This is the third part of a 4-part series where we discuss the five mistakes that lead to big losses in your equity investments and how to avoid them.

The 4-part series is as follows:

- Big losses from rich valuation

- Losses from cyclical businesses

- Losses from low quality businesses ( this article)

- Losses from seeming turnaround stories and no-growth businesses

Big losses from low quality businesses

Low quality businesses get married to you in haste when a bull market rages. And in a down market, you repent at leisure with big losses 🙂

Every stock market boom will be led by a broad-based rally with mid and small cap stocks on fire. This apart, the popular sectors see a rush in IPOs. There will be plenty of companies with poor quality balance sheets or poor businesses that join the party. And a bull market does not bother to separate the wheat from the chaff.

So, retail investors often end up with a large number of stocks of such companies at the end of every bull market. When the rally ends, investors tend to lose as much as 50-90% in most of these stocks with low quality businesses.

As Warren Buffett said: “Only when the tide goes out do you learn who has been swimming naked.“

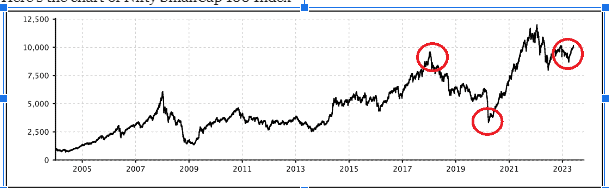

Why big losses are possible in the small-cap segment – low quality businesses of course!

The small cap index, which is on fire now, had slumped 40% post the 2017 bull run and saw a further slump during Covid. It is conquering its pre-Covid high only now, in 2023. In the same period, Nifty climbed over 50%!

Here’s the chart of Nifty SmallCap 100 Index

When the index plunged 40%, the bottom-of-the-quality-curve stocks plunged a lot more leading to significant loss for investors post 2017.

Why are we talking about the small-cap space now? It is because, when you look for multibaggers, it is typically in the small-cap space. Reason being, it is this space that provides opportunities to identify the less discovered stocks that hold potential to be re-rated and to even become an emerging large cap. That move typically generates the manifold gains that we all love to bag!

But let us understand the composition of this segment and why your chances of making money are so low here while your chances of ending with a low quality company that is a loss maker are quite high!

If we go by AMFI classification of stocks in to large, mid, and small caps, the 100th company has a market cap of close to Rs.50,000 crore and the 250th company has market cap of close to Rs.16,500 crore.

Below 250th company are all small caps and these add up to 1,750 stocks in the NSE. The market cap of 500th company is around Rs.5,000 crores and that of 1,000th company is around Rs.1,000 crore. During the small cap rally, the number of companies getting investor attention is so huge that investors will be bombarded with new multi-bagger ideas every day.

Let us take the auto space. For 10 auto companies, there are 100 ancillary companies, majority are small caps, and they make up for a big cohort that typically rally during mid and small cap boom. There are only 10 among them in the mid cap and above category and rest are all small caps. In general, auto ancillaries are fixed assets, labour and working capital heavy companies and so, generate mediocre RoCE. There are very few companies who score better on these parameters due to technology intensive products and in turn deliver better quality of growth (superior RoCE).

The banking and financial sector with 200 stocks is another pack with large number of small cap stocks. Out of the 8 old age private sector banks, only Federal Bank has managed to become a mid-cap bank while others remain small caps. The financial services comprising 146 companies have a long tail of small caps comprising NBFC, micro finance, asset management, brokerages, holding companies, etc

The other major cohort is chemicals and pharmaceuticals with nearly 230 companies. The chemical space has 130 companies with only 10% of them in the mid cap and above category. This space has been under watch for expensive IPOs and significant price erosion in recent past. It’s still a hard time for investors to distinguish between speciality and non-speciality after the IPO boom.

What is the point we are trying to make here? The point here is that only very few companies have graduated from small caps to mid caps and then mid caps to large caps over a period of time and the hype that small cap rally creates with multi bagger stories have not proved to be worthy. Rather, most of them are low quality businesses and trap investors during the boom.

(To avoid basic traps like low quality businesses, you can use our stock screener to get a list of companies by category, analyse them on various financial parameters and create your own watchlist)

Now let us move to more stock-specific examples to look at where you may risk ending with a company with a low quality business.

Why Amber isn’t the next Dixon?

Electronics manufacturing sector is another sector on fire now with a bunch of new listings. Dixon Tech’s rally and i-phone manufacturing story has created a hype around this sector. Barring Dixon, there is no listed player with scale. Being a capital plus labour intensive sector, can it create wealth or go the textile way? Ultimately qualitative growth is key to shareholder returns. This study of two players from this space may throw some light on growth Vs quality of growth.

It was in the 2017-2018 mid and small cap bull run that Dixon Technologies and Amber Enterprises came out with their IPO. Over the years, Dixon has not only grown 5 times in revenue in 5 years, but it has also generated superior RoCE of 25-30% with healthy cash flows and a NET debt free balance sheet at the end of FY23.

While Amber too grew 3 times in revenue, it couldn’t deliver on the quality of growth as Dixon did, while its debt went up 6 times.

Dixon’s stock is up 12.5 times since IPO while Amber is up 2.5 times.

What set these stocks apart was their capital efficiency (Refer DuPont analysis in the article). While both are low margin business, Dixon exhibited phenomenal capital efficiency by churning its assets up to 7.5 times Vs 2.5 times done by Amber to generate superior RoCE.

The infrastructure rout

You would be surprised if we say that there are less than 5 infrastructure companies now (barring Adani) in top 250 companies by market Cap.

L&T at 19th position, Adani ports at 30th and GMR Airports at 210th position are the three major ones.

But this sector was the poster boy of the 2008 bull market with Punj Lloyd, IVRCL, Gammon, Reliance Infra, JP Associates, HCC, etc. stealing the show and then IRB Infra, Va-tech Wabag, Sadbhav, Gayatri Projects, Ashoka Buildcon, Dilip Buildcon, etc in 2017.

But most of these went into oblivion. Let’s pause a bit and think why! It is to do with the fundamental nature of running a business in this space – which is aggressive bidding for orders, taking huge debt in balance sheet, and eventually landing in arbitration claims. They are certainly not recipes for generating long-term returns for shareholders!

L&T is the lone major survivor in this space, thanks to its competency and a visionary management for making its IT Services business big enough to contribute to half of its current market Cap. Beyond that, there are few long-term survivors like KNR Construction and Ahluwalia Contracts (that only does short term civil contracts) with qualitative growth. The rest fell by the way side.

How to judge low quality businesses?

The best guide to judging companies to stay clear of low quality businesses, to my mind, is the classification of companies by Warren Buffett as Great, Good and Gruesome with clear definition for each category.

- Great companies have all the hallmark qualities such as consistent growth, strong competitive advantage, capable management, good track record of capital allocation, high return on capital and caring for minority shareholders.

- Early-stage companies may lack these qualities, but they should start with good management, strong competitive advantage, and minority shareholder friendly practices.

- Gruesome companies stand at the other extreme with compromising qualities. A detailed insight into this is available in the 13th wealth creation study put forward by MOSL.

So, companies that fall outside of Great and Good categories can be called as “low quality” companies or companies with low quality businesses. The only solution to avoid such traps is NOT to jump impulsively into stories. Always judge companies based on key characteristics that are required for them to deliver qualitative growth. It takes a while to understand about any company.

The infrastructure stocks that we discussed above are classic examples of ‘Gruesome’ or low quality businesses. You may also find a lot of them in categories that we discussed above including auto ancillaries, financials, textiles, chemicals, etc.

The securities quoted are for illustration purposes only and are not recommendatory.