Fund ratings, at a glance, tell you a little about the history of a fund. For many of you it’s a quick reference on whether a fund is a good one or not. PrimeRatings (Free registration required to access) is a mutual fund rating system. But it’s not simply yet another fund rating tagging on to the list of ratings that are already available. PrimeRatings’ methodology:

- uses a more diverse combination of risk and return metrics,

- looks at fund categories based on their characteristics and investment purpose and not just their SEBI-defined category,

- spreads ratings out into a smoother curve which provides better distinction between funds and circumvents the problem of a sharp jump or fall in ratings

Here’s a look into our ratings process and how we’re different.

Being selective

Not all funds are rated. Funds must meet two basic requirements: AUM and age. The cut-offs depend on the type of fund. Equity funds, for example, need a minimum 3-year timeframe of existence and an AUM of Rs 100 crore before we rate them. Index funds have a lower AUM requirement. Liquid and ultra short term funds have a far higher AUM cut-off at Rs 1,000 crore and Rs 500 crore, but have a shorter timeframe.

We have different age and AUM cut-offs because each fund type is different. Liquid and other very short-term funds certainly don’t need a long history as their nature allows us to judge performance quickly. But given their high institutional interest, a large AUM is more prudent. Equity funds, on the other hand, need a longer timeframe to judge performance but can manage deftly even in smaller AUMs.

The next eligibility criteria is the category. Sector and themed funds are not rated – themes and sectors are tactical calls. Rating these funds as 5-star or 1-star serves no purpose. One, it doesn’t shed light on the potential of a theme. Two, it can additionally mislead you into thinking a fund is good simply because it holds a high rating.

We also don’t rate categories where the number of funds are too few to show meaningful results, such as multi-asset allocation funds, US-based funds, or emerging market global funds. We don’t rate closed-end funds.

How to read our ratings

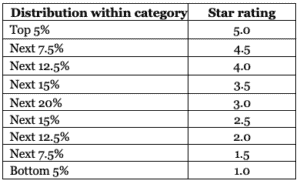

Based on metrics and weights, each fund has a score. The scores are rated on a curve in the distribution as in the table below.

In the below scale, 1★ indicates the lowest in terms of relative performance within the rated set, moving gradually higher to 5★. For example, 5★ funds are those in the top 5% in terms of score for the rated period. We update PrimeRatings every quarter.