As we head into the new year, equity markets couldn’t be on a stronger note. Markets appear to have pushed past the concerns, taking cues from interest rate direction, global and domestic growth & demand, stable government and more.

So are markets on firm footing to shoot high in 2024 as well?

As we see the equity outlook 2024 will be a year of frontloaded returns. A healthy correction could be underway in the second half, led by one or more of the following broad factors:

- Expectations vs reality on economic growth and interest rates, both globally and at home

- Slowing Govt. capex in Budget 2024 (July) to achieve fiscal deficit targets, and the impact on capex-centric and manufacturing companies

- Valuation excesses and euphoria in many pockets, including PSUs with narratives scoring over numbers

In our view, 2024 will be a year to play it safe, avoid excessive risks of relying on narratives in sectors or stocks, and be more realistic in terms of further upside from here. Here’s a detailed explanation of how we see equity markets behaving over the course of 2024.

A rewind of 2023

A look back on what shaped markets in 2023 will help set the equity outlook 2024. The year 2023 didn’t start with optimism against the backdrop of US rate hikes, concerns around a US recession and continued selling by FIIs.

The first trigger came after the Silicon Valley Bank crisis in the US in March 2023, which set expectations of a pause in rate hikes by the US Fed. Markets turned south as the US Fed remained hawkish and US 10-year yields hit 5%.

That panic marked bottom for both equities and bonds. Equity and debt markets made a stellar comeback in the last two months of 2023 as the Fed struck a U-turn on rates in its December policy meeting. Meanwhile, forecasts of a US recession didn’t come true as the economy showed significant resilience.

Our markets couldn’t help but dance to the tunes of US outcomes and aggressive FII selling. But we also saw the rise of Indian investor who absorbed the entire FII selling, including the large blocks of selling by Private Equity majors. This large domestic flow also helped our market to sustain valuations at the upper end of the PE band despite adverse global circumstances for a large part of 2023.

In our equity outlook 2023, and over the course of last year as well, we had advised you to look outside of Index, as we expected index returns to be capped. We placed an emphasis on auto and ancillaries, pharmaceutical API, cement, consumer durables and textiles. This bore true as the year played out.

Let’s take a quick glance through the outperformers and underperformers of 2023 to set the context for 2024.

Heavyweights disappoint

The biggest underperformer of 2023 was the heavyweight banking sector with a nearly 10% underperformance compared to the Nifty. After a stellar rally in 2022, banking heavyweights paused in 2023 as deposit rates weighed on their margins; the HDFC group merger, too, weighed. IT services managed to match Nifty returns but couldn’t do further lifting of the Nifty as large caps lagged mid-sized players in performance. IT has started 2024 on a highly positive note, though, calling an end to the pessimistic outlook.

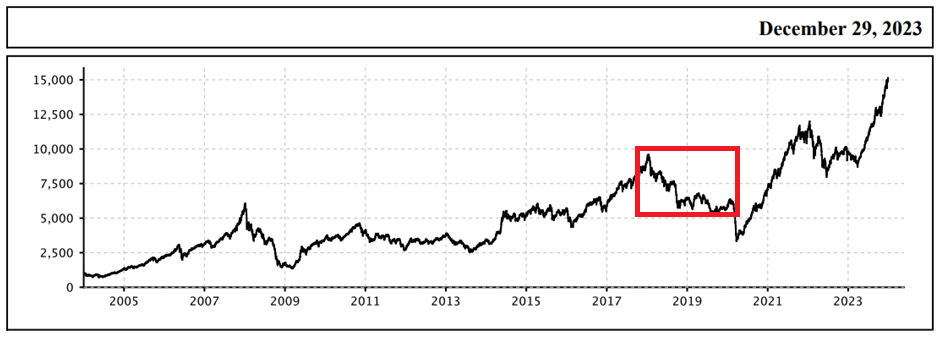

Smallcaps play catch-up

The smallcap segment significantly underperformed the Nifty, with -40% returns between 2018-2020 (pre-Covid) when the Nifty delivered just about positive returns. At the beginning of 2023, the Nifty Smallcap 100 was at the same level as it was in 2018. The index has since significantly caught up in 2023, delivering 50% returns over the pre-Covid peak.

This was also one of the opportunities we had highlighted in our 2023 outlook, and we had specifically issued a smallcap fund recommendation just before the smallcap rally really took off. There may be a little more of catch up remaining in the early part of 2024. Here’s a quick look into the chart of Nifty Small cap 100 Index.

Source: NSE India, Nifty Small cap 100 fact sheet

Realty steals the show

This sector was on the back foot for nearly a decade and a half – ever since the global financial crisis. But 2023 marked a phenomenal comeback for the sector due to robust demand. This sector’s recovery also has significant spill-over effect on demand for cement, housing finance, home improvement, and so on, as it is one of the key components of the capex in the economy. The upbeat sentiment in the sector is reminiscent of the 2007 heydays; the top index constituent, DLF, is back past its IPO price after 14 years.

Capital goods and PSUs surprise

Capital goods is another sector that surprised on earnings, as their exports also fired led by clean energy transition globally (US Inflation reduction act, Europe energy investments). Companies engaged in turbines, compressors, transformers, drilling & mining equipment, and consumables stole the show with stellar earnings performance. We had called out during our 2023 outlook that the story may gather momentum during the year, including exports.

PSUs, on the other hand, had 3 factors driving stock price – ignored valuations, global capacity constraints in sectors like defence, and upbeat sentiment supported by Govt. capex. Sentiment is the biggest factor among all playing out now and so this sector may prove to be deceptive for investors trying to catch late.

What lies ahead in 2024?

With this background, let’s get into what could play out over 2024. We have broken this down on the following lines:

- Broad market perspective

- Nifty valuations and market levels

Broader market perspective

With markets breaking out globally (US, Europe, Japan, India, Brazil) and sentiment upbeat, there is no reason to go on the back foot immediately. A better phrase to say about equities now is “there is a bull market everywhere!” (ex-China).

The pitch looks clean and good ahead of two main factors, both slated towards the middle of the calendar year.

- The first rate cut from the US Fed. A US soft-landing combined with rate cuts playing out as expected is the most desirable outcome for every asset class that the dollar is flowing into. It appears that all asset classes are currently priced for this outcome.

- Our own general elections, with expectations of continued stability of the current government. Expectations of continued pause on rates or a rate cut by the RBI are also being priced in.

However, expectations will have to play out as per template for markets to hold gains and end on a positive note in 2024. Even minor disappointments can lead to meaningful corrections.

For us, the implication of US economy macros is mainly on sentiment and flows, be it FII or FDI. India’s inclusion in MSCI bond index and potentially higher equity allocations in the Emerging Market (EM) basket, could lend some sort of balancing act.

More important for us would be Budget 2024 post general elections (in July) that may serve as a test for capex-dependent sectors as to what extent Govt. can continue the heavy lifting (after 2 consecutive years of 30% and a 35% growth in allocation) without deviating from the planned fiscal consolidation path. An adverse outcome on this front in Budget could disappoint markets unless private sector capex rises to the occasion to compensate.

At this time, therefore, all we can say is that markets are setting up for a good first half until the time expectations need to materialise. Based on how reality pans out, on global and domestic macros at that point, and market valuations, we may see markets react by staying on course or correcting.

Valuation perspective

By now, the Nifty has completed ~80% rally (16% CAGR) from the pre-Covid level. This is well-justified by a 100% growth in earnings (doubling of EPS) and there is valuation comfort of a contracting PE multiple (~25 times pre-Covid to 22 times now). This happened at a time when the economy itself took 2 years to recover back to its pre-Covid GDP levels.

See the graph below, on the Nifty EPS. The take off in earnings has come after 7 years of stagnancy. This has come by in the aftermath of Covid, especially the wild jump in FY22, and the continuity of growth from there.

There is one key point to note here – the bulk of the EPS growth is contributed by cyclicals that were putting a poor show until FY20 and then emerged as outliers post Covid. Cyclicals with 24.5% combined weight grew their PAT ~4X in 4 years, at >40% CAGR. Here’s a quick glimpse into the outliers, category wise, with their combined weight in Nifty 50:

Why is this important? The higher contribution of earnings from cyclicals limits room for further expansion in PE multiples. Therefore, current valuations at 22 times FY24 earnings and 19 times FY25 estimated earnings are quite fair in our view.

We expect the market to hover around 18 to 20 times FY25 estimated earnings on the lower and upper bands, respectively, as highlighted in table below.

An outcome other than soft landing in US may lead to lower than the 15% expected earnings growth. The lower band may be breached by 5-10% as global cyclicals may take a hit on their earnings.

To summarize the broad market and valuation perspectives:

- The current equity market sentiment is positive, in light of expectations on US interest rates and domestic political outcome.

- With this, the year could turn out to be one where returns are frontloaded in the first half and see an uncertain second half.

- The second half could be shaped up by how the US economy fares, how rate cuts both in the US and at home pan out, and what’s in store in our Budget 2024.

Also, its beyond our guess if anything unexpected could crop up in 2024; like the Russia- Ukraine Crisis in early 2022 and the Silicon Valley Bank crisis in early 2023 gave a bit of a hard knock to markets.

Themes to play and avoid in 2024

2024 will be a year to pay it safe and not take excessive risks. Here is where we see opportunities in 2024 and highlight what to steer clear of.

#1 Take shelter in large caps

Banking sector valuations are attractive considering their growth tailwinds and the sedate 2023 returns as we noted above. The IT sector has started 2024 on a positive note. Riding safe can work in favour of investors considering the stretched valuations down the order in most other pockets. Large caps in financial, IT services, pharmaceuticals, and consumption could provide valuation comfort combined with decent growth.

The texture of the market for 2024 looks like one can take shelter in large cap pockets and still make decent returns.

#2 Play the capex theme indirectly

One can therefore play the private capex recovery through financials, especially corporate lenders, which are trading at reasonable valuations at this point of time. Corporate banks in large and mid-sized space are doing well while tight liquidity conditions are giving them a better yield on the corporate book. Lower yield was hurting them in past and was forcing banks to chase retail lending; better yields on corporate book can therefore be highly rewarding.

Private sector capex in sectors like manufacturing will be largely funded by borrowings than FDI as these companies can take debt based on their earnings and prevents dilution for promoters. Besides, they borrow to fund their working capital requirements as well.

Outside of banks, to play the capex theme directly, it would be safer to stick to those with significant and proven execution capabilities.

If manufacturing were to grow at a far higher pace than the overall economic growth rate, then corporate lenders could emerge as a proxy growth play for investors.

#3 If you are ready to over-pay for stocks, pay for this cohort.

With all growth pockets seeing skyrocketing valuations, consumption as a pocket looks better from the point of view of balance sheet, return ratios and cash flows. Consumption is also one pocket with significant long-term growth tailwinds in a growing economy of large size like India.

These are businesses with secular growth prospects, healthy balance sheet and superior RoCE profile and look a far better place than cyclicals at this point of time. Large-cap consumer stocks, while doling out a temporary hit owing to higher valuation at entry, are still unlikely to take you for a ride on account of balance sheet or profitability issues which cyclicals are wont to do.

Here’s a quick comparison of the Nifty consumption Index against the defence and capital goods indices.

The consumption theme offers a wide variety of segments to look for opportunities as it covers broader categories such as retail, automobiles, consumer durables, FMCG, food & beverages, and so on. It also includes real estate proxies such as housing finance, home improvement, etc as well.

The larger focus here is lower cyclicality of earnings, clean balance sheet and superior RoCE profile while participating in long term growth opportunity. The large-cap basket may be especially worth a look.

#4 Look for evidence in narrative led themes like China + 1, manufacturing

While there is much hope on manufacturing, this theme can be highly deceptive if you overlook the key traits that lead to shareholder value creation, return on capital (RoCE). Already, narrative-led themes like chemicals have deceived investors in the recent past.

So even as there is excitement around the manufacturing sector, it makes sense to look at already successful companies and the traits made them succeed in creating value for investors. This has come from sectors like automobiles and pharmaceuticals in the past. Electronics is the new hope.

For example, in automobiles, consider Bajaj Auto. It has not only utilised the manufacturing economics of India (being a large domestic market), it also developed global markets (presence in 75 countries) and built successful brands - a success story that mirror Japanese auto majors. Each of these factors made up for exceptionally strong competitive advantage, reflecting in its FMCG-like RoCE.

It is important to take such outstanding enterprises as benchmarks in identifying the drivers of RoCE. Another example would be Eicher Motors and to some extent, TVS Motors. Similarly, in the emerging sectors, Dixon has proved to be an outlier that scores on scale, design (R&D) and customer acquisition (high profile large size global players).

Brands, design, manufacturing scale, R&D capabilities, and ability to develop markets are some of the key factors that can make a manufacturing company stand out and earn superior RoCE and in turn create value for investors. Simply “manufacturing” may not lead to superior outcomes.

#5 Be wary of order book stories, look for execution track record and balance sheet strength

Infrastructure is another hot theme in markets currently. If we look at this sector over last 20 years, L&T is the only company that has created long term value to shareholders. You will seldom find any other large cap or mid-cap in this space barring GMR and the Adanis.

For L&T, a big chunk of its current value is represented by its IT services subsidiaries as well. There have been few long-term survivors like KNR Construction and Ahluwalia Construction, but these are still small caps.

The sector has always been in the limelight in every cycle at the time of order accretion - but few players have successfully navigated the execution and payment cycles without landing into arbitrations. During the order accretion cycle, market prices the stock to perfection based on a certain execution timeline and certain profitability assumption that goes for a toss during other two cycles.

This time, such aggressive assumptions seem to have built in PSU defence players as well, where the order delivery is scheduled over 5-7 years while market has taken their valuations far beyond what these businesses may usually fetch.

#6 Stay clear of turnarounds and penny stocks

There is huge fanfare for yesteryear stories in spaces like infrastructure, energy, resources, railways, and so on at this point. There is a saying that “turnarounds rarely turnaround”, but companies that are still leaders in their respective industry with critical product or engineering capabilities could be candidates for it.

But it is extremely important to check whether the turnarounds have evidence in numbers in terms of debt reduction, better capacity utilisation, margin expansion, business expansion and improving operating cash flows.

Turnaround should be clearly visible in operating cash flows and debt reduction. Otherwise stay clear of such stories. You may use our “debt reduction” and “steady cash flow” Prime Stock Screeners to filter out stocks based on these parameters.

What to do with your equity exposure?

For direct stock investors - stick to key index sectors and stocks in 2024 while hunting for select opportunities outside of index as discussed above to generate extra returns. Focus on the large-cap segment as well. At PrimeInvestor, we will look for stocks along the lines explained above.

For equity mutual fund investors – take this opportunity to check if your portfolio needs rebalancing to trim equity excesses especially in the mid-and-smallcap segments. Continue with SIP (or regular investments) in your equity funds and do not stop or postpone these. The latter half of the year may throw up opportunities to buy on dips, so you can consider maintaining some surplus for investments then. As we did last year, we may also play sector/thematic opportunities through funds. Do look out for these calls (which will also be housed under Prime Funds) which you can use to play specific opportunities if you wish to.

7 thoughts on “Prime Equity Outlook 2024”

Do you think that following still holds true or earnings of other companies are also changed? Is Nifty reasonably priced now? Do you want to see earning reports of July to get more details?

“The higher contribution of earnings from cyclicals limits room for further expansion in PE multiples. Therefore, current valuations at 22 times FY24 earnings and 19 times FY25 estimated earnings are quite fair in our view. “

Welcome your query sir,

And this is perhaps the right question at the right time

As you are aware, we explained about extent of earnings contribution that came from banks, metals, industrials, etc in the report itself to comment on what multiple is fair.

Interestingly, FY24 was the first year after a long time (excl. Covid years due to volatility) where a double earnings growth for Nifty 50 played out either on expected lines or a tad better than that. Otherwise, every year prior to that, there was a downward revision.

If we consider the current earnings growth momentum to continue in FY25 (15-16% growth), then Nifty 50 is trading at 20-21 times FY25 earnings (we are now entering Q1 of FY25).

At this point of time, a 1 PE multiple is equal to 1,000 – 1,150 points in Nifty (as Nifty EPS is 1,000 for FY24, expected at 1,150-1,160 for FY25)

So, if you assume same 22 PE would sustain for FY25, then it would come close to 25,000-25,300

(mathematically, no prediction/target, trying to arrive at fair assumption)

Hope Telecom, metals, cement and power would support Nifty to carry this earnings momentum (15-16%) in FY25 on the back of very high earnings (profit) momentum that we are seeing in those sectors. Again cyclicals doing the job and so PE multiple expansion is not desirable unless the earnings can grow far higher beyond this 15-16%

In short, from fair pricing, Nifty is moving fast and borrowing “some” returns from future as well.

A consolidation or correction would be healthy to remove excesses (largely in specific sectors) and lay a healthy foundation for future growth and returns. We can’t call it when as it needs a trigger.

Right now, markets are bullish globally and banking on “inevitable” rate cuts (that’s what equity markets are assuming).

A healthy correction should happen form some kind of “dis-appointment” for the market – either on interest rates or Govt. policy shifts or worsening geo-political issues or some unanticipated causes.

Hope this clarifies

Thank you

Extremely well written. Well done….I wish everyone good luck in one’s investing journey in 2024

Thank You . A detailed but easy to read article which has info and action points. Kindly share Your views on Geo Political / War Risk. Unlike the period till 2020/21, the threat of war is increasing. How a retail investor, who is mid way towards building retirement corpus, protect his corpus. Will 50:50 Equity – Fixed Income combo will help ? Balaji, Bangalore

Let us try to simplify this. We think it is best not to derail financial goals for such risks. There are only 2 scenarios – one there are such wars that will cause market to crash and eventually factor it in. In which case, you should be using such opportunities to buy. Two, the war kills economies. In which case no asset allocation will help much so there is no point planning for the same 🙂 Vidya

Nicely written article and informative for 2024 equity outlook.

Most Awaited Update, Thanks for the Article.

Pranams to all the efforts from all behind it 💐

Comments are closed.