Low interest rates and rising inflation are a dilemma for savers. There is a constant conflict between risk and return. As far as the retail investor is concerned, he looks forward to being ‘protected’ by the regulators. Financial literacy does not come easy and ninety percent of us would not know the difference between a fixed deposit and a debenture. And we would be forgiven in thinking that the term ‘secured’ debenture or bond means that every rupee we invest is safe! But where should we draw the line in the search for high interest rates?

In this context, of late, I notice a lot of teasers from online platforms such as jiraaf.com, clubinvest.in which promise higher yields than I can get from rated / listed debt instruments. I find that behind the high interest rates, the risks on many of these offerings are beyond comprehension to the layperson and that it is our regulatory structure that permits such easy access to small investors’ money. The more we try to legislate, the more the focus is on the micros, missing the big picture. Regulators tend to be reactive rather than proactive. This is the single largest flaw in our regulatory structure, that gives rise to so many scams and rip-offs.

Regulation of online bond platforms

Recently, there has been a reactive move from the regulator to regulate ONE of these avenues. This recent SEBI circular tries to regulate these platforms. One of the clauses reads as under:

“An entity acting as an online bond platform (OBPP) on or prior to this circular coming into force, shall cease to offer products or services or securities on its OBP other than the following:

* Listed debt securities and

* Debt securities proposed to be listed through a public offering.

Such OBPP shall divest itself of offerings of other products or services or securities”

Putting this in context

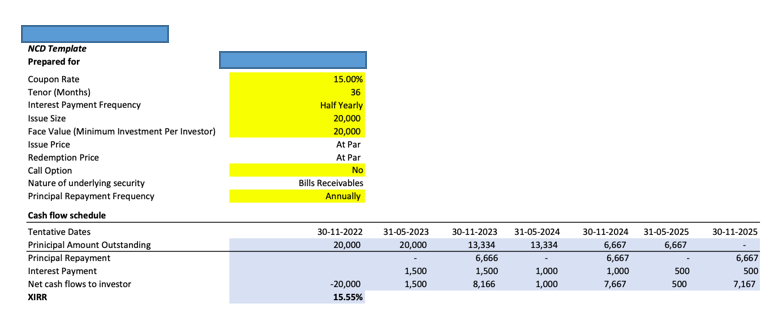

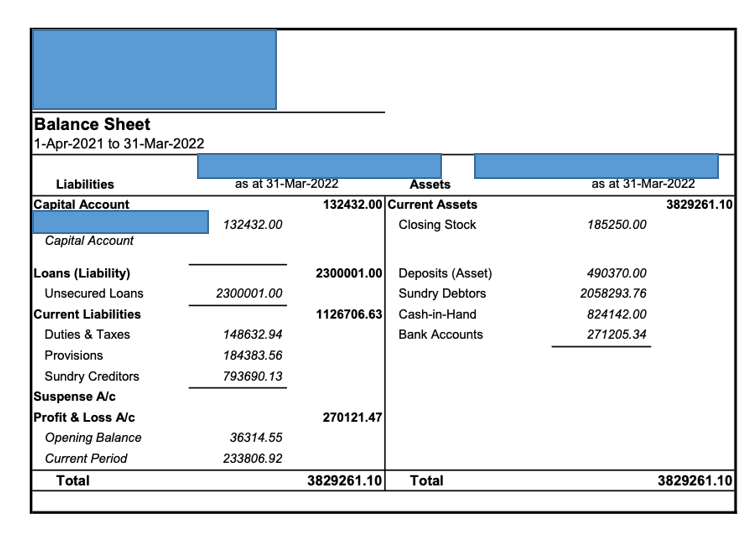

Let me give you an example of one of the bonds that was being hawked on one of these platforms. Below are the terms of the bond. The balance sheet of the borrower is presented after it.

It doesn’t need great balance-sheet-reading skills to decipher that the capital invested by the entrepreneur in the business you’re lending to, is negligible. The equity capital of Rs.1.32 lakh, is supplemented by unsecured loans of Rs 23 lakh. I doubt if any banker would even give this borrower a second look. I also read elsewhere that the fund-raise they plan under this offer is Rs.35 lakh.

Red flags

The sustainability of this firm would depend on how much funding it can raise quickly. This is not a risk that should be taken by a lay person. There is no credit rating either. I do not see the name of a trustee for this ‘debenture’. In case of a delay or default, one would be dependent on the intermediary who sold this bond to us. There is no liquidity on the debenture once you buy it. There is no listing either.

Some of the bond offerings are intended to fund start-ups. When we invest in debt instruments raised by start-ups, we run the risk of default / delays to an unknown extent. Most of them would be in the cash burn stage, have high working capital needs and depending on further fund raising from PEs/VCs etc to be in continuing existence.

In the above example, the promise of repayment is focused on expected future performance. The retail investor cannot have the ability to judge this.

Some of these platforms also offer you debt products that are labeled as ‘leasing’, ‘invoice discounting’ ‘factoring’ or some other terms. These are all high-risk activities. Take ‘invoice’ discounting. If the supply is to a well-known name, finance companies would queue up to provide finance against that. The fact that retail investors are expected to provide finance against receivables reflects on the risks of the supplier.

Today, banks and NBFCs are flush with money. Any entity that is credit-worthy can tap them for debt at reasonable rates of interest. Therefore, when a start-up or any business entity skips the institutional route and comes directly to the retail investor for money, it should tell us that such firms may not have a bankable story.

I am very distressed at the idea of such small companies raising money from retail. It is a risk that should be best left to institutional investors/bankers.

A word of caution for retail investors

As a retail investor, you have to realise that there is no return without risk. When someone promises you a very high interest rate, pause. Unless the business earns a return on capital higher than what it gives you, it cannot repay you. And if it does earn such a high rate of return, it is unlikely to need money from such informal sources, as institutions would queue up to fund it. Perhaps the company is too small to be of interest to lenders. However, giving them access to retail is not a good thing.

Such unlisted bond offerings are likely to be curbed by the SEBI circular. The circular gives a time window of three months by which these online bond platforms will need to register with the regulator. Thereafter, they can offer only listed bonds. There is no restriction on private placements (offer to less than fifty investors). I see a renewed aggression in some websites to use this three-month window to push what they have on hand, using webinars and social media bombardment.

But will that mean all of these platforms will become brokers and such unlisted lending will cease to exist? Not necessarily. One cannot rule out these platforms taking a different shape – not issuing bonds that are in demat form. There could emerge other forms of borrowing that may not come into the purview of SEBI. One would need to watch what form and shape the current and emerging crop of platforms take, 3 months from now. Since our legislations are micro focused and activity based, we will not see the end of this crowd funding fiesta.

Listed debt

Then, there are platforms like bondskart or goldenpi that offer listed bonds. You go through a process that is transparent and whatever debt I have seen on such platforms is credit rated. Minimum bond lot sizes vary from Rs 2 lakh to Rs 10 lakh. Yields on offer vary from 7-10%. There may be a stray case of higher yield, but most AA rated bonds will fetch you less than 10% today. Usually, your bond purchases from such platforms are secondary market transactions. Perhaps the broker has ‘warehoused’ these or bought them in bulk and is retailing them with a spread. You get your bonds in demat form, the interest goes to the bank as do your maturity proceeds.

Proposed reduction in market lot

As a further push to retail participation in such bonds, SEBI proposes to reduce the face value of listed bonds issued on a private placement basis from Rs 10 lakh to Rs 1 lakh, reducing the market lot size also accordingly. This will take effect from January 1 2023.

What to watch for

However, the SEBI circular on online bond platforms does not address the modalities through which such bonds can be sold or placed, which I expect would come in once the OBPs are registered with them.

The circular is also silent about credit rating requirements. Investors should note that listing of a bond is not difficult for the issuer and is no guarantee of credit worthiness. It merely allows the exchange to function as a platform on which to trade in such bonds.

The actual ability to exit before maturity would depend on whether you can find counter-parties for your holdings.

Way forward

SEBI has stated its intent of expanding the bond market. Hopefully, they want retail investors to have a happy experience. If it is true, then they must also restrict retail products to highly rated paper rather than unrated or high-risk debt.

Safeguards I want as an investor

As an investor, here are the safeguards I would like to see on any bond offering:

- A proper offer document that is filed with the regulator and available online

- A SEBI approved debenture trustee

- Instrument only in demat form

- A Registrar & Transfer Agent

- Clarity on TDS

- A schedule of quarterly information to be provided to every debenture investor that includes the latest P&L and Balance Sheet signed by the promoter at least

- Full disclosure of shareholding-

- A disclosure of total debt of the entity including off balance sheet debt

A suggestion to the regulators

To the regulators, I have a suggestion. All these activities are what a bank or a licensed finance company should be doing. In India, the thinking is that if the law does not prohibit something expressly, it is permitted. Instead, make the laws such that if something is not expressly permitted, it is banned. Especially when it comes to money. And make sure that those who violate are behind bars for a couple of decades.

A final word to retail investors

As an investor, when you put money into shares, you know your risks. In debt instruments, you have to have far more knowledge about the borrower. You can punt on a share. It depends on how others in the market behave and is driven by expectations.

Repayment of debt depends on knowing the financial strength and cash flows of the borrower. The borrower needs to have not just the ability to pay, but the willingness to do it!

It is your money. It is your decision to put it where you choose. However, please do not think that there is someone protecting you. SEBI or RBI or the government cannot be looking after every one of us. It is always “Investor beware”.

(You can also read a dated article of ours about bond issuances such as covered bonds offered by such bond platforms here.)

6 thoughts on “The search for high interest rates: where to draw the line”

Very informative article. RBI & SEBI has to bring public awareness about the pitfalls, it’s too easy to lose money in such debt instruments. Thank you!

Wonderful article.

Thanks a lot

Thank you so much for the very important article that could save many investors losing capital. By making this article free , a PrimeInvestor team shows the client loyalty.

The borrower needs to have not just the ability to pay, but the willingness to do it! 🙂

Very apt article on the pitfalls that retail investors need to be wary about. There are no dearth of sub par investment options in the debt space and the past blowups of Ponzi schemes are testimony of how gullible investors are caught in the trap of greed without any risk management. Trying to maximize returns through high yielding high credit risk alternatives blow up ultimately.

Extremely thankful to PrimeInvestor team and Shri R Balakrishnan ji for taking up this topic and bringing it everyone’s attention. Adwords & SEO optimization has ensured that those who search for keywords like – “High FD rates”, “High interest debentures”, “Better than mutual funds” will get ads of atleast half a dozen fintech platforms (WintWealth, GripInvest, Jiraaf, Growpital, KlubWorks, KredX, TykeInvest etc.) offering new-age high yield products for investment. Once a person sees these high yield promising offerings, one thing is certain – loss of satisfaction . [We hope that the damage is contained there with no loss of capital]. Once mind knows that instruments offering *Fixed Income* upto 20% exist and *are accessible*, the yield of FDs, Sovereign Debt, and AAA Senior Secured Listed NCDs [~7.5%] is going to become tasteless. We need to be aware that the moment greed occupies the house of mind, peace & sound judgement are thrown out.

As the learned author has explained – one might get lucky in direct equity and mutual funds (earn 4x or 5x of FD / G-Sec returns without having taken 5x risks); but in debt products the equation is simple – 2x or 3x return of FD / G-Sec returns will definitely imply that 3x or more risk has been taken to earn it. Every cautious investor must keep invoking the eight guardian deities of the eight directions listed in “Safeguards I want as an investor” in the article. And should invest only after being blessed by the presence of all the eight deities.

I hope that all the regulators looking after money market and capital markets take cognizance of the *Fintech* revolution and its far reaching consequences on lifecycle of financial instruments / products (from their origination to delivery and finally maturity /redemption.) We would be really fortunate if the regulators consider the suggestions made by Shri R Balakrishnan ji; till that happens, atleast we investors, for our own safety, must abide by the commandments given in this article.

Thanking you

Warm Regards

Comments are closed.