Last month, we analysed the cement industry in detail. In the analysis, we’d noted a few points – one, that there has been consolidation in the space, two, that companies had been deleveraging, and three, that margins have been under threat owing to pricier energy and inputs.

These three points now come into the limelight. Ever since news broke a month ago that the Holcim group was putting its cement businesses in India on the block, it has been closely watched. And last week, the Adani group signed a deal to take over Holcim India’s cement business. Holcim’s India arms are Ambuja Cements and ACC Limited.

Together, these two companies account for about 12% of industry capacity. That’s next only to leader UltraTech Cement. So, this deal between Adani and Holcim is bound to not only impact the players involved but also the entire industry.

It was no surprise then that, on the day the deal was announced, shares of UltraTech and Shree Cement closed at between 2.5% and 3% lower while that of ACC and Ambuja Cements soared.

While it will take a good while for the acquisition to go through, it is worth noting how this deal could shake things up in the cement industry. With the demand outlook for the cement industry improving, understanding what to watch for would be crucial.

The Deal

The Adani Group, through an off-shore SPV (Endeavour Trade and Investment, based in Mauritius), has acquired Holcim’s stake in Ambuja Cements and ACC at a share price of Rs. 385 for Ambuja Cements and Rs. 2,300 for ACC. The Adani family also has to make the mandatory open offer for 26% of the shares of Ambuja Cements and ACC from non-promoter shareholders since the deal will result in a change in ownership. The entire deal including the open offer has been valued at USD 10.5 billion (~Rs. 81,000 crores) and this, in addition to equity from the Adani family, is reported to be funded by several foreign banks.

The transaction is expected to be concluded in the second half of the year and is still subject to approvals and the execution of the open offer (its impact on total non-public shareholding has to be watched). But we’re not getting into the structure of the deal itself. What we’re focusing on is the impact on the industry, ACC and Ambuja Cements.

Gautam Adani, a first-generation entrepreneur who needs no introduction, had his sights set on the cement space for some time now. With this acquisition deal with Holcim, the group has managed to leapfrog to the #2 spot in an industry where setting up capacities takes a few years at least. The table below shows the capacities of Ambuja Cements and ACC.

There are two parts to analysing the impact of the Adani group’s deal with Holcim India – one, the impact on the industry itself, given the combined size of Ambuja Cement and ACC. Two, what it means for the two companies involved as their ownership sees a marked change.

Impact on the cement industry

Like we said in our report ‘Cement Industry: 5 things to know before you choose a stock’, the industry is already a fairly consolidated one in terms of capacities and is dominated by a few large players. Ambuja Cement and ACC together account for 67.45 MTPA. While leader UltraTech is head and shoulders above 120 MTPA, the Adani group chairman has already expressed his intention to double capacity to 140 MTPA in the next five years.

Ambitious as this may seem, one cannot rule out the group taking the inorganic route to get there. This is a marked change from the more cautious approach that the Holcim group took for ACC and Ambuja until now.

In 2016, the combined capacity of Ambuja Cement and ACC stood at 63 MTPA. This has not changed much and currently stands at only 67.45 MTPA. UltraTech on the other hand whose capacity in FY 2015-16 stood at 63 MTPA, today is at nearly double that with 120 MTPA on the back of sustained organic and inorganic expansion (even taking over debt-ridden smaller players).

With an aggressive second-rung player, the cement industry could see two main trends:

- Amplified consolidation and pace of acquisitions as the Adani group ramps up capacities and UltraTech strengthens its position. This could result in the industry being dominated by 2 large players with the rest following by a margin. To put it in perspective, Shree Cements is the next highest in order of capacity, but with a far lower ~45MTPA to its name.

- More intense competition as the new owners work to wrestle market share away from the other players. Being an industry that operates in terms of smaller regional markets, UltraTech and Ambuja + ACC combined are the only ones with a meaningful pan-India presence. Intensification of competition could pressure price and can be hard on smaller players – circling back to likely acquisitions.

Impact on Ambuja Cement and ACC

If the cement industry looks set to see some action over time in terms of consolidation, for the two companies in the acquisition, it could mean a big pivot away from the way they have been run, up until now. Here’s what could happen.

#1 A possible merger?

Ambuja Cements and ACC have been part of the same group for a while now and the idea of merging the two is hardly new. While there have been obstacles to the merger in the past (including unfavourable regulations surrounding limestone mines), with the latest development, the case is strong for the Adani Group to push forward with the merger.

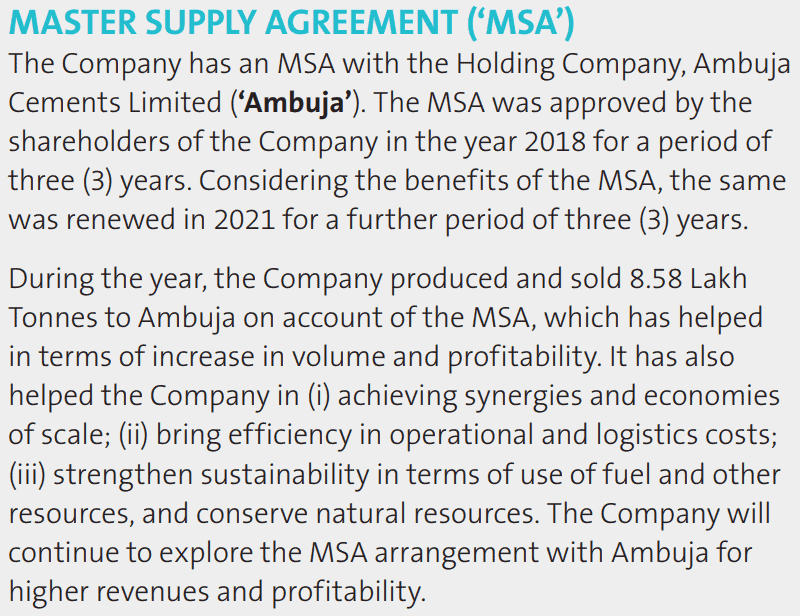

Recognising the synergies and cost rationalisations that could be unlocked, the two companies already have a master supply agreement in place to integrate some of their operations which has helped in controlling costs (especially logistics) for both companies in recent times.

Source: ACC Limited Annual Report - December 2021

#2 Good for revenue and margins

A press release on the acquisition states that “Both Ambuja and ACC will benefit from synergies with the integrated Adani infrastructure platform, especially in the areas of raw material, renewable power and logistics, where Adani Portfolio companies have vast experience and deep expertise. This will enable higher margins and return on capital employed for the two companies,”. Here are the ways this could happen:

- Adani Enterprises’ Mine Developer and Operator (MDO) business is one of the largest developers and operators of coal mines in India. In addition, it also has coal mines in Indonesia and Australia (controversial Carmichel mine) through its subsidiaries. Adani Enterprises is also the largest player in the Integrated Resource Management business where they manage the entire procurement process (domestic and import) of resources. While this business began with just coal management (AEL is the largest coal supplier in India and the largest importer of coal from Indonesia), they have now diversified to cement, steel etc. In an environment where rising fuel costs (especially coal, pet coke and diesel) have pressured margins of cement makers, the Adani group’s position of strength via its MDO and IRM businesses could give Ambuja Cements and ACC an edge in preserving margins.

- Fly ash, a key input that will aid in reducing energy costs could be procured from the group’s power plants.

- Ambuja Cement and ACC pay an annual fee for technology support to Holcim Technology Limited. In 2021 this amounted to Rs. 131.25 crores and Rs. 154.51 crores for Ambuja Cements and ACC respectively. At ~1% of net sales, this could help in protecting margins.

- The Adani group expects to be one of the largest customers of its own cement business via their infrastructure businesses and this could help topline by providing captive business.

#3 Zero-low debt but for how much longer?

Both Ambuja Cements and ACC have prioritized being net-debt zero (though this may have come at the cost of meagre capacity expansion). With the mood set to change to one of aggressive expansion, the companies may take on debt to fund growth. In an industry where balance sheet health is prized with many smaller players falling prey to bankruptcy, Ambuja Cements and ACC could lose the edge that they now have over the others by being net debt-free currently.

Being vigilant with debt has meant that the companies have been able to save on interest costs and have built up enviable cash positions. The cash and equivalents (standalone) as on December 2021 stood at over Rs. 10,000 crores for both companies together (Ambuja Cements - Rs. 4,163; ACC - Rs. 7,404). With the new owners shifting gears, the war chest could be used up to fuel expansions.

What’s on the cards for investors?

While the captive business that the Adani group will provide and the cost benefits of being a part of the Adani system are strong positives that will benefit non-promoter shareholders too, the following points need to be carefully considered by investors.

- Less cash for dividends: Both Ambuja Cements and ACC have prioritised handsome dividend payouts (even if a bulk of it went to Holcim). But here again things might change with the focus clearly set on aggressive capacity expansion.

- Change in management & parent support: While Holcim can be accused of being too slow in ramping up capacities and losing market share as a result in India, Ambuja Cements and ACC have enjoyed the benefit of having an MNC parent. As the top cement maker in the world, Holcim would have brought technical expertise and support. Apart from this, generating cash flows, remaining debt free and return on capital have clearly been prioritized for both players.

With a first-generation entrepreneur, who has seen a meteoric rise in the fortunes of his businesses, at the helm, investors may find that the cautious nature of Ambuja Cements and ACC is set to change. Both companies will now be part of the Adani group and any news (good or bad) pertaining to the other group companies will have a bearing on Ambuja & ACC’s stock prices. Some of the businesses are or will be taking on large debts to fuel capex plans. Debt: equity ratio is already high for many group companies - (Adani Enterprises is at 1.87, Adani Green Energy at 20.2, Adani Transmission at 3.02 and Adani Power at 2.61). This deal itself has been funded partly by debt and news like this could weigh on the stocks of Ambuja Cement and ACC.

In a nutshell, the Adani group’s acquisition of ACC and Ambuja Cements is likely to change prospects for both the industry as well as the companies themselves. The trends explained in this impact analysis will evolve only over time - but it is important to keep watch on how this deal progresses (expected to take up to the second half of the year) and how other cement players are responding to the Adani group’s plans for the companies.