Note: Articles attributed to PrimeInvestor Research team are collectively researched, discussed, and authored by all members of our core research team made up of Aarati Krishnan, Vidya Bala, and Bhavana Acharya.

Last week, we suggested an asset allocation plan for these tough times and also mentioned some equity funds that suited current market conditions. We also asked investors to deploy their money in equities in a phased manner. But given that the Nifty50 is busy taking out new lows with stunning rapidity, what are the Nifty levels at which the market gets really cheap, or attractive to invest lumpsums in? This strategy note is an attempt to answer this question.

The strategy

While investing a big sum at a market bottom is every long-term investor’s dream-come-true, market bottoms are often crystal clear only in hindsight. When you’re in the midst of panic and mayhem, it can be very hard to identify such lows.

We don’t claim to know exactly where the market will bottom out. But as fundamental and long-term investors, there’s one guidepost that we thought we could use – Nifty50 valuations. Here’s an attempt to identify the levels at which Indian markets will trade either at fair value or below it, so that you can deploy your money at reasonable levels.

Do note the following:

- This is recommended only for investors who can take short-term losses for a better shot at returns over a 5-year plus horizon. This is not a substitute for your regular investments towards goals through SIPs, which must continue at all market levels.

- Do not liquidate emergency funds or money needed in the next 2-3 years to make such one-off investments.

- The strategy is not based on technical analysis. It uses valuation as a metric to identify approximate levels that are attractive to invest into the market.

Estimating the Nifty levels

The starting point for estimating attractive market levels is the earnings estimate. In this exercise, we used the Nifty50 earnings estimate for one-year forward (FY21) as a starting point to gauge good levels to invest.

Currently, research reports tell us that the consensus estimate for Nifty50 earnings for FY21 stands at about Rs 660. But past experience tells us that this is subject to fairly big misses. Today, the achievement of this number is highly uncertain given two key imponderables.

One, the impact of crude on the large oil and gas companies besides issues ailing the banking sector. According to a February earnings review report by Nomura (India Equity Strategy), the decline in oil prices and shrinking refining margins can hurt the Nifty50’s earnings by as much as 5% for FY-21.

Two, the business disruptions caused by the coronavirus outbreak will also take a toll on revenues as well as earnings. We are assuming a 5% earnings dent in FY21 on account of this.

Allowing another 5% buffer in addition to these risks will lead to Nifty50 earnings falling 15% short of the current number in FY21. Thus, the discounted FY-21 earnings per share for the Nifty50 comes to Rs 561.

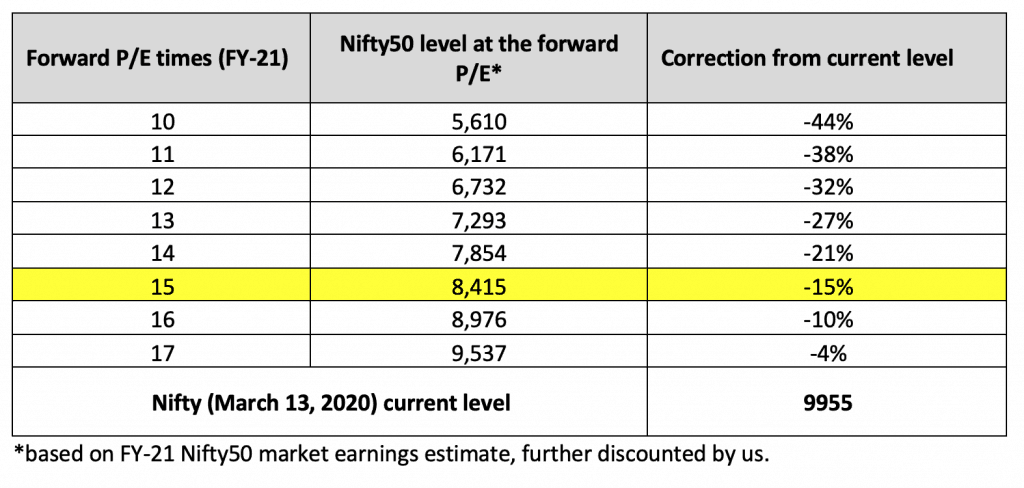

Having arrived at this EPS, the next step is to guess the likely PE at which the Nifty50 will be either at long-term averages or below them. Here, we used the history as our guide. In severe bear markets like 2008, Indian markets bottomed at forward P/Es close to 7-8 times. But the 15-year average forward P/E for the Nifty50 is about 15 times. Based on these indicators, here’s a matrix of the Nifty50 levels which may be good entry points for investing lumpsums into equities.

What the table above tells is that the Nifty 50 would need to touch around 8400 levels (please don’t measure the exact level, and allow for a deviation of at least 1 percent) for you to deploy at the long-term average P/E of 15 times. That means another 15% correction from here. In other words, meaningful valuation-based deployment can happen post that.

Since we cannot be sure how deep the correction will be, you could use the following as a guidepost:

- Invest one tranche at the current levels since it is close to a 20% correction from January 17, 2020

- Invest a second tranche when the P/E moves to the long-term average territory of 15 times forward

- Invest the maximum proportion below 15 times (below Nifty 8400 levels).

What if the correction isn’t that deep? It is okay because the markets may test recent lows multiple times over the next few months and you would anyway be investing through SIPs.

Please note the following:

- The P/Es are forward fiscal earnings estimated by analysts and further reduced by us. These earnings can well be downgraded further. This is the reason we went with lower P/E and Nifty levels.

- The Nifty levels above are NOT based on trailing P/E. So just look for the Nifty levels we have mentioned.

Where to invest?

Even if you know the right levels to invest, deciding what stock to pick up can be difficult, especially if you need to react with lightning speed. The lows of the past week also tell us that it isn’t easy to buy individual stocks, even if liquid, in the midst of mayhem and panic.

However, there are still good alternatives to buying individual stocks at market lows. Simply buy the market itself through index funds! You can invest in the Nifty 500 or in a combination of Nifty 50 and the Nifty Midcap 150. Please note the difference in returns in this combination has not been high, with latter (the Nifty plus Midcap 150 in a 70:30 mix) delivering just marginally higher returns in the past.

| Option 1 | Allocation | Comment |

|---|---|---|

| UTI Nifty 50 index fund or Nippon India ETF Nifty BEES | 70% | 5-year returns of this combination has beaten the Nifty 500 100% of the times by an average 0.63%, from 2005 onwards (data available since then for the Midcap 150). We took the primary largecap index where you can be certain of staying with market flavor. We took the midcap index that can deliver some alpha from the 101-250th stock by marketcap. To this, we applied various allocations (50:50, 60:40 and so on) to arrive at the one with the highest certainty of beating the Nifty 500. This combination can also deliver higher in the initial leg of the rally when the upside is limited to quality bluechip stocks from the Nifty 50. Volatility in this portfolio can be marginally higher than the Nifty 500. |

| Motilal Oswal Nifty Midcap 150 fund | 30% |

| Option 2 | Allocation | Comment |

|---|---|---|

| Motilal Oswal Nifty 500 Fund | 100% | This index delivered an average 13.2% annual return on a 5-year basis when returns were rolled from the year 2000. This index holds potential to deliver better in a broad market rally. It’s akin to buying the entire market. However, it may underperform if the initial leg of the rally is restricted to select large caps. Since it goes beyond the 250 stocks in option 1, the rest of the index, albeit smaller in allocation, can beef up returns a bit over the longer term. |

Please refer to our Prime Funds section to know more about the index funds mentioned above. At this juncture, it is hard for us to pinpoint which option works best. What we know is that historically their difference has not been high. So, use one of them as a proxy for buying the market.

Please note that this strategy does not guarantee downside protection in the near term. You need a minimum 5-year time frame for it to pay off.

35 thoughts on “Prime Strategy: At what Nifty levels should you be investing?”

I have been reading this analysis a couple of times since yesterday. At the outset, very straightforward and correct approach.

Challenge is to estimate by how much Nifty earnings fall and what multiple to pay.

In a global recession (say, base case), the NIFTY earnings can fall -15% to -30%. If we add Corona, then all bets are off.

Should we be comfortable paying 13-14x whatever EPS we estimate. So probably another 20% below the targeted 8415 levels. Appreciate views.

True we cannot be sure how much earnings will fall for sure. Which is why 10x is also given ? Thanks, Vidya

Good one.

I want to know some thing what fii get profit on sale on this lavel ?? And if fii are sell why dii buys ?? From last fifteen years this this happens. I ask this question to somany analytics but nobody answered can you clear my this doubt? I

Replied on twitter. Vidya

Hi Team,

I am investing in Mutual Funds from the past 5 years… Not even a single SIP is missed out or Never sold a single unit.

and my SIP amounts are increased over 5 years and all sip’s are goal-based. My only investment is SIP’s, no real estate.

The returns after investing over 5 years are negative. can you help me to understand this?

Can I get negative returns over 10 years or 15 years period? I am a little afraid of what if markets crash at the time of my kid’s education goal finish year.

Do I need to diversify my asset allocation to RealEstate or Gold

My goal is to get returns of 10 to 12% at any point in time after investing over 10 years. is that possible?

Hello,

The past 5 years hasn’t actually seen a longer corrective phase, and a good part of it was a very strong rally. So SIPs were averaging investment costs higher more than they were averaging lower. This apart, there have been 5-year periods where equity markets have been loss making; it’s only over 7 year periods that markets haven’t lost.

This is why asset allocation is very important – returns would have been much better if 35-40% had been invested in debt for a 5-year investment period. Since you have a longer holding period, you don’t need to invest this much in debt. But you do need at least some allocation to debt to prevent return erosion in markets like these. You need to adopt a portfolio approach that combines equity, debt and different categories in both. If you need reference or readymade portfolios, you can look through Prime Portfolios (link).

SIP is a method of investing, it is not an investment itself. You’re investing in equity mutual funds, not in a SIP. The primary benefit of SIP is that it allows investing smaller amounts regularly, which is useful for those who don’t have big lump sums to invest, nad because it makes investing a discipline.

Gold is a hedge as well, but we don’t recommend gold at this time. Please read part about gold in this article: link. Real estate does not guarantee returns, is highly illliquid and subject to several other risks, and it’s hard to identify which locality to invest in. It also calls for high quantum of investment. Please continue your SIPs as it will help in markets like these.

Thanks,

Bhavana

Thanks for your very detailed reply. As always No 1 rule in personal finance is to continue investing.

Is it okay to buy Nippon ETF NIFTYBEES? Looks like it’s not reflecting Nifty and going at a much higher premium more than tracking error.

Also for Motilal the ETF available is either midcap 50 or midcap 100. Shall I buy one of them?

Hello Sir, We are constrained from providing recommendations on the blog. Please write to contact@primeinvestor.in IF you are a subscriber. thanks, Vidya

Amidst the din of ‘expert’ opinions doing the rounds, this comes out as a clear and crisp piece of advice.

Enjoyed reading the note !

Thanks! Vidya

Excellent, timely and very useful. Thank you

Thanks! Vidya

Hi,

Do you recommend specific stocks? I suppose you assess the constituents of a fund before recommending (or not) an MF. It would be very useful to have your views on specific companies for those of us who prefer going long a stock instead of MFs. (Obviously, market moves and other factors can affect the stock but it would be great to know that an expert has at least assessed the fundamentals).

Thank you

Yes, we plan to cover stocks very selectively in a quarter. Current subscribers will have access to it at no extra cost. But in periods such as he present fall, indices would be a better option than stocks in our view. thanks, Vidya

Hi, Can you please write about and explain why many debt funds have been giving negative returns past two week, thank you

Hello Sir,

Yields have been volatile and that is one reason. In these times, such volatility is to be expected other than in liquid funds. other than that, funds that held YEs bank have seen a fall. If there is any other major event trigegred fall, we will analyse. Vidya

thank you

Great Article!!

Being rational in the time of chaos is difficult. This article gives some ideas.

Thanks.

Thanks! Vidya

Thank you for guiding us on the right levels to buy. I’ve read that all index funds are going to see tracking error due to Yes Bank lock-in. How would that impact investors? Should one ignore tracking error?

YEs, it is a concern. Funds have represented. It will be a an anomaly and we hope they are given some relief as ETFs too will be hurt and that will be a big deal. thanks, Vidya

Great article Ladies. Keep up the great work. This drives some sanity in thinking about investments, going forward

Thank you. Vidya

Comments are closed.