PrimeInvestor Research Team

March 24, 2024

3 Comments

What does your typical day look like? You wake up, have a cup of coffee or tea. There’s breakfast to have, lunch to prepare, laundry to do, spend the day at work, with a well-earned sleep at the end.

But that’s just the routine! There’s so much more you do in the day – stepping out to a nice lunch with colleagues, browsing through Amazon or Flipkart and filling up that shopping basket or then going out to the mall and doing the same. Swiggy or Zomato come in handy when you’re too tired to get dinner ready. Your commute is made bearable listening to music or podcasts on your phone or the perfect car sound system. Weekends are spent at the movies, at dinner maybe, or lazing at home with your big-screen TV. Or perhaps driving down in your comfortable SUV to a short weekend getaway once in a while!

This is your story. This is the NEW consumption story. Aside from the routine goods we all consume to live and survive, life has now become more about aspirations and experiences. Call it the YOLO effect or upgrading your lifestyle, you are now revving up the New Consumption story in India.

Our newest smallcase portfolio – Prime Trends – Consumption is built precisely on this consumption theme.

Broadly, the following four factors form the basis for our investment thesis:

Discretionary spending pick-up: The general thesis is that the average income levels of the population has crossed the threshold that takes care of the basics and incremental income will now go towards discretionary consumption.

State-wise trends indicate an acceleration in spends across the spectrum: Some of the more developed states, which have crossed well beyond the national per-capita average, have become the bedrock of modern retail and discretionary consumption. Meanwhile, currently poorer states can see consumption picking up as they progress in development thanks to improved infrastructure, shift towards manufacturing and higher labour force participation.

Growing middle-class to spur aspirational spending: A World Economic Forum study says that the number of middle-income households is likely to increase from 21% of population in 2018 to just over 40% of the population by 2030. Easier access to credit and social media, along with e-commerce, have also become enablers of consumption. All point to a healthy growth rate, far higher than nominal growth rate, for companies that can successfully address the growing consumption needs.

Scope in individual regions: The large size of our economy and the economic output of each geography offers scalable opportunities for businesses. It isn’t necessary for a country-wide presence for companies to scale up; the sheer size of each region offers ample scope even for regional players.

Current market conditions are also lining up for a well-timed entry. There is, of course, the broader market correction that we’re seeing. Even without this, the shine has been rubbed off the consumption story in recent times. The Covid and post-Covid periods have caused fluctuations in the demand (and input costs) environment and this is reflecting in quarterly earnings numbers, and consequently in stock prices. Several higher-priced consumer plays are now available at attractive valuations, providing a good window of investment opportunity. The long-term consumption story, therefore, looks even better now!

So, if your spending is going to charge the economy and the consumption theme, there is a way to also benefit from it!

The 30% Crypto tax is the Indian government at its passive aggressive best (or worst, depending on your view point).

The text of this tax law coupled with what the finance minister said in the post-budget interview leads me to think that the government holds the crypto ecosystem in absolute disdain.

The crypto exchange promoters are welcoming this move as a recognition bestowed upon them. Obviously, they are choosing to see the slim silver lining.

Truth is this is just one jaw of the vice that is going to be applied on the crypto industry.

The other jaw will likely be when the crypto bill is introduced regulating these exchanges with stipulations such as these:

1. Requirements for KYC registration (not just collecting PAN but registering with KRAs) 2. Limits on the range of crypto assets that can be offered for trade (likely by coin market cap initially and with regulatory approval then on) 3. Possibly, placing qualification limits on investors allowed to invest in crypto (bringing to bear the ‘accredited investors’ concept that SEBI is working on) 4. Severe curbs on how they can be marketed (no celebrities, for example)

In essence, the government would do everything short of banning to ensure that the growth of this industry is significantly tempered.

Why would the government do this? Simple:

1. India is not a big crypto mining country – we don’t have the power capacity to spare. 2. That means most of the crypto assets are ‘imported’. 3. Which means flight of capital and a potential current account problem for the central bank and the government

India already is struggling with gold – another non-productive, imported asset that causes balance of payment issues. Why would they encourage creation of another?

A recent ET Wealth study done jointly with us, had many of our distributor and advisor friends lashoutat us on social media. The same happened some months ago when we took a firm call on Franklin funds. We thought we should not react but since this appears to be repeating, we decided to ‘respond’.

We have several ‘buy’ calls on funds. No distributor/advisor criticizes us for wrong judgement there. Whenever we give ‘sell’ calls, we are hit out in the social media (without naming us of course – they are gentlemen) as being ‘immature’ ‘rash’ and that we ‘need schooling’, ‘we do this for a hobby’ or ‘performance alone does not matter’ etc. These comments are never from investors (they give us more constructive feedback, thankfully). They come from doyens in the advisory industry whom we respect and from whom we learn, along with several respectable distributors. And many are but good friends in Chennai! It’s a small city here folks.

To these doyens and distributor friends, we wish to say – we are open to learning. We welcome criticism. But we prefer them to be issue-based and factual. A general dig about our ‘testing labs’ doesn’t help us improve, you know!

So, here’s the thing:

When we gave a ‘sell’ call on Franklin fund house, it was only partly based on the performance – our detailed note had it (not our problem that the media took excerpts). It was a judgement call on how a fund house that put investors through painful times can be depended upon again. It is our view and we stated it clearly. Why does it upset distributors? Please feel free to counter it with a rebuttal based on facts and logic.

When we wrote on HDFC Top 100 or ABSL Frontline Equity a year ago on why we prefer index funds to these large caps it was based on sound evidence of exceedingly inconsistent performance. It remains the same.

For those who question us on our testing labs, we wish to make two points: One, our process and our thought process: We like to follow a process rather than just tell our customers ‘X fund manager is a good guy. We trust him. He has conviction in his calls’. That is not our way.

We respect all fund managers and their difficult task. But to us, performance matters and consistency in performance matters the most, however small or big an AMC or fund manager. Our numbers time and again show that consistency pays off in the long run. Our ‘testing labs’ have enough ‘metrics’ to show us ‘steady relative underperformance or outperformance’.

Yes, we do go beyond numbers to the ‘prudent portfolio construction’ that someone asked us to measure. Every fund’s portfolio has a story to tell and means to be prudent. One can decide not to tolerate the portfolio underperformance, or one can give a narrative of conviction and decide to wait. Where it is not clear, we do hear what the fund manager has to say. We recently did that for a midcap fund too!

But in this qualitative second step, it boils down to what convinces us or the investor. And that becomes a subjective call. That is where we take comfort in process. We take comfort in a fund manager sticking to his/her process but willing to make changes when the performance chain breaks. We think that is an important quality in fund management. Course correction shows willingness to change and improve.

Instead, to ask an investor to wait it out because a fund cannot perform or will perform in spurts and go silent later is not quite convincing, is it? And for 3 years, 5 years? Does an investor need a fund manager and an advisor on top of it, to say this? He might as well throw a dart!

Two, investor behaviour: There is little reason for an investor to tolerate prolonged underperformance simply because the odd year will give him the bounce back. Which year will that be? In Tamil, there is an adage: ‘thai pirandhaal vazhi pirakkum (come the harvesting Tamil month of thai in January, there will be a new path). A poor fellow asked ‘endha thai?’ (which January will it be?) The odds don’t favour an investor in the face of prolonged volatility and stark underperformance.

Our own study of several thousand customers in an earlier firm, tells us that investors who are long-term will not put up with poor performance beyond a year or two.

Secondly, there is a HUGE difference between a young investor with a portfolio of a few lakhs and another with several crores. The latter is affected very little by underperformance in a couple of funds while the former does take an impact when his few thousands of SIP underperform.

Besides, he/she now has a poor experience. He will not return.

And pray, when they have better alternatives in MFs, what favour are we doing by asking him to stick to an underperformer? Is it tax? It is the investor who should be concerned, not the advisor/distributor. Please don’t take an investor to be a fool! Is it commission? In that case an investor should be even more concerned!

For 20 years or so ‘the buy and hold’ mantra has stood investors (and distributors) in good stead (and still does). But that is meant to ride out the market volatility and the market underperformance – NOT FUND UNDERPERFORMANCE when a whole bunch of other funds manage their act!

If investors did that 15 years ago, it was because they could not keep track of performance. It was too cumbersome to even switch funds! Any reason they should act the same now, when they can see their fund’s performance with a click and there are better and clearer alternatives? Even if that means simply an index fund?

Besides, the 20-year argument is not going to help an investor who has, say, 7-12 years to accumulate enough returns for their children’s education, does it? Is 10 years too short a period to expect a fund to deliver?

And who are we – as advisors, researchers, or distributors to ask investors to put up with underperformance for no reason? Who are we to insist that an investor MUST hold THE SAME FUND for 20 years to see results? Who are we to bask in the past glory of an AMC’s 25 years track record when a 25-year-old doesn’t give two hoots about it?

And how long are we going to say not holding ADAG stocks helped a fund in hindsight or not going near infra and real estate helped an AMC in 2008? Of course, it did help! Good for the investors. MOVE ON and show us what funds do NOW!!!

It’s about time the investor’s ‘guides’ took a relook at changing investor preference, changing product line-up and changing ways to invest, track and review. Why are index funds a taboo in many distributors’ books, even today?

And finally, our calls on funds are our views. We will stay accountable to investors who take them. Why does it bother so many of our distributor friends? After all, they have their own processes and outcome to share with their clients?

Also, please be assured – we have our own ‘research game’ and we don’t need any ‘schooling’. We have our own track record of writing and educating investors through various forums including media. And we definitely have a track record of creating wealth for thousands of grateful investors across the country through our research and recommendations.

Gentlemen, you’re all welcome for a coffee session in our office if you want to know if we have ‘metrics’. We will be happy to show you. The learning can be mutual! Avoid ‘virtual’ mudslinging and troll-like behaviour. Doesn’t do anybody any good.

Let’s move on. It’s not 2001, its 2021! The investor is king not the manufacturer!!

After a flurry of book reviews earlier this year, I have gone largely silent on this count. Not that I became suddenly too busy or stopped reading books. Rather, I decided to go ahead and clear out some backlog that I had in my personal reading list. Here are brief notes about each of them – I hope one or more of these catch your fancy.

None of these books are particularly ‘PrimeInvestor’ topic – relating to personal finance or FinTech. Nevertheless, I thought I’ll share my thoughts on these books – 4 of them – in a brief note. Some of these books are quite popular, and all of them are worth your time, if the topic interests you.

“A Short History of Nearly Everything” by Bill Bryson

Although this book was neither short (running to more than 500 dense pages) nor about history in the traditional sense of the word, it made for a fascinating read. It does cover ‘nearly everything’ though – starting from the big bang and finishing up a few years after the millennium. The book gives a history of science and scientific discoveries across the spectrum – from cosmology (where it starts) through palaeontology, geology, and the modern physical sciences. There is a lot of stuff about the lives and quirks of scientists which can be occasionally distracting from the flow of the science in the book, but nevertheless quite engaging.

People who went to school in the 80s (like myself) or even the 90s, will likely find out that a lot of stuff they learnt in school are outmoded now thanks to newer discoveries. The book is a good refresher on science for everyone. Non-science folks, especially, will find this book a good, friendly guide to the realms that they are likely not familiar with.

This book, written in mid-80s, presents a survey of western philosophy from a historical perspective. There are 6 main sections covering individual philosophers through the ages – Plato, Descartes, Hume, Hegel, Marx, and Sartre. Not to say that these are the only philosophers or schools of thought covered – there are quite detailed accounts of Aristotle (obviously), Kant, Nietzsche, Wittgenstein, and more. The sections on Hegel and Marx are especially strong and relevant to this day. And, of course, existentialism, in a completely different sense, captures the personal ennui of modern existence. So, the book provides a macro perspective that can be helpful to make sense of our contemporary quotidian existence.

The language is quite simple and the writing style fluid, which makes for fluent, if not easy, reading. You can expect to come out of the reading with a bird’s eye view of the western philosophical landscape, up until relatively recent times. Indian readers may be disappointed by the lack of any mention of oriental, leave alone Indian, philosophical thoughts and how they compare with the occident.

“Godel, Escher, Bach – An Eternal Golden Braid” – Douglas Hofstadter

This is a book that I started reading in college, but never got around to finishing until recently. It’s a most remarkable book – even saying that it’s a work of staggering intelligence would be underselling it.

Bach was a genius composer from the 18th century. MC Escher was a graphic artist from early 20th century. Kurt Godel was a logician and mathematician from the same period as Escher. What the works and findings of these three have in common is the subject matter of this book. Using concepts such as recursion, strange loops, self-reference, and self-replication, the author spins a web of connections between the seemingly disparate fields of art, music, science, and mathematics. The chapter on Zen koans provides for a delightful excursion into the world of meanings and meaninglessness. The exposition of Godel’s famous incompleteness theorem is the most lucid and patiently developed among the handful of explanations I’ve read on the topic. The extrapolation of the concepts of recursion and replication into the world of cellular genetics is eye-opening.

For those uninitiated into the music of Bach, this book will provide great motivation to get into it. And for those with a passing familiarity (like myself), it would likely take them into unexplored territories and provide great insights. For example, I discovered ‘Crab canon’ and this ingenious depiction and play of the piece on a mobius strip.

The later chapters on artificial intelligence provide a good grounding on the fundamental questions in the field, but can be underwhelming for those who have followed the developments in the area over the past four decades since this book was published (in the early 80s).

Overall, the book is not an easy read – although the author makes strenuous effort to keep it engaging with motivating dialogues that precede every chapter. The book runs into 750+ large format pages, and definitely not for casual reading. However, for those that commit and apply to get through it, there are rewards aplenty.

“Seven Brief Lessons on Physics” – By Carlo Rovelli

After reading the Hofstadter’s tome, I definitely needed something smaller and this book let me go all the way to the other end of the spectrum in that aspect. ‘Seven brief lessons’ is almost a tenth of the size of GEB, coming in at 80 pages. But it makes for a thoughtful read nevertheless.

This book, published in 2015, brings readers up to speed (or up to 2015) on various advancements in physics. Covering topics like general relativity, quantum theory, quantum gravity, gravitational field, particle physics, and thermodynamics, it presents a bird’s eye view of what the current state of knowledge is in these disciplines. The language and style are masterful and easy to follow.

Of course, short 10-15 page essays on these topics hardly do justice to these vast areas of study, and leaves the reader wanting to know more. And that might precisely be the aim of the book.

The last ‘lesson’ of the book is a wonderful and reflective – almost meditative – essay that provides perspective on how human beings are situated in the vast cosmos and what our eternal quest has been.

I chose these four books not as a group, but individually for different reasons. One of these books was recommended to me by a friend while I was reading the others.

But, I could easily see the recurring themes in all these books. No theory – be it physical or philosophical – is final. No finding is absolute. No ‘truth’ is unchallengeable. It is both humbling and invigorating at the same time.

The pursuit of knowledge embodied in each of these books is remarkably similar and provide a rather encompassing insight about humanity’s earnest endeavors over time. But this pursuit may never end, and our body of knowledge is likely to be ever ‘incomplete’.

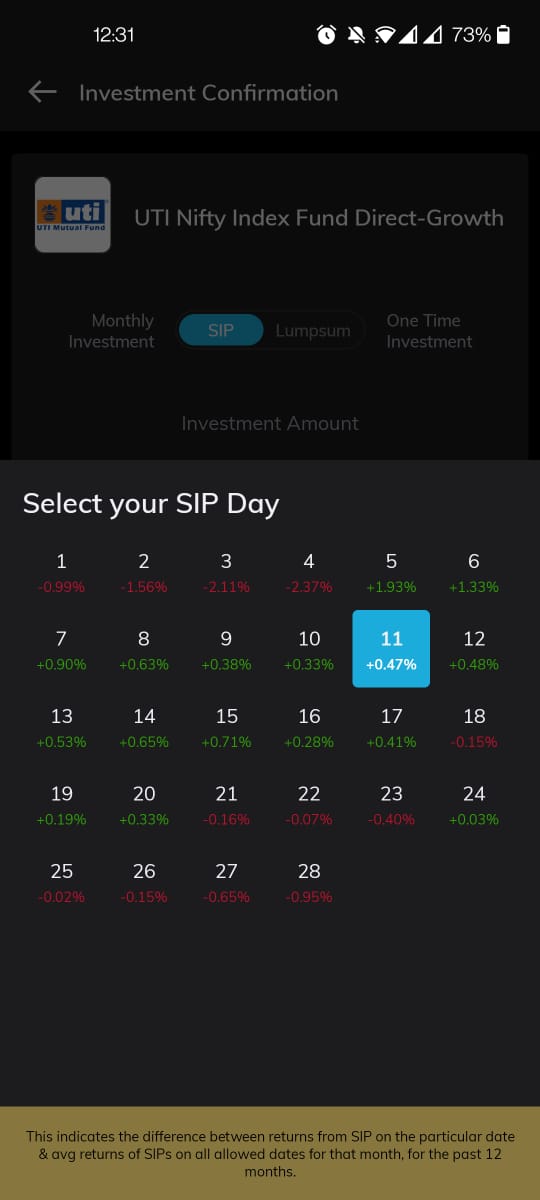

You can tell when a platform marketplace is getting too crowded when useless, misleading ‘features’ get added on to the software in the quest for ‘differentiation’. I ran into a prime example of just such a thing when someone sent me a screenshot of a page from the Paytm Money app.

This page/screen is part of the SIP setup flow of the app. When an investor chooses a fund to set up a SIP, the app shows a calendar to choose a monthly date. So far, so good, and expected.

What is not quite expected is the extra ‘information’ provided in the calendar. Each date is accompanied by a percentage figure (see image). This number purports to show how a SIP on that date has performed relative to the other SIP dates.

That is, each date is accompanied by a percentage that tells you (per the explanation in the bottom of the screen) the outperformance (or underperformance) of an SIP done on that date compared to the average SIP performance for that fund over the past 1 year.

Wow! Right? Now, an investor can choose, for EACH fund they are investing in, the exact date that could maximize their returns!

But, of course, this is BS. For one, the sample size is ridiculously small – 12 data points for each date, and two, using the recent one-year performance for an equity fund for making long-term investment decisions is just plain wrong.

Mercifully, as useless and frivolous this feature is, it is unlikely to cause much harm to investors. As our recent researched article shows, it does not quite matter which date you choose for your equity fund SIP – the returns differential is minimal and entirely up to chance. So, just because you choose a ‘high-return’ date based on this data, it won’t dent your returns significantly.

But that doesn’t make for a good marketing tagline, does it? 🙂

If you’ve been whiling away the hours listening to legends such as Lata Mangeshkar or Kishore Kumar, you’re not alone. And as you returned to yesteryear classics, so too have stock markets gone back to two companies that own the rights to these and thousands of songs. SAREGAMA India and TIPS Industries have seen their stocks hit new highs after 20 years.

SAREGAMA and TIPS own the rights for thousands of songs from the 90s. SAREGAMA owns the rights for over 1.3 lakh songs, TIPS owns rights for nearly 25,000 songs.

The two stocks have gained 10 times in the last 1 year!

So, why the sudden revival of old music? A few developments appear to have led this trend.

An increased demand for streaming music, thanks both to the explosion of such platforms and cheap data, and from the effect of the work-from-home development.

Legal developments that worked in favor of licensing rights of the music IP owners

Companies signing licensing deals with streaming platforms.

Quite apart from these, the fancy for these stocks could also be that markets were picking up on work-from-home beneficiaries! Please note that this is not a review or a recommendation on the industry or the stocks. This is simply a quick take to explain the trend in music stocks.

Music and video streaming platforms

Cheap data and high smartphone penetration are driving demand for music through streaming platforms. The music segment now contributes significantly to the total revenue for the Indian music recording industry. The demand for music also appears to have jumped as millions working from home turned to increased streaming. A survey conducted by Nielsen for Spotify concluded that audio-streaming apps are among the top five ways Indians discover new music.

The OTT music streaming segment is highly competitive with domestic music platforms like Saavn, Gaana & Hungama, as well as international streaming platforms like Apple music, Amazon Prime, Google Play, Spotify & others.

Internet broadcasting & copy right laws

Two, an interesting development on the legal side seems to be working in favor of these companies. The Spotify Vs Warner legal battle in India appears to be leading to favorable thinking in terms of rights and licensing requirements.

The need for licensing agreements pursuant to an interim order by Bombay HC in a recent legal battle points to better pricing deals for IP right owners in future.

Music stocks – business boost

So, how has this helped Tips and Saregama? Well, they are licensing their IP rights on their song library to various platforms. The shift in the way people consume music as well as legal developments have helped companies combat the piracy and licensing issues that they struggled with in the past. This is helping them monetize their IP rights on a significantly larger scale.

SAREGAMA, for example, has inked licensing deals with both domestic and global players including Facebook, Spotify, ShareChat, and Triller, as well as big platforms such as YouTube and Amazon Music

For SAREGAMA, licensing revenue has doubled in last 4 years from Rs. 138 crore in 2017 to Rs. 283 crore in FY2021. This jump comes even as the company reported a decline in revenue from Rs 544 crore in 2019 to Rs 442 crore in 2021. It now wants to invest Rs.200 crore for acquisition of new music over the next two to three years to capture 20% share of new music.

Similarly, TIPS has inked licensing deals with Facebook, YouTube, ByteDance’s Resso, JioSaavn, and Amazon Music. The company, which is also the largest producer of Punjabi films, has initiated a demerger exercise to separate music and film businesses, suggesting that it sees enough promise in the music industry to let it stand alone.

Of course, how steadily these revenue sources can scale up for the companies bears watching.

Occasionally, we get questions at PrimeInvestor about investing in cryptocurrencies. Unsurprisingly, these questions arrive at a higher frequency when these currencies are trading higher and making rapid up-moves. As they are doing now. BitCoin is trading at higher than $56,000, more than 700% up in one year. And there is the new DogeCoin which has moved up 30x in just 4 months!

At PrimeInvestor, we don’t cover these instruments from a content perspective, nor do we conduct research in them. Naturally, we do not recommend our customers/subscribers invest in any of them.

Why? For the following reasons:

They are not regulated in India. The currency is not regulated by RBI (which actively frowns on them), and trading/investing in them is not regulated by SEBI. As such, these activities are to be done entirely at the risk of the investor, without any regulatory cover or oversight. We don’t cover such investment products.

They are purely speculative – there is no tangible underlying asset – either a commodity or a business with cash flows – that drive the value of these instruments. They are purely driven by scarcity of a digital creation, and by supply and demand in the market.

There is nothing to research – Reams and reams of documents have been written about cryptocurrencies, especially BitCoin, but most of them are about global central banks, inflation, and other economic indicators – signals that are used to predict (read: speculate) on the prices of these currencies. And their prices move due to things like a tweet from Elon Musk. These are not things that can be analysed or researched.

Just like the GME story from earlier this year (and ongoing), they are tempting, captivating narratives. But there is little in them beyond material for pleasant daydreams. When you wake up from these dreams, rest assured that PrimeInvestor will be there to guide you along a safer, steadier path to financial security and freedom.

I like to approach my investing with the same mindset that I approach watching India play cricket abroad. The keyword there is ‘abroad’.

See, when India plays abroad (and I mean the SENA countries – South Africa, England, New Zealand and Australia), my expectations are low. When they do better, I am elated, and when they lose, I don’t get too depressed.

I think watching our investment portfolio should be the same. Having realistic expectation means, a boom market (like now) makes us real happy, but a downturn does not faze us much. There is, let’s just say, downside containment of our disappointments 🙂

On the other hand, if we look at our portfolio like watching India play at home (like right now), we expect too much, every defeat is a an unexpected disaster, and a win feels like just ok.

Not good feelings; And makes us act rashly with our portfolio (like ‘resting’ Rohit Sharma :-/ )

How do we form the right expectations, you ask? Glad you did – please read this article from our archives – it’ll set you right!

SEBI’s recent circular on restrictions on both valuations and holdings of perpetual bonds by mutual funds has created a storm – not just among the fund manager community but all the way up to the Ministry of Finance.

The circular on perpetual bonds

The circular, broadly, states the following:

A mutual fund scheme cannot hold more than 5% of its assets in a perpetual bond issued by a single issuer. It cannot hold more than 10% of its total AUM in perpetual bonds in a single scheme.

No AMC can own more than 10% of the perpetual bond issued by an issuer.

Closed-end funds shall not invest in perpetual bonds.

The maturity of all perpetual bonds shall be treated as 100 years from the date of issuance of the bond for the purpose of valuation. Currently, MFs follow the call/put option date to value the yield.

The circular shall be made effective April 1, 2021.

What the circular means

The circular, if applied, shall mean 2 things:

Many funds will not be able to hold such a perpetual bond if their mandate restricts them. For eg. An ultra-short-term fund can’t meaningfully hold such an instrument.

Funds may need to revalue the bonds, and this can lead to mark-to-market losses as yields will be marked up if one considers the date of maturity as 10 years as opposed to 2-3 years.

Funds across the spectrum hold these funds. Banking & PSU debt funds, Low duration funds and balanced advantage/dynamic asset allocation funds are among the larger holders of this instrument. We will put out a more detailed report on fund holdings, if this circular remains.

It is noteworthy that, AMFI, in a response to this circular, has stated that the ‘100-year valuation’ will apply only if there is no traded value to the instrument. Now, this may provide some respite.

But here’s the bouncer. Media reports quote a communication from The Ministry of Finance (MoF) to SEBI – raising concerns about this proposal and the possible panic selling. It has also stated that perpetual bonds are used for bank’s capital needs and requested that the revised circular on valuation of perpetual bonds be withdrawn.

This being the case, we will wait for clarity on what is to happen before we write about it for you. As of now, restraining mutual funds from taking exposure to a highly risky category like perpetual bonds is a good move. However, the valuation norm, at an extreme 100 years, can cause impact on your NAVs. We’ll keep you posted.

When I read non-fiction books, I keep myself daily minimum targets to get through it in reasonable time – at least 100 pages a day, or in some tough reads, 50 pages a day.

With Phil Knight’s ‘Shoe Dog’, I had to set for myself daily maximum reading targets – not more than 150 pages a day – so as to not let my other work suffer.

I could not, however, hold myself to the target – I finished the 400-page tome in a day and half flat. In one word, it’s ‘unputdownable’.

Chandra, my partner from FundsIndia, gave me the book 2 or 3 years ago and exhorted me to read it, and I’m ashamed that I just got around to it. Of course, as with the other books I am reading these days, I am wishing this book existed and that I read it, 15 or 20 years ago.

‘Shoe Dog’ chronicles the advent of Nike and the adventures of Phil Knight. It captures the period between 1962, when Phil first embarked on the journey (literally, actually), and 1980, when the company went IPO and Phil and his company, finally, made it.

It took 18 years to become an overnight success.

The tribulations that they went through during these years are, at the same time, totally pedestrian and incredibly arduous. From backstabbing partners to disloyal employees to relentless problems with bank and cash flow to lawsuits to fighting government bureaucracy – there is not a stripe of a problem they seem to have quite missed out on.

Through it all, they – Phil and his coterie of carefully assembled colleagues – persisted somehow – with a sleight of hand here, a slice of good fortune there, and honest to goodness hard work everywhere – to realize their vision and dreams.

It is a tale of dogged perseverance – and Phil alludes to it often in the book – the Oregon spirit. The state of Oregon is famous for the trail that it’s named after it – the Oregon trail. The path followed by migrating settlers who moved west in the early 19th century. The adage that accompanies the legend is that “The cowards never started and the weak died along the way. That leaves us, ladies and gentlemen. Us.”

And it’s not a dry business book either. As an autobiographical memoir, Phil opens up with extraordinary candour about his personal life as well. And it will be hard to be dry-eyed at the end of the book. And the quality of writing – the style and the narrative flow – is absolutely top-notch. It has all the flair and cultivated skill of a well-published author. The language is alternately poetic or dramatic as the narrative calls for. Not a dull moment.

I have a bit of a personal connection as well. Nike was my first “employer” – I interned at their sprawling headquarters in Beaverton, Oregon for two hot summer months in 1994. I caught a glimpse of Knight only once – as he walked by with his lunch tray in the cafeteria. By then, he was a god among men, at least in that campus. The road that led up to the main building from the outside world was called Bowerman drive (I used to cycle to the office – I would ride up this drive to the security block where they would hand out canteen coupons for people who biked to work). Back then, I had no idea about that name or the other names that the remaining lanes in the campus were called.

I wish I did – the streets are all named after the people who were instrumental in the founding of Nike – all who are the protagonists of the story in the book.

My key takeaway from the book is this one thing, that is not said out loud in the pages. Phil Knight did not invent anything – sneakers were there before him, his partner invented waffle soles, people outside the company came up with the Air idea, and heck, even the name Nike was a colleague’s idea. But he had one thing – a passion for running and good shoes. Essentially, he had taste in footwear- he could tell bad shoes from good shoes. And he turned that love into a business and he never, ever let go.

Few books have caught the interests of the Indian investing public as well as the book ‘Coffee Can Investing’ by Saurabh Mukherjea and others.

Fewer still investment methods have found a fan following as the stock picking process recommended in this book.

Admittedly, I am a bit late to this party. Nevertheless, when I picked up the book and read through it, I could see why investors were enamored with it. The sub-title of the book captures the lure well – ‘The low-risk road to stupendous wealth’. Who would not find that enticing?

There are few problems with the book – more on that in a bit – but, the book is definitely a good read and worthy of recommendation. Please note that I am recommending the book, and not necessarily the investment process detailed in there. Please read and adapt it to your needs as you see fit. (Side note: Please don’t ask when PrimeInvestor is going to come up with a CC portfolio – we have our own philosophy and methods 🙂 )

The book’s premise is beguilingly simple – pick stocks that have a proven track record (of 10 years or more) of growing their revenues and have high return on capital employed (ROCE). The formula undergoes some changes when applied to financial services companies (looking at loan growth). But that is the simple step.

The tougher part may be to hold on to this portfolio without disrupting it for a period of 10 years. No profit booking in peak markets, no discarding of ‘losers’ – no activity in it at all. If you read the commentaries on this book, you will find many people taking issue with this hands-off approach. For example, when companies have governance issues as they often do, should we still keep holding? Or get out and find a new CC stock? That’s a tough call to make.

But Saurabh and co present this method with conviction and by backing the conviction with data from the past. The book is replete with tables of returns from various such portfolios created at different points in time, all showing the merits of both the stock picking methods and the virtue of patient holding.

The book also touches on some tangentially related topics along the way – about the Indian real estate market, on mutual fund expenses, investing in small-caps etc. Most of you, I think, will skim along these chapters, as I did. There is not much new there.

The book is a bit outdated though, in some respects. The authors keep mentioning that long term capital gains on equity investments is zero. We all know that since 2018, that has not been the case. Similarly, they advocate, in a specific case, investing in the dividend option of a mutual fund, which is also an anachronism for today’s world. Given that it’s been 3+ years since these changes came to effect, one would have thought that the book would have seen an edited version published.

And while they recommend mutual funds for small-cap investments, they provide little guidance on how to go about picking those funds (of course, PrimeInvestor subscribers have ready access to the top funds they should invest in).

Nevertheless, I liked this book for these reasons:

The stress on the virtues of patience in long-term investments – which is the achille’s heel of investors in general and Indian investors in particular.

The commitment to a diversified portfolio – including other non-equity investments as well.

The emphasis on looking at the costs of investing – like expense ratio, brokerages etc.

And, I have to mention a word about the writing style – it is top-notch. The book makes for an easy read – not necessarily a quick read, since there are many concepts to be digested on the way.

Readers of this book will come out with a better understanding of the Indian equity markets and will be more informed about stock-picking methods. And just those make the book a worthy read.