When you compare the regular and direct expense ratios of mutual funds, how do you decide something is expensive or not? At PrimeInvestor, we have a new tool to help you make this comparison. But the tool alone can’t help you decide. This article will tell you how to use it effectively and what other factors should go into deciding your choice of plan.

Before we get into comparing direct and regular plans – if you are new to mutual funds, we recommend that you read our primer on how mutual fund expense ratio works.

You can also read our article on the expense ratio differences across categories to know which categories cost more through the regular plan. This article is for investors who are beginners or have some experience with mutual funds. For the pros, you know what to do – just use the expense ratio tool along with other performance metrics such as the ones in our category rolling returns tool to arrive at your conclusions.

How to compare expense ratios

When it comes to understanding how your fund’s expense ratio compares with others, there are broadly 3 points you need to consider before coming to a decision on whether to hold a fund or not.

#1 Comparison within category of same plan

The first due diligence is to check how a fund’s cost compares with its category within the same plan. For example, if you hold a flexi cap fund under the regular plan, you must know where your fund stands in terms of cost with its own category under the regular plan.

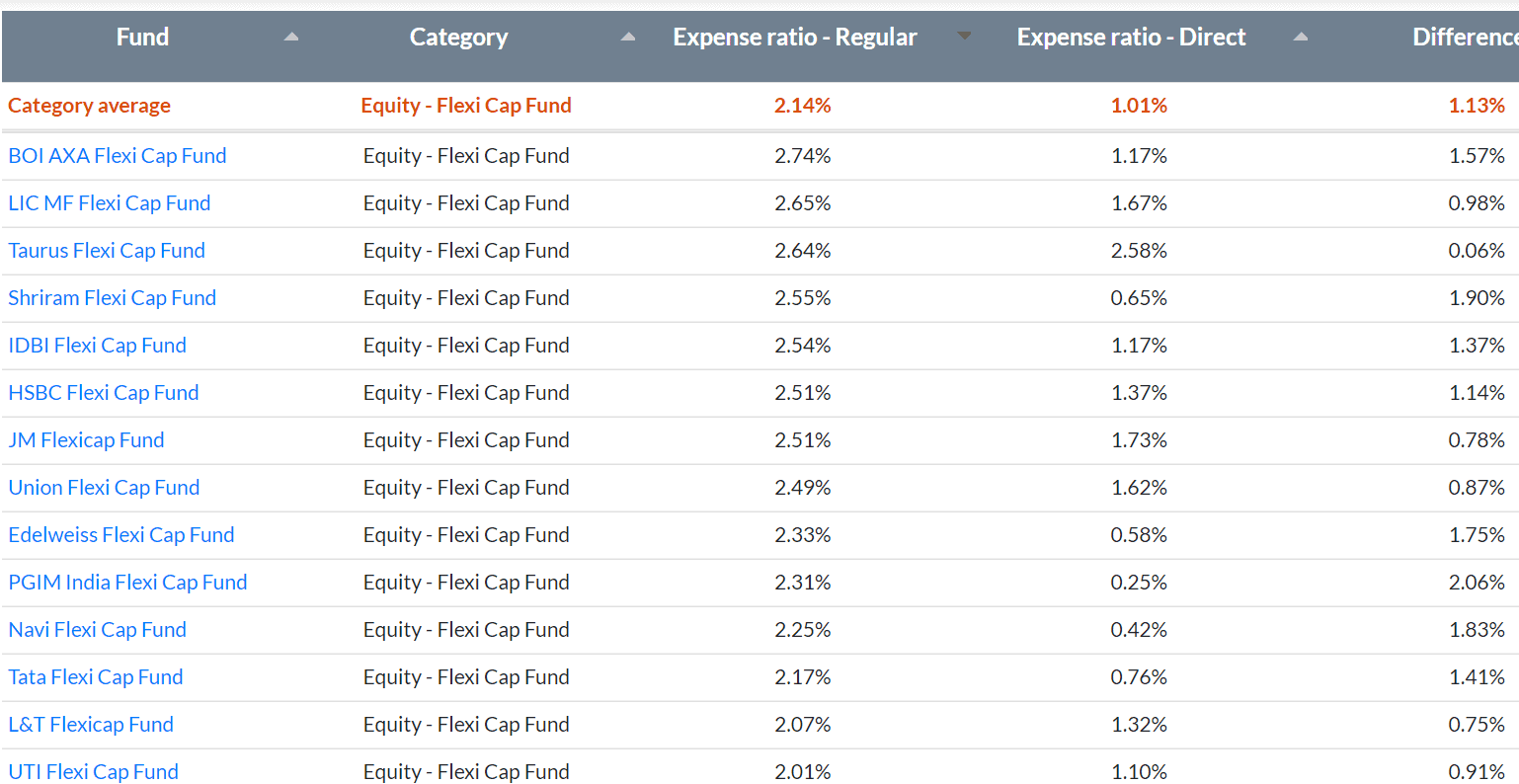

In the image below, (you can check our tool – Mutual fund expense ratio Direct Vs Regular for more data) Edelweiss Flexi Cap’s regular plan has a marginally higher expense ratio than the category average while UTI Flexicap costs a bit lower than the category’s average.

You can make a similar comparison of the direct plan with its own category. In the same example, you will see that Edelweiss Flexicap’s cost is lower than UTI Flexicap under the Direct plan. But let’s not conclude that Edelweiss is a better alternative to the UTI fund because it’s lower on expenses, without knowing the performance. In other words, how a fund’s expense ratio compares against peers is just one among the metrics to look at. It is not the deciding factor. You can have both a low-expense fund with poor performance and a high-expense fund with high performance. What you need to see is whether your fund’s costs are high in relation to its peers and whether returns are compensating for the costs.

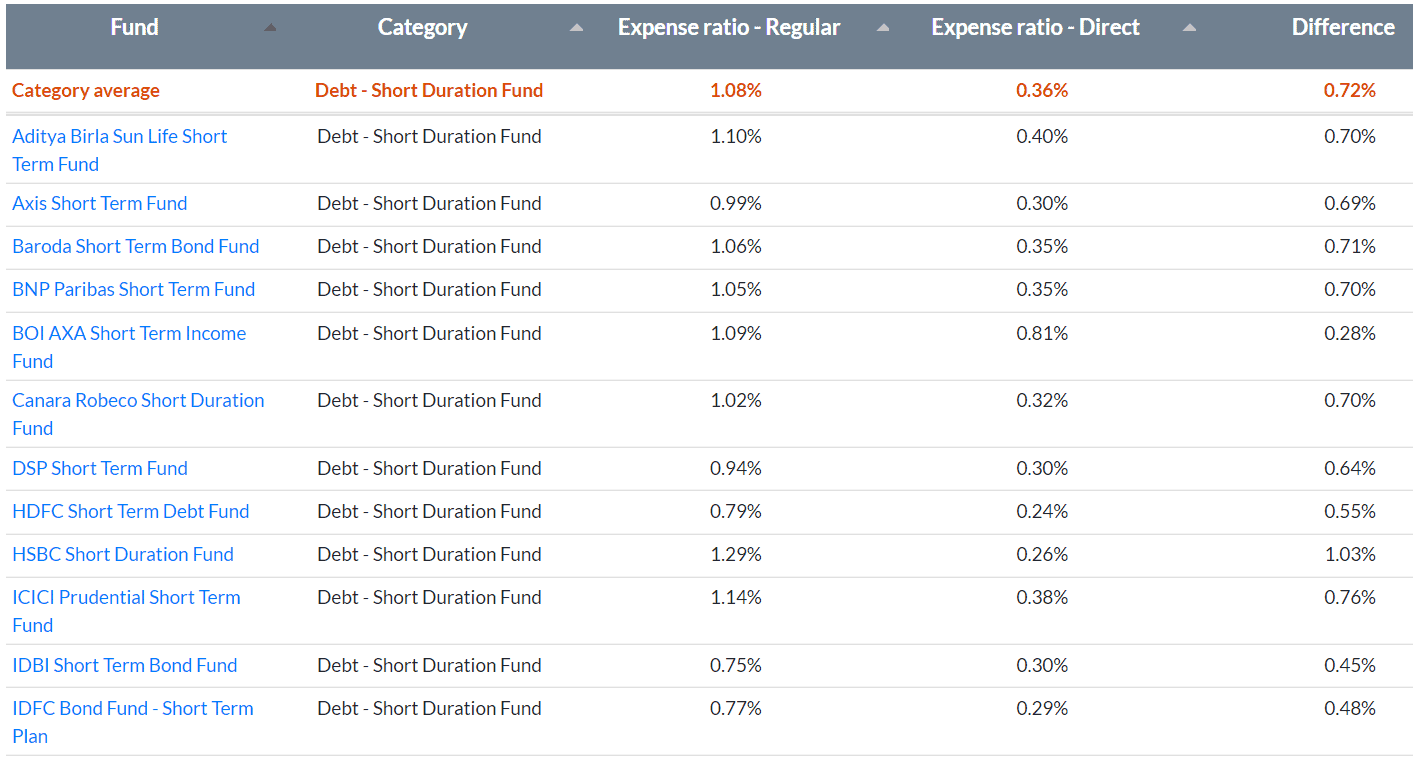

Expense ratio will play an important role in debt funds where cost can significantly eat into your net returns. For example, in the image below for short duration funds, HSBC Short Duration regular plan will find it challenging to ever beat IDFC Bond Fund Short Term with its 50 basis point higher cost – unless the fund takes significantly higher risks. Hence, debt funds are a lot more ‘cost sensitive’ than equity funds.

#2 Difference between direct and regular

If you hold a regular plan and see that its expense ratio is within category limits and it’s a good performer, that’s step 1 done and you may stop with it. But if you are seriously contemplating whether to switch to direct or just curious to know how much more you pay to be in a regular plan, then our tool will give you the simple difference between the direct and regular plan expense ratios. In the first example above, you know that UTI Flexicap’s regular plan is 0.91 percentage points more than its direct plan. Yes, it is not low per se but how does it compare with its peers? Is the scheme reasonable in the extra cost it charges for the regular plan?

This is where comparing the difference for the category makes sense. In this case, for the category on an average, the difference between the direct and regular plan works to 1.13%. UTI Flexicap’s figure is thus lower than the category. So, you know that your fund’s additional expense is at least within the trend in the category!

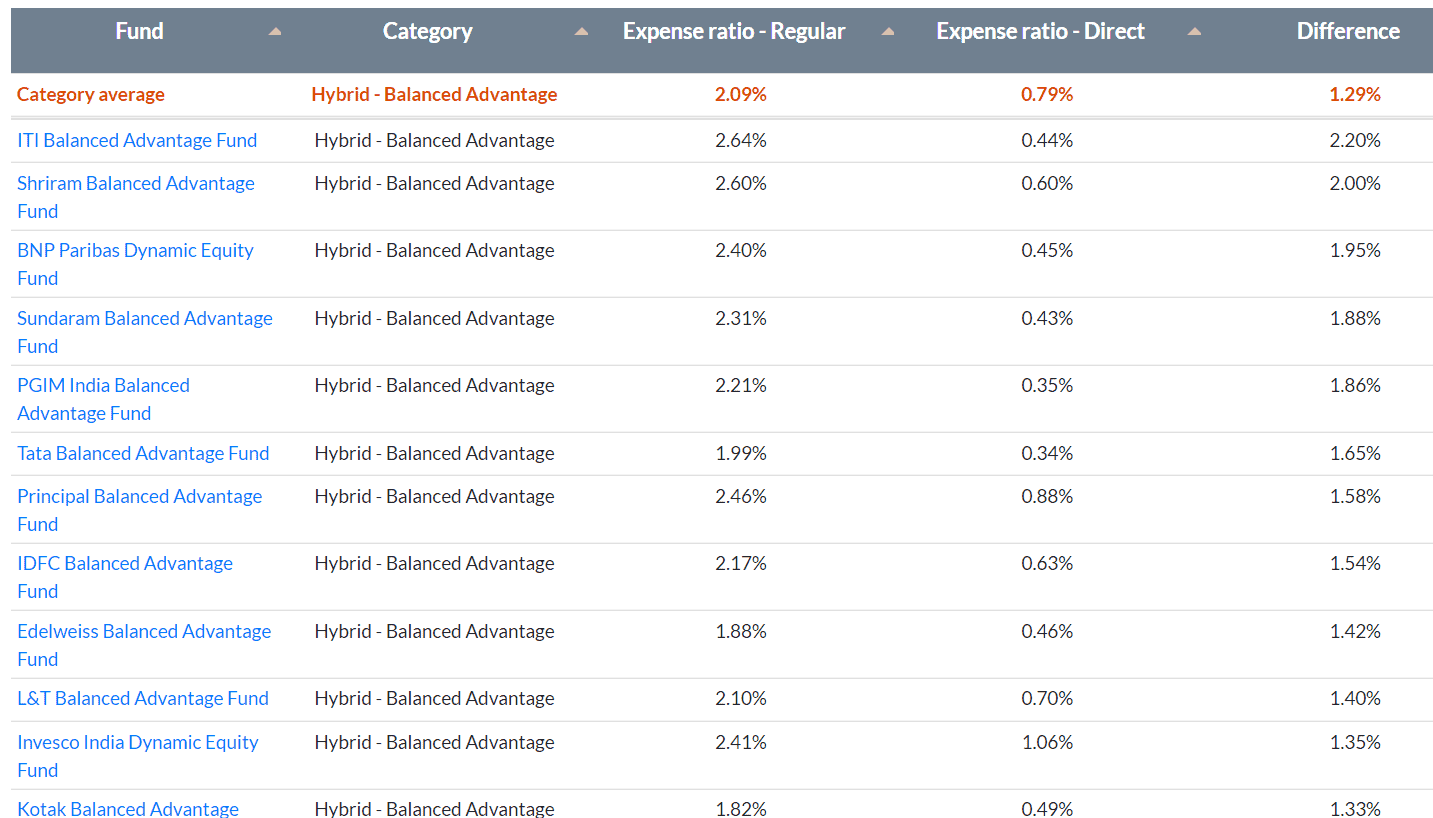

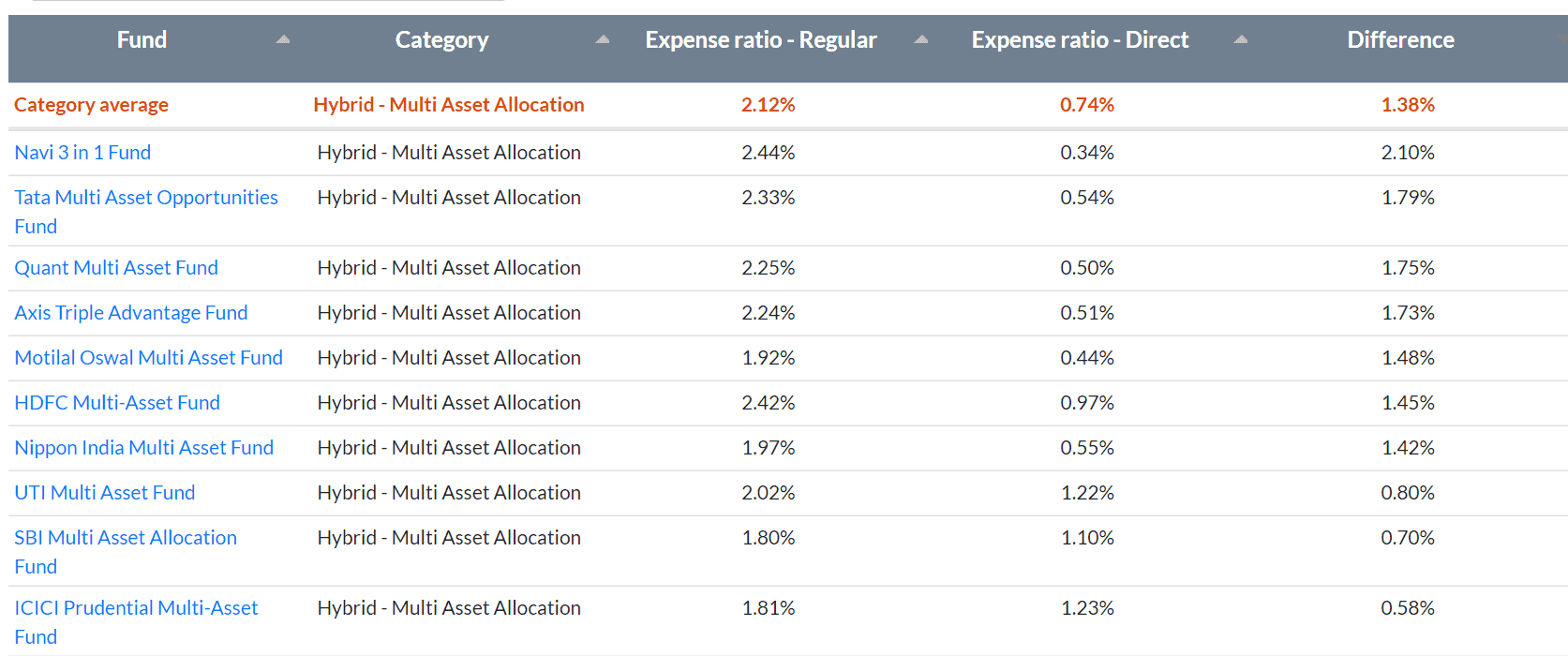

But if you take hybrid balanced advantage funds (image below), you will see that even top performing funds such as Edelweiss Balanced Advantage have a difference (between regular and direct) as high as 1.42% – that is higher than the category’s differential. What does this tell you? That these are likely distribution-driven products – where commission plays a large role in gaining AUM traction.

#3 Categories that are expensive in regular

With the above, you will know the difference between direct and regular cost. You will also know whether a fund is within its category average in the extra cost it charges for the regular plan. But then, there can be categories where the difference per se for the entire set itself can be very high.

Let us continue with the example above of the hybrid balanced advantage category. The image will tell you that 8 funds have a difference of over 1.5 percentage points over their direct plan. That is a significant difference for a category where returns are lower than regular equity (since they hold derivatives and debt that cap returns). Clearly, in categories such as this, if you have the right approach or guidance to choosing funds, direct plans make more sense. This is the case with multi asset allocation funds too!

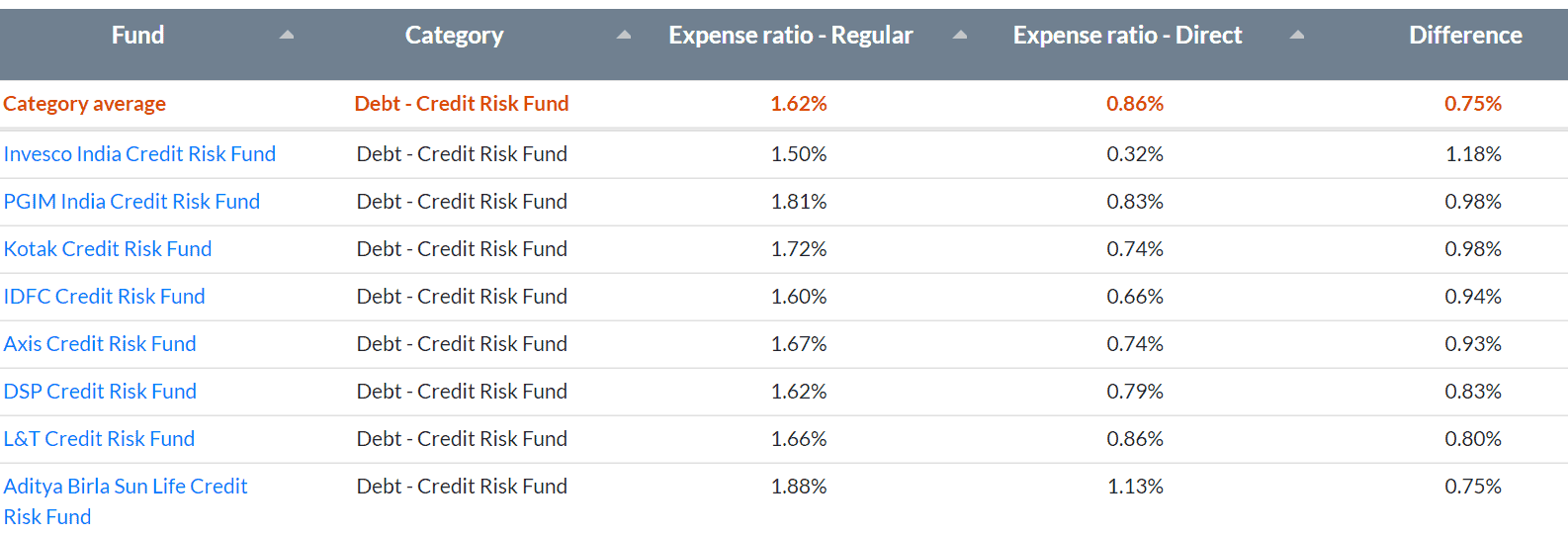

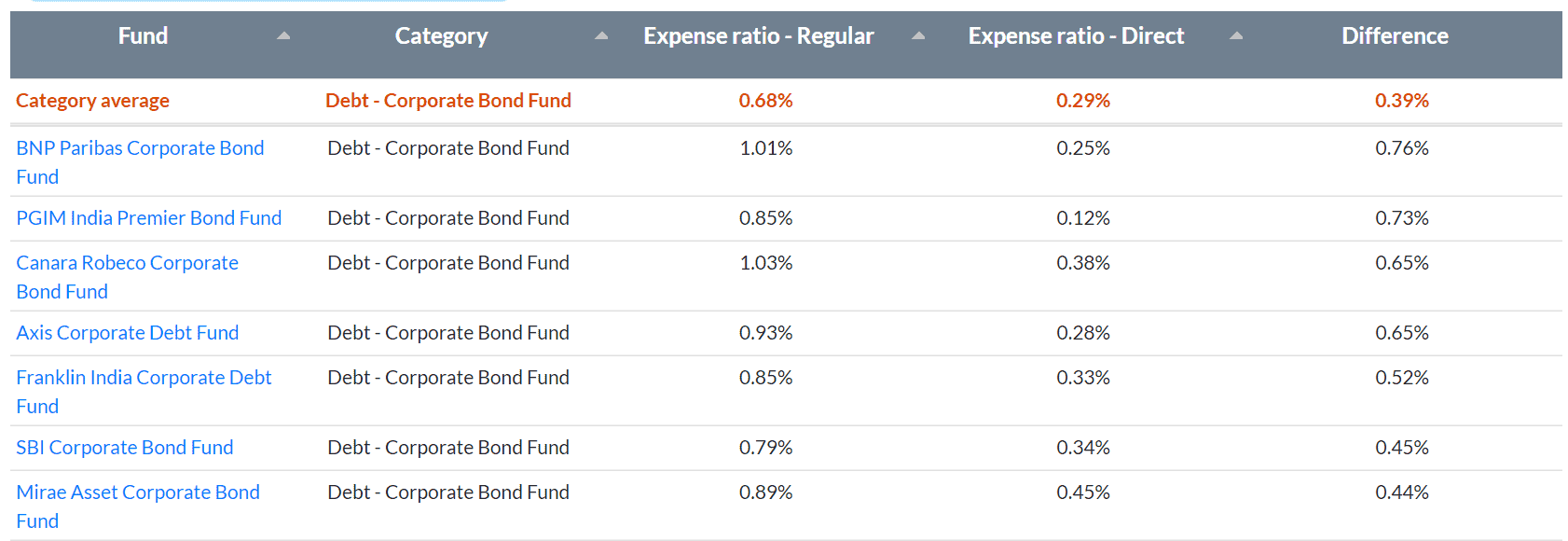

In categories such as debt, the difference between direct and regular can be very stark when some categories are hard to sell and need a push. In such cases, the distribution commission can be quite high. Look at the credit risk category given below. Notice that the expense ratio of regular plans of the credit risk category is more than twice the average of the corporate bond category. What’s more, the difference between regular and direct is just 0.39% on an average in the case of corporate bond funds as opposed to 0.75% for the credit risk category.

In the debt space, a marginally high cost can eat into your returns since your returns are typically in the single digits, unlike equity.

Many hybrid categories, thematic and international fund categories also showcase high expense ratios and high differences between regular and direct.

What you need to keep in mind with expense ratios

In fund expense ratios, there are different factors to consider when concluding whether a fund is too expensive or not. Keep the following points in mind:

- A category with a higher component of active management can have a higher expense ratio, in general, than those with relatively less active management. For example, multi asset category or sector funds have higher expense ratios than say Equity Flexicap or Multicap. A credit risk fund involves a lot more active debt management and due diligence than a corporate bond fund. Hence, its expense per se is higher than the later, whether you’re looking at direct or regular. Of course, whether the credit risk delivers for the risk and cost is a separate matter.

- When the differential between regular and direct is higher than the category average, it means your fund is paying more towards distribution and commission than other funds. Whether you see value in such a higher cost is a call you would need to take. At PrimeInvestor, where a fund is performing well but its additional cost of regular plan is far higher than the category’s average, we specifically give a call of ‘Buy through direct’ in our MF review tool. In such cases, it is a clear red flag that the regular plan cost is very high and can be avoided.

- Higher-than-category difference expense ratios can also occur for 2 other reasons: one, a fund that has a small AUM is allowed to charge at a higher slab as per SEBI’s regulation. This occurs when the fund house is also new. Hence, to promote the funds and make use of the higher cap allowed, many new AMCs with small AUMs will have higher differential in expense ratios. Given below is an example of Quant AMC and how some of their funds garnered AUM on the back of performance as well as high distribution & commission spends. Two, the fund house may be large and established and still have a higher regular expense ratio to promote/push certain schemes to be marketed more. This can be seen in categories such as multi asset allocation with lower AUM as also other hybrid categories, besides thematic funds, or certain debt funds – depending on the market’s flavour. In these cases, it is your call on whether you find the performance of the fund enough to take the higher cost in stride.

Your takeaways

- In general, you need to worry less about a high expense ratio in a scenario where the fund and the market are both delivering. That also means that expense ratio is less important in potentially double-digit earning categories such as equity and becomes more important in relatively lower returning classes such as debt, equity savings or balanced advantage. No doubt both make an impact on your returns with compounding.

- That said, where a fund’s expense ratio is unusually high in the regular plan, then it calls for a decision. If you are a user of a platform such as PrimeInvestor there is little reason for you to go for a regular plan, especially in funds where we have issued an ‘invest through direct’ call.

- Some categories that are high maintenance (multiple asset classes or high due diligence on credit risk etc.) can have higher costs. Therefore, the larger call for you to take would be whether you need to own funds from such categories at all.

- Expense ratio should not be seen as a standalone metric. Performance, portfolio quality and fitment of strategy in your portfolio should take precedence. Higher cost will in any case eventually show up in performance. You might see a few funds we recommend having a higher expense ratio than peers. That will likely be due to the nature of category. And remember, we recommend the direct plan.

- When the difference between regular and direct is high and you decide to switch to direct, take into consideration your own tax situation and cash outgo. This is entirely individual to you. It is not possible for us to give a ‘strategy’ for this.

- New fund offers, funds heavily promoted by AMCs or distributors, or banks need to be viewed from a cost (expense ratio) angle, beyond its fancied appeal.

P.S: Some of you have already asked us for a calculator on the difference in your corpus arising from direct plan over regular plan. We plan to build a tool where you can input your return assumptions. The current tool would get too crowded and confusing if we introduced multiple data with assumptions in it. We mean it as a simple expense ratio comparison tool. We will sound you off once the calculator is ready!