Seniors often give a standard piece of financial advice to folks born in the 80s or after – ‘Max out your Voluntary EPF contributions.’ That’s because their own retirement planning began and ended with the EPF (Employees Provident Fund).

But with tax laws changing and much better investment options emerging, there is no longer any need for investors to rely on EPF for their retirement needs. We recommend keeping your EPF contributions to the minimum permitted by your employer, or even skipping it, if possible, for five good reasons.

#1 It’s employer-dependent

A big flaw in the EPF is that it forces you to put your retirement savings at the mercy of your employer. Your enrolment, KYC process, deposit of contributions, transfer of your EPF account when you switch jobs and processing of your maturity proceeds – all of these are routed through your employer and are dependent on the co-operation and competence of HR in the organisation you work with.

Employees across India who have worked with dubious companies ranging from Kingfisher to Byjus have lost out on both their pay cheques and their provident fund contributions when their companies ran into governance or debt troubles and decided to default on PF dues. EPFO’s FY23 annual report (its latest) records ₹13,953 crore in dues from defaulting organisations.

Crooked employers apart, recording errors by HR can also leave your money stuck with the EPF. The EPF is a peculiar investment organisation which has four times more dormant accounts than active ones. The EPF had 29.88 crore subscriber accounts as of March 31, 2023, but only 6.85 crore belonged to active contributing members.

The EPF’s large collection of inactive accounts is mainly due to employees switching jobs and being unable to access their past balances. Organisations create new UANs (Universal Accounts Numbers) when employees join them, fail to transfer PF balances of leaving employees or forget to officially close accounts. All of this results in employees’ EPF accounts becoming inaccessible later.

While the EPF may have worked smoothly in an earlier era where employees were sworn to a single organisation for life, it has proved a bad fit for employees of this generation who are mobile and frequently switch jobs for better prospects.

#2 Tax breaks are going away

Fans of the EPF hard-sell the scheme based on its ‘unique’ EEE (exempt-exempt-exempt) status which once made contributions, returns and maturity proceeds completely tax-free. But the EPF’s EEE status is now history due to recent changes in tax laws:

- From April 1 2020, employer contributions to the employees’ EPF account exceeding Rs 7.5 lakh a year were made taxable in the employees’ hands as a perquisite.

- From April 1 2021, tax laws were amended to say that if the employee’s own contributions to the EPF exceeded Rs 2.5 lakh in a year, the interest on the excess contribution would no longer be tax-free. This partly revoked tax breaks on contributions and returns.

In addition to all this, your EPF contributions are not eligible for section 80C benefits under the new tax regime. Today, opting for the new tax regime is a good decision for most taxpayers, with a standard deduction of Rs 75,000, wider slabs and low surcharge. Sticking with the EPF for the sake of wanting its tax breaks can prevent you from making this beneficial switch.

#3 The 8% return is unsustainable

One of the oft-repeated arguments for EPF is that no other vehicle can give you a guaranteed return of 8.25% (tax-free). It is true that the EPF has ‘declared’ returns of 8.1% to 9.5% in the last 15 years.

But fixed returns at these levels are not sustainable in the long run. EPF’s portfolio choices are guided by the investment pattern mandated by the government. Currently, guidelines require EPF to invest 45%-65% in central and state government securities, 20%-45% in other top-rated bonds, up to 5% in short term debt and 5%-15% in equities via Exchange Traded Funds.

The EPF is thus mainly a debt vehicle which sticks to sovereign and AAA rated debt for over 85% of its portfolio. While it has been investing incremental sums in ETFs (Sensex, Nifty, CPSE ETF, Bharat 22 ETF) since 2015, these account for just Rs 2.34 lakh crore, under 10% of its Rs 24.75 lakh crore portfolio. This cannot move the needle much on returns.

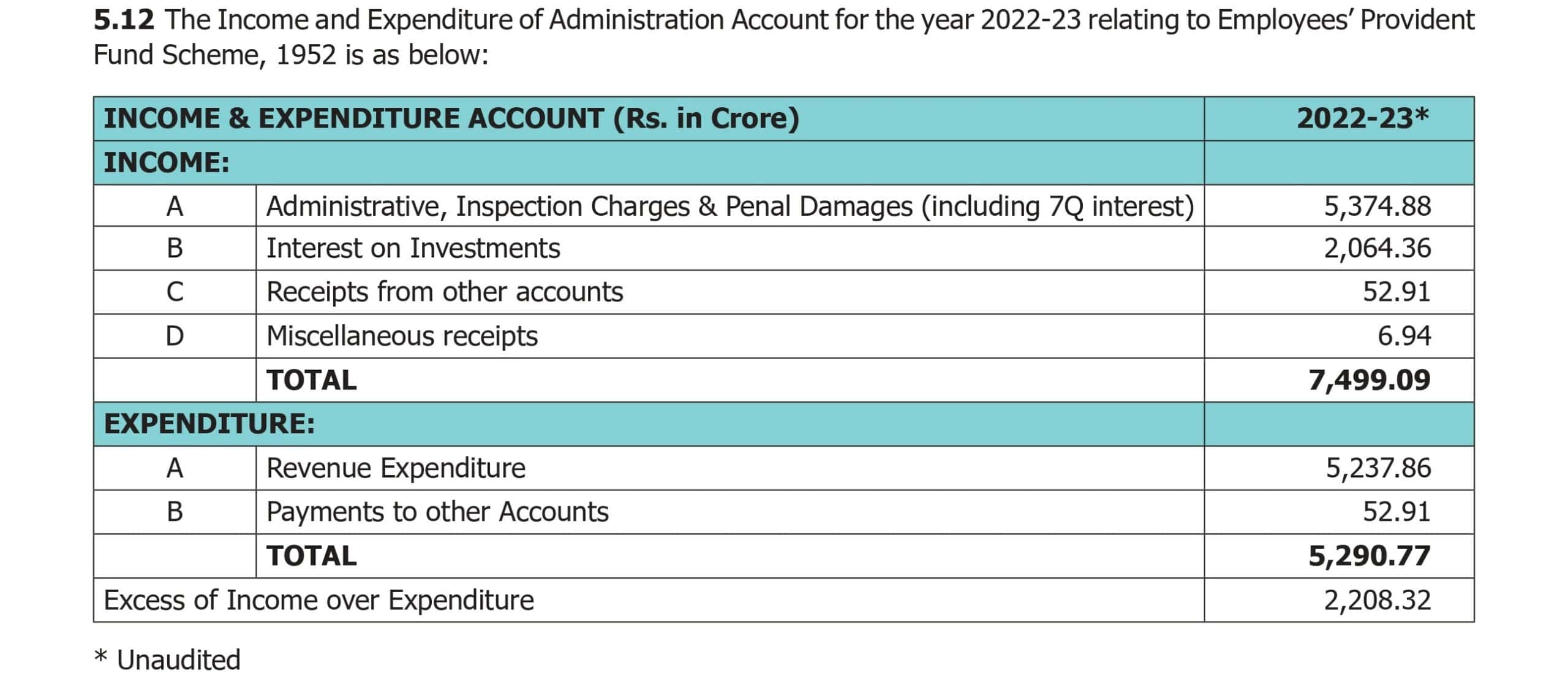

EPF returns depend mainly on yields on government securities and bonds from AAA companies, which are currently in the 7-7.5% range. Yet, the EPF has been declaring and distributing returns of 8% plus year after year. In 2022-23 for instance, while it declared returns of 8.15% to subscribers, its portfolio earned a weighted average yield of 7.78%. (Source EPF Annual Report 2022-23).

This is possibly because of administrative charges levied by the fund from employers and the large number of inoperative accounts, where retiring employees have failed to claim their balances within 36 months.

In the long run, the EPF cannot afford payouts that are much higher than yields on g-secs and AAA bonds which make up the bulk of its portfolio. Yields on g-secs and AAA bonds have trended down from over 8.5% to 7% in the last decade or so and are likely to head further south as India transitions into a more developed economy.

#4 It has archaic accounting

When you invest money in mutual funds or the NPS, your contributions go to buy units at the prevailing Net Asset Value (NAV) declared by the fund. Your returns are also calculated based on the mark-to-market value of the portfolio which is reflected in the NAV. This lends transparency to how and where you are earning your returns from such vehicles.

However, EPF operations are a black box. It pools contributions from subscribers, invests this in a common portfolio and pays claims out of this pool to subscribers who are retiring or exiting from the fund.

To decide its annual “returns”, the EPF prepares a simple income and expenditure account every year where excess of its income from administrative charges & interest over its expenses are treated as a ‘surplus’ and paid out. It is also not clear how often the EPF does a mark-to-market valuation of its portfolio, as its investments are captured at face value in its annual report. Substantial delays in publication of its annual accounts and reports (2022-23 is the latest one in the public domain) also make it hard to fathom the state of its finances.

The EPF also does not follow unit accounting. Unit accounting makes it possible for investors in mutual funds, NPS and other market vehicles to time their entry and exit into the vehicle to favourable bond or stock market conditions and ensures that portfolio returns are fairly distributed to investors.

In fact, the lack of unit accounting seems to be the reason why the EPF has found it so tough to credit interest dues to individual subscribers on time, since the change in taxation policies in 2021. While the fund claims that subscribers will be given due credit for their accumulated interest for compounding purposes, the interest credit often does not reflect in member passbooks for several months after the end of each financial year.

#5 It rejects a lot of claims

There’s nothing new about the EPF’s accounting methods or investment patterns. But a disturbing feature of the fund lately has been a rising rate of claim rejections. Though the EPF’s user interface has become friendlier in recent years, with subscribers able to access their balances and passbook through the Umang App, the back-end seems to be mired in problems.

The X handle of the EPFO (@socialepfo) is rife with complaints from subscribers whose maturity claims or advances from EPF have been delayed or denied. This particular issue has also been getting media coverage of late.

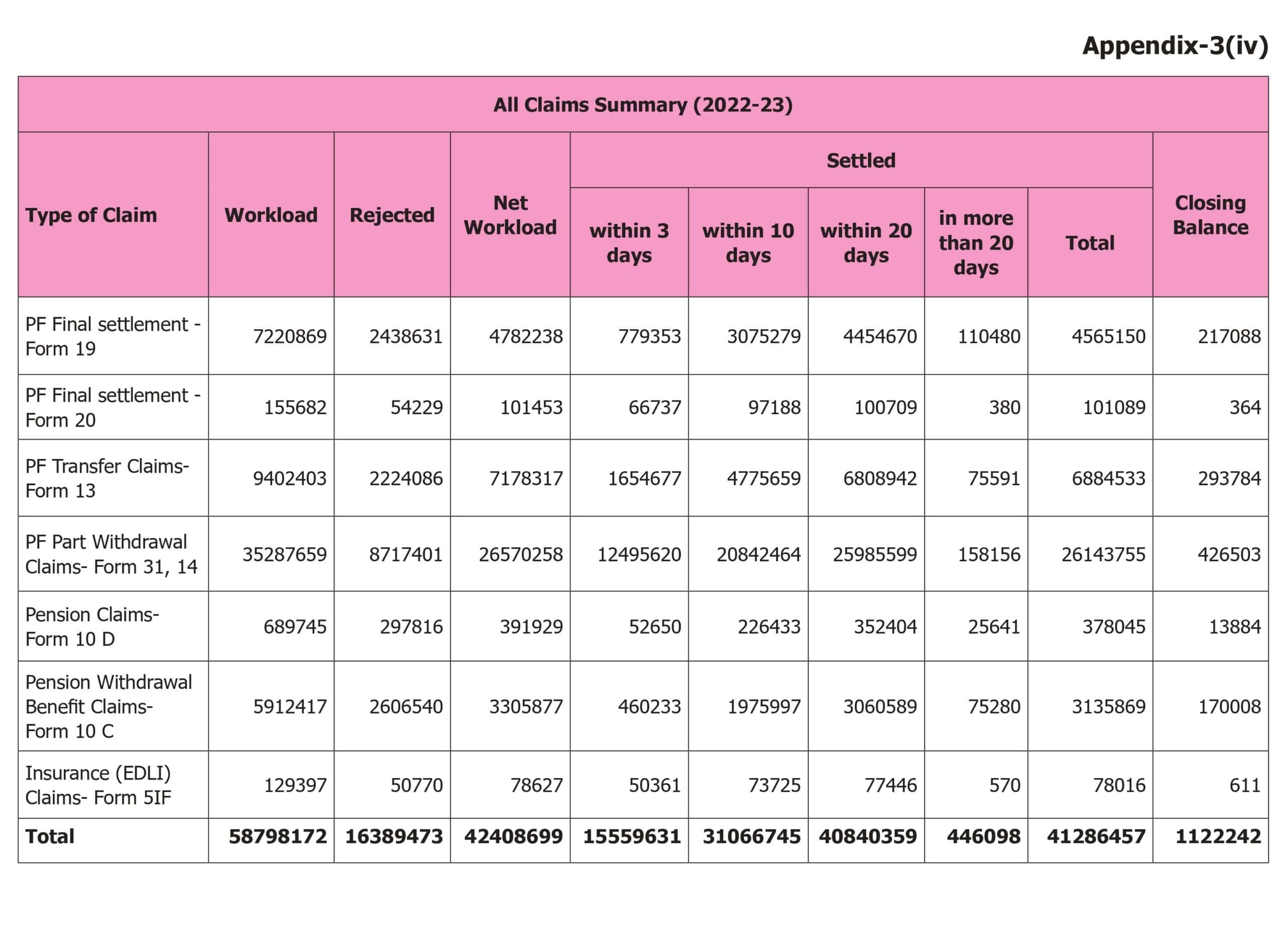

Subscribers trying to withdraw their balances say they are stymied by minor name mismatches between their EPF records and their Aadhar, multiple UANs created in their name, lack of proper Aadhar seeding or UAN allotment and so on. They also complain of being made to run from pillar to post due to jurisdiction issues, inordinate delays in responses from EPF offices and more. These experiences are not one-off, as the EPF annual report for FY23 reveals that it rejected 33% of the final settlement claims filed in that year.

Given that an employee makes lifelong contributions to the EPF and cannot easily withdraw prematurely, claims rejections in this vehicle need to be taken much more seriously than is the case with other investments.

Bottomline

All this makes a good case for opting out of the EPF if your employer allows it. The EPF is supposed to be optional for employees earning over Rs 15,000 a month in basic pay. If your employer organization insists on enrolling you, you can still keep your contributions to the minimum of Rs 1,800 a month (based on 12% of Rs 15,000).

Given that retirement is a long-term goal for most folks and a tough one at that, investments towards it are best made in equity-oriented vehicles rather than debt-oriented ones like the EPF. While you minimize your EPF contributions, it’s important to start building a corpus with mutual funds or other equity vehicles, to ensure your retirement goal is met.

43 thoughts on “5 reasons to give EPF a miss”

Very insightful article. Thank you Aarati.

Can we sell our EPF easily if we want to, now? What are the strings attached?

You can withdraw all your money if you have quit one orgn and not rejoined another for over two months. Or you can take an advance of a limited amount based on conditions. Try these and minimise future contributions

I think both EPFO and PPF fall in the same category. Funds that even invest up to 35% in Equity (the likes of Parag DAA) can easily beat the returns. Also when you get the lumpsum at the end of PPF or EPFO you still need to invest it somewhere. So why not do that from now onwards.

Exactly

My money is stuck in EPF. I can’t get it out even though I am eligible. A previous employer bungled something up and I they are taking months to do anything about it. I tried checking with them what is wrong and I couldn’t find a thing.

I wish there was a clear mandate to – employers: either deposit EPF or pay the same amount in a/c. I’d rather foot the tax on that anyway small amount than deal with EPF.

I have indeed read this article and it is so well done. However something like EPF doesn’t deserve an iota of this respect – point 5 alone (+ the quagmire of a hell EPF and its babudom is).

What else? I have heard ZERO stories of anyone getting things cleared at EPF after retirement even quarter easily. ZERO. And I know a lot of stories.

And this kind of expectation scares me away from NPS as well. I know NPS might be a slightly different beast, but mere connotation of “sort of Govt backed” gives me creeps.

Really sorry to hear this. Perhaps you can reduce your contributions under your present employer. Try complaining on the Twitter handle @socialepfo tagging the FM and see if you get a response. Also try and get an advance of your current balances. Understand your misgivings about NPS. Hard to reassure you on the withdrawal process but at least the accounting is modern.

Try to get an advance from epf so at least part of your money is safe.

Thanks Aarti. Didn’t know about this Twitter handle. Will try this. Appreciate it.

The a/c is kinda “stuck”. I do not know how to explain it. I am not able to do anything other than logging in and accessing passbook. Last employer did some pension part ZERO for few months (they say it was EPFO’s fault but EPFO says it was employer i.e. employer’d 3rd party payroll processor’s fault).

I will try to use that twitter handle you shared.

Yes please!

There is no way FM is going to give a reply. She puts up a straight face even in press conferences and treats all press folks as second class citizens. I have Zero expectations from one of the most incompetent and arrogant minister in this circus called Govt.

It is not the FM who sits and replies to tweets personally :-). Just that tagging the office gets a response from EPFO. Have seen it happen so worth a try.

Very thought-provoking article, indeed.

At 57, I am closer to retirement. I have worked for 3 companies and all accounts are linked to a single UAN. I am am able to see passbook/statements all the accounts at EPFO site. I have never withdrawn from EPF so far. I am still employed and I am continuing to contribute to EPF. I have enjoyed the (exempt-exempt-exempt) tax benefits throughout my career, until 2021 when the tax exemptions began to go away.

Given the administrative hassles in withdrawing from EPF, what is the ideal thing to do in my situation?

Should I just withdraw the whole amount and invest it elsewhere?

Hopefully as your UAN is linked should be all right. Check with your employer if you can file a claim for withdrawal as you have completed 55 years of age. If you can withdraw please do it and invest in MFs as recommended by primeinvestor

Wonderfully summarised. sometimes, the HR is reluctant to make EPF optional. Further, am not sure how many of them would allow to contribute to PF on a minimum of 1,800 (12% of 15,000) when the person is earning a higher basic salary. So for most of us, there is no easy way out.

I hope the government amends the labour law which provides an option to the employees to choose between NPS and PF.

You are quite right. Some newer organisations do allow you to minimise or opt out.

When & how tax on interest beyond 2.5L are deducted? Is it TDS ?

It is not TDS as there is no money credited to account unless claim is made. It is available in your passbook along with taxable and non taxable part of interest. You have to account for it while filing your ITR’s.

the catch here is that by the time you file ITR, the interest for FY is not yet known. So we are declaring taxable interest income of previous FY which is technically not correct. What i have heard is that assessee is supposed to “Manually” calculate taxable interest, and do ITR filing based on that – which is too much to ask.

Talk of Digital India – here we are!! Sad but true.

Very informative article about EPF.

Thanks,

Vijay

Thank you

All this makes a good case for opting out of the EPF if your employer allows it.

-> An employee with a basic salary of over Rs. 15,000 and who has never been a member of EPF can opt out of the scheme. But once they become a member, they cannot opt out of the scheme.

So, one cant opt out if he/she is member of EPF already, which will be case for most of us. Not sure if we can request employer to reduce it.

True, but you can avoid making higher VPF contributions at least. If you switch jobs, can avoid becoming a member in new organisation.

Great Article Aarati,

I specifically wanted to ask 2 things

1. “The EPF is supposed to be optional for employees earning over Rs 15,000 a month in basic pay. If your employer organization insists on enrolling you, you can still keep your contributions to the minimum of Rs 1,800 a month (based on 12% of Rs 15,000). ”

All the employers are making 12% contributions of the basic pay, I hope you meant that it has to be limited to 12% of basic pay only, and not that we can reduce the contribution to 1800 even if the basic pay is for example 1 lakh rupees?

2. Can you share a list of best practices to ensure we dont face claim rejections ? I know you cannot give a full proof list, but if there are things you have read etc. Like Aadhar linking, Name matching etc.

Thanks

Devang

Only some employers contribute 12% of basic pay. EPF rules actually mandate only 12% of basic pay upto Rs 15000. This is why the recommendation to keep it to Rs 1800 if possible. Hard to give a list as EPF itself doesn’t seem to have one unfortunately. Non standard practices across its offices. But ensuring a single UAN and correcting your Aadhar so there is no mismatch between EPF ac and Aadhar on exact name, surname, spelling, address may help.

Also add Father’s name. I got transfer rejected several time with reason that Father’s name mismatch. After multiple attempts they approved.

Thanks for sharing that.

Hi Aarati,

1. I have a large corpus in EPF. Retiring in two years.

2. Could you guide on withdrawal and investing in MFs.

Thanks and Regards

Rajiv K Mendiratta

Kindly check with your employer if you can withdraw your balance now as you have completed 55 years. You can invest in the FDs plus mutual fund options recommended in Primeinvestor. Do make sure you have an allocation to both debt and equity.

Comments are closed.