Warren Buffett never fails to recommend it and 90% of US fund managers struggle to beat it. If you’re wondering what this miracle investment is, it’s the US S&P 500 index. Indian investors will soon have the opportunity to buy this US benchmark locally with Motilal Oswal AMC launching an open-end index fund replicating it – The Motilal Oswal S&P 500. The fund will carry a total expense ratio of 1% under the regular plan and 0.5% under the direct plan, with minimum investments of Rs 500.

Warren Buffett never fails to recommend it and 90% of US fund managers struggle to beat it. If you’re wondering what this miracle investment is, it’s the US S&P 500 index. Indian investors will soon have the opportunity to buy this US benchmark locally with Motilal Oswal AMC launching an open-end index fund replicating it – The Motilal Oswal S&P 500. The fund will carry a total expense ratio of 1% under the regular plan and 0.5% under the direct plan, with minimum investments of Rs 500.

The NFO opens on April 15, 2020. Should you bite?

What’s in it?

The S&P 500 index is a free-float market cap-weighted index made up of the 500 most liquid large-cap names in the US market. The index covers 82% of US market capitalisation. Nearly $10 trillion of assets globally are benchmarked to it, with index funds valued at $3.4 trillion tracking it. Compared to the Nasdaq 100 or Dow Jones Industrial Average, the S&P 500 offers a much wider coverage of the US market, representing both industrial and technology names across eleven sectors. The index currently features 505 stocks with a total market cap of $22,569 billion.

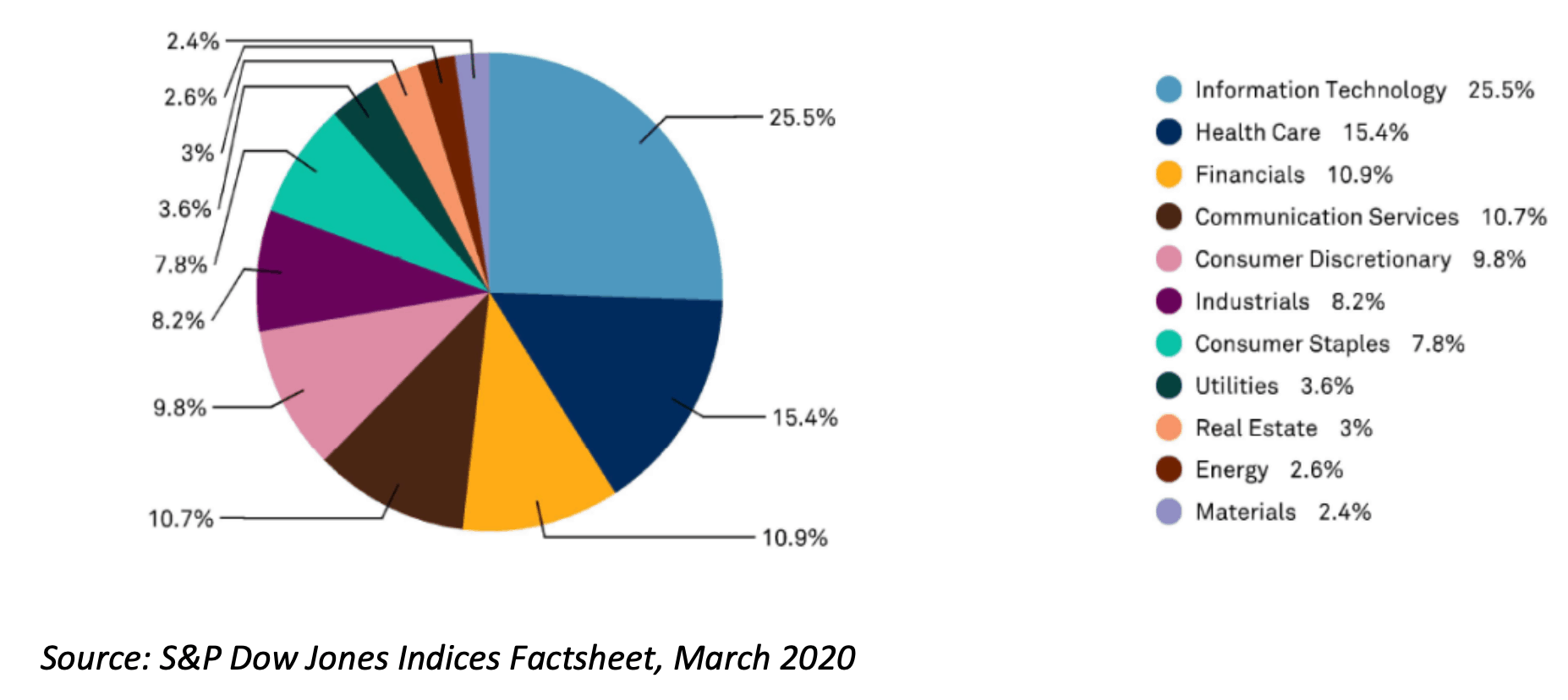

Compared to Indian indices such as the Nifty50 or even the Nifty500, the US S&P 500 is a more diversified index. Its top sector – Information Technology – is at 25.5%, followed by healthcare (15.4%), financials (11%), communication services (10.7%) and consumer discretionary (9.8%). Its top ten holdings making up a 25.4% weight. India’s Nifty500 features a bigger weight of 32% weight to its top sector financial services and top ten stocks take up a 44% weight.

62 thoughts on “Should you invest in the Motilal Oswal S&P 500 Index Fund?”

How will this be taxed as?

Hello sir,

Taxation is the same as for debt funds – capital gain on holding 3 years and above is long term, and taxed at 20% with indexation. Less than 3 years is at your slab rate.

Thanks,

Bhavana

I was thinking confused wheater to invest or not on Motilal Oswal S&P 500 Index Fund, but now I am clear what should I do

Thank you so much

Well written !!!

The risk i see with Index are, they are getting skewed to particular sector now a days. Nifty having more Banks and Financials. S&P 500 having more Internet and Tech.

Valuable insights, you would not recommend a lump sump investment now given US markets are down. My outlook is long term 10+ years.

We have mentioned valuations are not that cheap and said if you are investing lumpsum follow up with SIPs. thanks, Vidya

Yes we would not. Valuations are expensive and earnings outlook negative

Hi, great well written, researched and interesting article. The article is also thought provoking and push people to think through.

Thank you!

Tracking Error

When i look at Index Fund, the utmost important aspect which i have to look for is Tracking Error.

I have copied and pasted what they defined in their SID “The Fund Manager would not be able to invest the entire corpus exactly in the same proportion as in the underlying index due to certain factors such as the fees and expenses of the Scheme, corporate actions, cash balance and changes to the underlying index and regulatory restrictions, lack of liquidity which may result in Tracking Error. Hence it may affect AMC’s ability to achieve close correlation with the underlying index of the Scheme. The Scheme’s returns may, therefore, deviate from its underlying index. “Tracking Error” is defined as the standard deviation of the difference between daily returns of the underlying index and the NAV of the Scheme. The Fund Manager would monitor the Tracking Error of the Scheme on an ongoing basis and would seek to minimize the Tracking Error to the maximum extent possible. There can be no assurance or guarantee that the Scheme will achieve any particular level of Tracking Error relative to the performance of the Underlying Index.”

What is your view on the same.

These are standard disclaimers and could well transpire. We don’t paticularly have a view on it. thanks, Vidya

Good write-up !

1. How do we hedge against USD-INR appreciation and depreciation for this investment if i invest a lumusm amount and wait for 3 years ?

2. For NRI’s, is it good idea to invest in USD in one lumsum amount to gain thru currency appreciation of say 2-2.5% YoY ?

Thanks

The idea of the fund is to diversify to US market and long-term trend of rupee depreciation against the dollar. This fund is not a play on currency arbitrage not to hedge currency fluctuation. If so, currecy futures is the way to go. We do not have expertise on it. We also do not have expertise to state at what currency levels to invest. We have given in the article about the US market valuations (equity fundamentals) and whether it is cheap or expensive and how to invest thanks, Vidya

I have index only portfolio of Nitfy 50 and Nifty Next 50 Index funds with allocation of 80%:20% for my equity portion of the portfolio, I do have Parag parikh LT fund and waiting for the exit load to complete and move to this Index fund MO S&P 500 index fund. Can i have 15% of allocation to MO fund in this overall portfolio, Please share your views

Hello sir,

This is a specific query on our recommendation which we’d prefer to avoid answering on this forum, as it is meant more as a discussion forum. If you are a full subscriber to PrimeInvestor, please write to us with your question on our recommendations and we’ll help.

Thanks,

Bhavana

I believe the Indian Index funds are treated as Equity funds for taxation. When the same kind of index funds track US index. comprising of all equity, why it should be given debt funds tax treatment? Is there any rationale behind such taxation?

Hello sir,

That’s a question to ask the government 🙂

The taxation rule is that funds that invest 65% in domestic stocks alone get equity-type taxation. Anything else is debt taxation, which is why FOFs that invest in equity funds are taxed like debt as it is not investing in stocks. International stocks are obviously not domestic, so they don’t have equity taxation either.

Thanks,

Bhavana

Comments are closed.