher-end crane segments where foreign manufacturers currently dominate, and managing competitive intensity without sacrificing margins.

ACE’s dominant position in pick-and-carry and tower cranes, improving financial metrics, and a credible roadmap toward higher-value segments make it a stock worth having on the watchlist. The question is whether ACE can capture a larger share of the higher-margin, higher-technology end of that opportunity. For that, a watch on execution and product profile, and sustained margins hold the key.

Disclosures and Disclaimers

The following Disclosures are being made in compliance with the SEBI Research Analyst Regulations 2014 (hereinafter referred to as the Regulations).

1. PrimeInvestor Financial Research Pvt Ltd is a SEBI-Registered Research Analyst having SEBI registration number INH200008653. PrimeInvestor Financial Research Pvt Ltd, the research entity, is engaged in providing research services and information on personal financial products. This Research Report (called Report) is prepared and distributed by PrimeInvestor Financial Research Pvt Ltd with brand name PrimeInvestor.

2. PrimeInvestor Financial Research Pvt Ltd, its partners, employees, directors or agents, do not have any material adverse disciplinary history as on the date of publication of this report.

3. I, Sathya Pillai Shanmugam, author/s and the name/s in this report, hereby certify that all of the views expressed in this research report accurately reflect my/our views about the subject issuer(s) or securities. I/We also certify that no part of my/our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report. I/we or my/our relative or PrimeInvestor Financial Research Pvt Ltd do not have any financial interest in the subject company.

I/we or my/our relative or PrimeInvestor Financial Research Pvt Ltd do not have beneficial ownership of 1% or more in the subject company at the end of the month immediately preceding the date of publication of the Research Report. I/we or my/our relative or PrimeInvestor Financial Research Pvt Ltd do not have any material conflict of interest. I/we have not served as director / officer, etc. in the subject company in the last 12-month period.

4. I Sathya Pillai Shanmugam do not hold this stock as part of my investment portfolio. I/analysts in the Company have not traded in the subject stock thirty days preceding this research report and will not trade within five days of publication of the research report as required by regulations.

5. PrimeInvestor Financial Research Pvt Ltd has not received any compensation from the subject company in the past twelve months. PrimeInvestor Financial Research Pvt Ltd has not been engaged in market making activity for the subject company.

6. In the last 12-month period ending on the last day of the month immediately preceding the date of publication of this research report, PrimeInvestor Financial Research Pvt Ltd has not received compensation or other benefits from the subject company of this research report or any other third-party in connection with this report.