- Inconsistent performance among funds in this category makes it hard to pick a quality one

- Increasing credit calls by these funds changes the risk-return profile

- Better returns for the same to lower risk possible through other newer categories

For long, conservative hybrid funds (predominantly consisting of the erstwhile Monthly Income Plans or MIP schemes) were sold as options that would provide regular income through dividend. In 2013, when dividend distribution tax was made uniform across debt funds, the dividend lure took a hit. In Budget 2014, when the definition of long term, for capital gain purpose, became 3 years from 1 year, MIP lost further sheen.

Finally, it moved to be a category to earn better-than-debt returns without the risk of pure equity. The equity and debt blend also helped introduce either equity or debt into a portfolio. While this last proposition appears well-grounded compared with earlier reasons for which they were sold, we don’t recommend investments in funds from this category. Three reasons:

- Inconsistency. Performance of hybrid conservative funds is increasingly fluctuating, with few funds able to steadily deliver above-average returns.

- Risks.Hybrid conservative funds are not free of credit risk, and this makes them unsuitable for short holding timeframes.

- Performance. Newer categories such as balanced advantage and equity savings have characteristics similar to hybrid conservative funds and are able to better achieve the objectives of the latter.

Changing performance

Consistency measures how steady a fund is, in delivering returns. Consistency is typically backed by a clear strategy that enables it to perform across market cycles. Understanding this at the time of investing in the fund is vital because you need to know if it can continue to perform the way it has. A fund that does well in some phases and poorly in others increases uncertainty about its performance going forward.

On this count, conservative hybrid funds slip. Of the 16 funds in the category (ignoring funds that saw big debt write-offs to avoid skewing the figures), just 5 were able to beat the category average more than 60% of the time when looking at 2 year returns since 2015. On a 1-year and 3-year return basis in the same period, just 4 and 6 funds respectively, were able to consistently beat peers.

Franklin India Hybrid Debt, for example, saw 2-year returns hold above other funds for most 2019 and 2018, but floundered in 2017 having delivered in 2016. BNP Paribas Conservative Hybrid has a similar patchy history, while current high return generator Baroda Conservative Hybrid has only just begun to perform better than peers.

Other funds that were strong performers earlier lost heavily. Aditya Birla Sun Life Regular Savings, for example, used an aggressive equity strategy of holding about 30% in equity to beat peers by a large margin. With exposure now mandated at a 25% maximum, the fund’s returns slipped. SBI Debt Hybrid similarly used an aggressive duration strategy to power ahead, but failed to maintain the pace once duration finished playing out.

Part of the inconsistency stems from funds’ frequent change in strategy in a bid to maximise debt returns at all times and as the profile of the category in an investor’s portfolio kept changing. This saw funds move into duration when opportunities looked promising, but were unable to either time the strategy right or failed to book out of it on time. Or, funds followed accrual but frequently changed portfolio maturities between short and long term papers based on rate cycles. Such a strategy uncertainty does not bode well for steady performance.

HDFC Hybrid Debt, for example, relied heavily on duration from 2015 to 2017. It was premature in this strategy in 2015 which hurt returns; it eventually paid off in 2016. But continued betting on duration in 2017 sent returns back lower and a switch to accrual from there hasn’t yet helped the fund pull back above averages consistently. The fund did not participate much in 2019’s gilt rally. Nippon India Hybrid Bond, similarly, got duration calls wrong and then morphed into a credit risk portfolio.

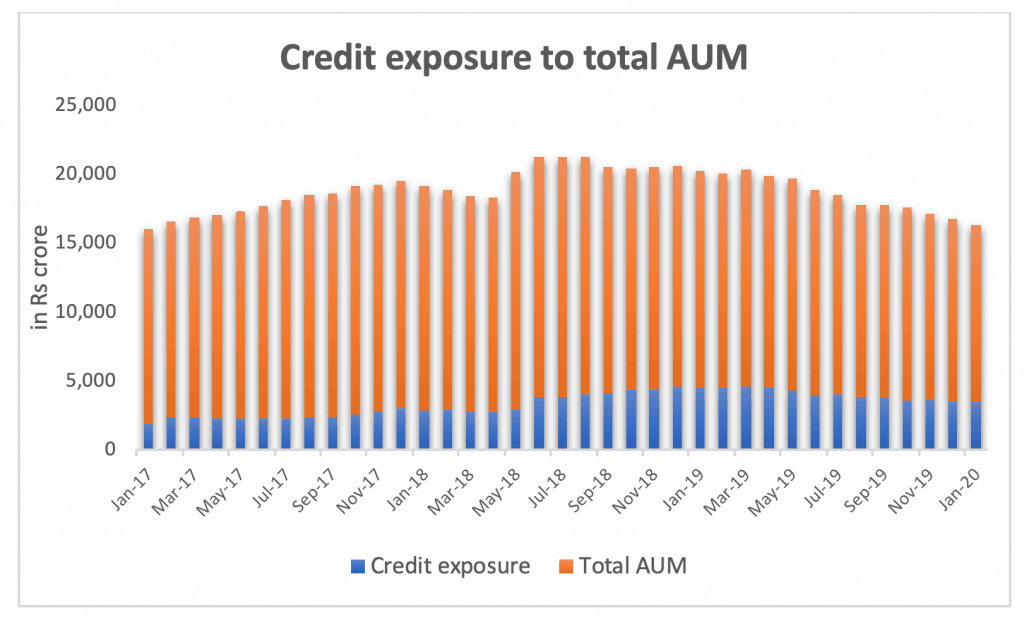

Credit risks creeping up

Credit risk is the one factor often masked in conservative hybrid funds. Earlier, funds played it safe by relying on AAA funds alone while the risk came from the equity exposure. Now, however, risks come both from equity and credit calls.

As a proportion of the overall AUM, exposure to debt rated AA and below has gradually moved higher to 27% now. Up until mid-2018, the credit exposure was less than 20% of the total. Of course, erosion in AUM is a contributing factor to the rise in overall credit risk proportion. But breaking this down into individual funds also shows the same trend.

Half the funds in the category held at least 15% on an average in lower-rated papers over the past two years. A third held an average of 20% in such papers. For example, ICICI Prudential Regular Savings has held between 40-50% of its portfolio in AA and below papers for over a year now. This dampens its long-term consistent performance record. Nippon India Hybrid Bond had a whopping 60%-plus in low-rated papers, in line with a credit risk fund.

These hybrid funds additionally are meant to suit conservative risk profiles, given that it provides debt-plus returns without the risk of equity. Taking on credit risks renders unsuitable for their basic purpose.

Credit calls on the debt side aren’t wrong and they do hold potential for higher returns. However, credit risk needs a long timeframe in order to absorb any potential losses which conservative hybrid funds don’t normally call for. The debt events of the past year have resulted in write-offs in several funds, on their DHFL exposure, on Anil Ambani group, IL&FS group, and Sintex exposures. Axis Regular Saver, for example, held about 7.3% of its portfolio in DHFL papers. Its 1-year return dropped from 5.3% to a loss post June 2019.

These hybrid funds additionally are meant to suit conservative risk profiles, given that it provides debt-plus returns without the risk of equity. Taking on credit risks renders unsuitable for their basic purpose. Besides, if you were to take on credit risks, a pure credit risk fund would serve better and deliver higher returns as well.

Better performers

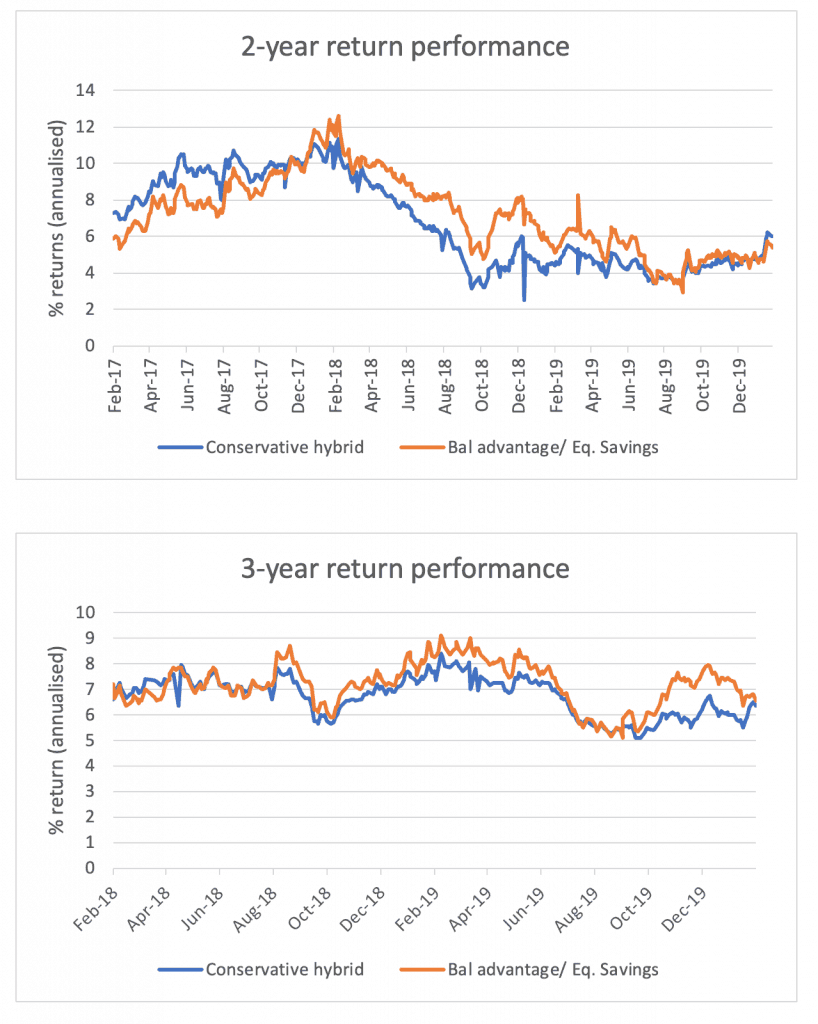

In the past 5 years, newer categories such as equity savings and balanced advantage funds (does not include dynamic asset allocation) have fitted themselves better to achieve the objective that hybrid conservative fund set out to do. These funds use pure equity, debt, and derivatives to bring in a low-risk fund with debt-plus returns. These funds have the additional advantage of being equity-oriented from a tax angle.

Given that the categories are new and that funds have changed allocations post new categorisation, there are only a handful funds that have followed an investment style of combining equity, debt, and derivatives and can be compared. Returns for these funds, on an average, beat conservative hybrid funds considering the period from 2014 onwards. 1-year returns over this period saw equity savings/ balanced advantage average beat conservative hybrid category 64% of the time. The ability to deliver returns improves as the timeframe stretches to 2 and 3 years.

A higher open equity exposure is one key factor that pushes returns for these funds. Apart from a few, these funds tend to have 30-40% in open equity. However, on the risk front these funds do not fall behind conservative hybrid funds thanks to the low volatility and safety of the derivative and accrual-based debt strategy. This apart, being equity-oriented funds, they are taxed at lower rates than conservative hybrid funds for those outside the 5% tax brackets.

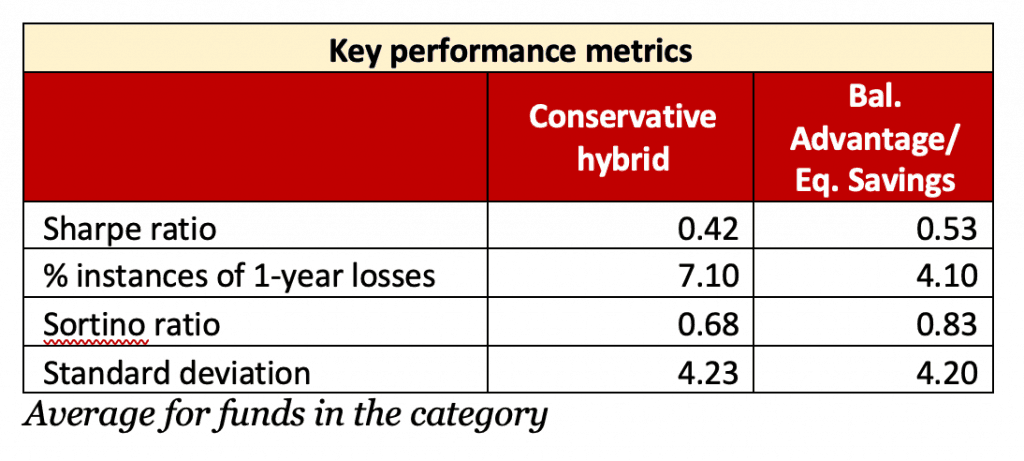

On metrics that measure risk and return – volatility, downside containment, Sharpe ratio (measures risk adjusted returns), and Sortino ratio (measures downside volatility) – equity savings/ balanced advantage funds score better than most conservative hybrid funds.

What it means for you

The conservative hybrid category losing potential has these takeaways for you:

- It is far more efficient to build your portfolio using pure debt and pure equity funds. Substituting an underperforming fund is easier with pure debt or equity funds. Conservative hybrid funds have limited choices and would require you to re-allocate among your other funds as it feeds into both equity and debt components of your portfolio.

- If you have a timeframe of 1.5 to 3 years, use funds in categories such as equity savings and balanced advantage if you wish for marginally higher returns than pure debt funds (Hybrid – Low Risk in Prime Funds) and want tax efficiency. Else, you can stick to pure debt funds that fit your timeframe.

- If you already hold conservative hybrid funds, use our review tool to assess their performance. Else, consider moving to pure debt or pure equity funds depending on your timeframe.

Also Read : A Low Risk mutual fund option for the conservative equity investor

18 thoughts on “Prime Views: Why you should avoid this fund category”

Hi Team,

Though you have discouraged investments in Conservative Hybrid Category, would be keen to know your views on Parag Parikh’s NFO in this space. REITs/INVits is an additional attraction here..

Also if you can throw some more light on the issue of having some portion of your long term ‘asset-allocated’ debt portfolio (say 20-25%) in such hybrid categories to earn 200/300 bps more than the average. Is that advisable?

Would also like to call out that I am very impressed by all the work that you have been putting in. (Rolling return Tool is amazing!!)

Kudos to the entire team.

Thanks.

Regards,

Deepak

We do not have an opinion on the Parag Parikh fund. Please note that hybrid funds are not debt fund substitutes – it also depends on which type of hybrid fund you are using. We do not also have a long enough record for balanced advantage/equity savings funds to know what their returns can generally tend to be over time. We have discussed balanced advantage funds here. – thanks, Bhavana

What are your thoughts on the Canara Robeco Conservative Hybrid Fund? The current debt portion seems stellar and returns have been good too.

Please use our MF Review Tool for our views on funds. – thanks, Bhavana

What is the outlook on an Aggressive Hybrid equity fund? Are they suitable for investors in such market conditions?

There is no separate outlook for each category. In general, hybrid aggressive funds have become a lot more inconsistent. We have mentioned it in our last prime funds review – https://primeinvestor.in/prime-funds-review-changes-to-fund-recommendation/ thanks, Vidya

unable to read this article even after applying for 14 days free trial

Hello sir,

Sorry about that. It should be accessible now.

Thanks,

Bhavana

Which theme according to you is investment strategy for next 5 years for a high risk profile investors.

According to me small cap, value and credit risk will do well from here on.

Hello sir,

You can find theme/strategy funds recommended in Prime Funds. You can find our outlook for 2020 here for equities, and here, for debt. where we discuss what can work in the coming years. But briefly, yes, there are accumulation opportunities in midcap/smallcap and value-based strategies. We’re a little more wary on credit. Do read the articles, and their related outlooks for a better understanding of what our views are.

Thanks,

Bhavana

Changed my perspective towards conservative hybrid funds. I used to prefer Chf against BAF

Hello,

Well, depends on the timeframe. We don’t prefer BAF for long-term portfolios either :). As we’ve noted in the last what-to-do section, using pure equity and pure debt funds is a lot more efficient and easier to manage than hybrid funds. For short trimeframes, yes, BAF or equity savings will work well.

Regards,

Bhavana

Nice article. Two questions on balanced advantage/equity saving fund

1. What is the credit risk exposure on these funds?

2. You have mentioned that these funds are relatively safer due to derivatives and accrual based strategy. What prevents them to follow duration based strategy? Is it by regulation?

Hello,

1. Credit exposure is low for almost all funds, except for a couple. Credit calls aren’t yet a problem for these categories, and given that debt exposure is not the majority if the portfolio anyhow, they may not take to it. The return drivers so far come from juggling the equity exposure more than credit calls.

2. Nothing prevents funds from taking duration calls :). They just haven’t, even over last year when there was enough opportunity. Some funds did a small bit, but like with the answer to the earlier point – the extent of debt exposure is not that high, and funds tend to typically limit how much they played around on the debt side. Aggressive hybrid funds do the same thing. You will always have outliers, but the general trend is to buy and hold on debt.

The issue is not with duration itself. If managed well, it can certainly help returns. Dynamic bond funds, for example, are entirely based on getting duration calls correctly and funds do deliver. We have a long-term gilt fund in our long-term recommended portfolio and in Prime Funds.

The problem with conservative hybrids was the constant changing of strategy that creates confusion on where returns are coming from, what the fund should be doing, etc. If it is a clear strategy of dynamic debt management to play rate cycles when opportunities arise, then it can work well. When it isn’t, and there’s a continued shift between various debt options, then returns can be affected. Hope it’s more clear now.

Regards,

Bhavana

Thanks Bhavana for the quick reply and answering my query. Looking forward to your article on value investing analysis.

Superb article and I fully agree that Conservative Hybrid kind of funds SHOULD be avoided. I honestly wish you had this service and I knew about it 1.5 yrs back. I have learnt it the hard way. I had investments in both ABSL Regular savings fund and Nippon Hybrid Bond fund. After a couple of haircuts on the debt side (ILFS ), I decided to exit both the funds and had to pay STCG. But still it was better as it had many more heavy draw downs after I exited the fund!! This is classic case of funds taking unnecessary risk in non risk averse investors portfolio. On another note I have invested about 15% of my portfolio in L&T Value fund for last 3 years and the returns have been way LESS than even bank SB interest rate!!! Grateful if you can check the statistics and do a similar article on Value funds. Does it make any sense today to invest in this type of themes or better stick to the general trends. Looking forward to your thoughts. Thanks .

Hello sir,

Thanks for the appreciation! An analysis of value investing and what it takes to be a value investor is in the pipeline 🙂 The divergence between these funds and others is stark with the recent market turnaround. Regarding L&T Value specifically, the fund was earlier a mid-cap oriented fund – it was aggressive, somewhat opportunistic and not really value despite the name. Post re-categorisation into the value category, the fund began changing strategy to become more value-based. At the same time, the fund was gradually reducing mid-cap/small-cap allocation – but in the 2018 correction, the mid-cap exposure hurt it. So it’s been a tough time for the fund as it was adapting its portfolio and strategy.

Regards,

Bhavana

Thanks for the good insights.

Comments are closed.