Warren Buffett never fails to recommend it and 90% of US fund managers struggle to beat it. If you’re wondering what this miracle investment is, it’s the US S&P 500 index. Indian investors will soon have the opportunity to buy this US benchmark locally with Motilal Oswal AMC launching an open-end index fund replicating it – The Motilal Oswal S&P 500. The fund will carry a total expense ratio of 1% under the regular plan and 0.5% under the direct plan, with minimum investments of Rs 500.

Warren Buffett never fails to recommend it and 90% of US fund managers struggle to beat it. If you’re wondering what this miracle investment is, it’s the US S&P 500 index. Indian investors will soon have the opportunity to buy this US benchmark locally with Motilal Oswal AMC launching an open-end index fund replicating it – The Motilal Oswal S&P 500. The fund will carry a total expense ratio of 1% under the regular plan and 0.5% under the direct plan, with minimum investments of Rs 500.

The NFO opens on April 15, 2020. Should you bite?

What’s in it?

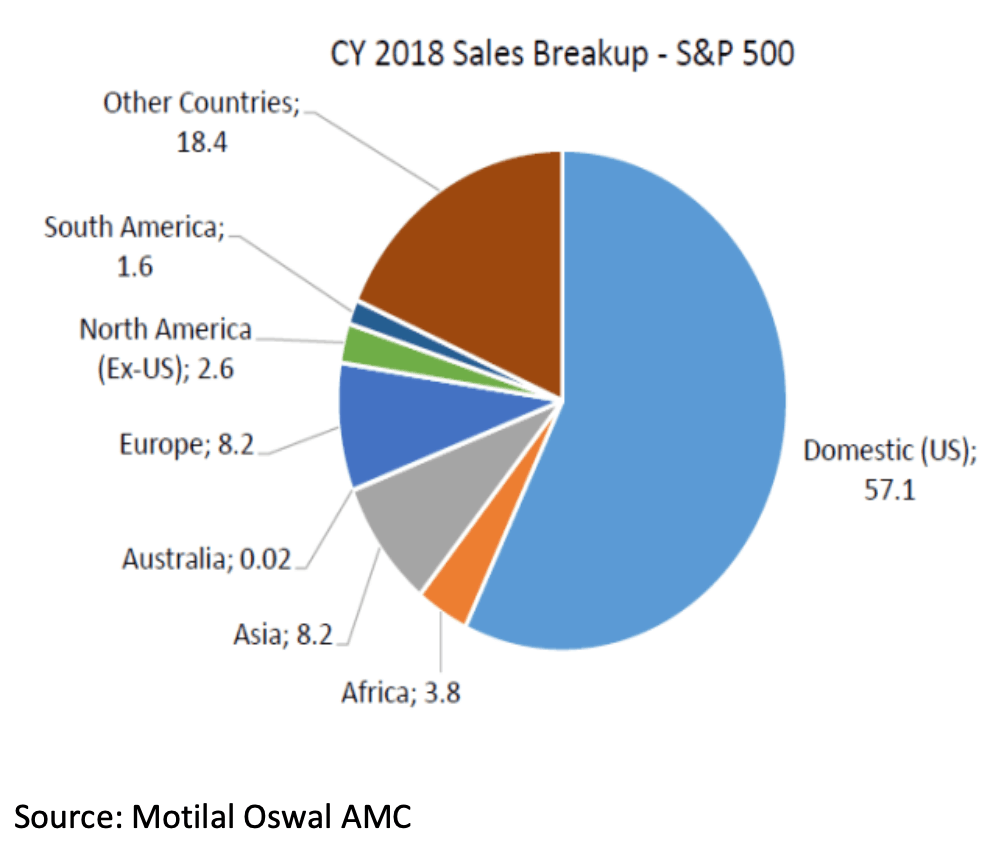

The S&P 500 index is a free-float market cap-weighted index made up of the 500 most liquid large-cap names in the US market. The index covers 82% of US market capitalisation. Nearly $10 trillion of assets globally are benchmarked to it, with index funds valued at $3.4 trillion tracking it. Compared to the Nasdaq 100 or Dow Jones Industrial Average, the S&P 500 offers a much wider coverage of the US market, representing both industrial and technology names across eleven sectors. The index currently features 505 stocks with a total market cap of $22,569 billion.

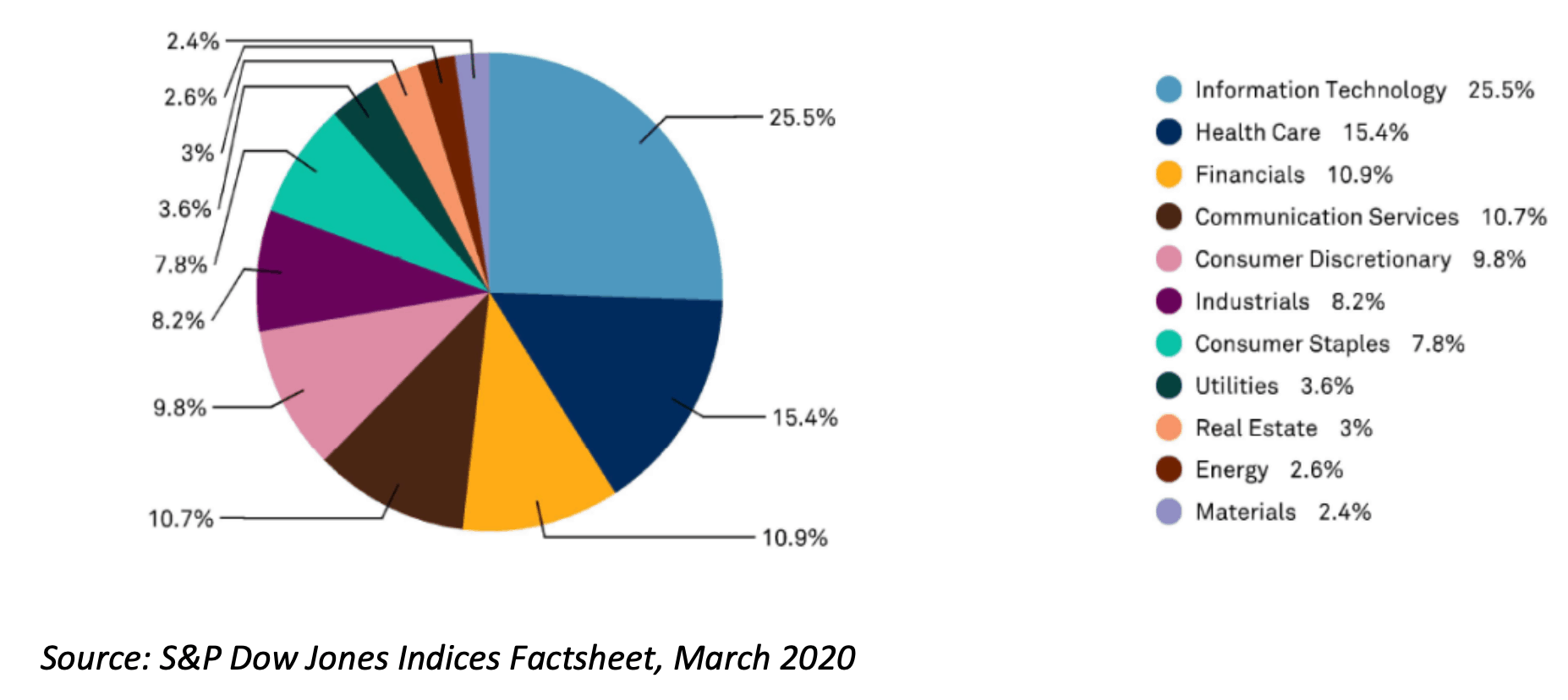

Compared to Indian indices such as the Nifty50 or even the Nifty500, the US S&P 500 is a more diversified index. Its top sector – Information Technology – is at 25.5%, followed by healthcare (15.4%), financials (11%), communication services (10.7%) and consumer discretionary (9.8%). Its top ten holdings making up a 25.4% weight. India’s Nifty500 features a bigger weight of 32% weight to its top sector financial services and top ten stocks take up a 44% weight.

62 thoughts on “Should you invest in the Motilal Oswal S&P 500 Index Fund?”

What is difference between index fund , fund of funds and etf . For nifty fifty ,nifty next fifty , nasdaq 100 and S and P 500 which one is a better option index fund or fof or etf and which are the schemes available for each one of them ? Please help me understand. .

Hello sir,

You can refer to Prime Funds and Prime ETFs for recommendations on which index fund/ETFs to buy. If you want a portfolio built with passive funds, you can check the Passive Portfolio in Prime Portfolios. In these, we’ve picked funds and ETFs after considering tracking error, volumes, expenses etc.

Thanks,

Bhavana

What if one has Franklin India feeder – Franklin US Opportunities Fund in the Portfolio. Should one replace with MOSL S&P 500 or continue with Franklin or have both? (especially when expense ratios are also more or less same). Thanks!

The exepnse ratio is marginally higher for the Franklin fund. It will entirely be your call on whether you want a pasive approach or active approach to investing. If you ask me whether you should go with index funds or with active funds in India, it is a slightly easier answer as we have enough active funds that can still beat the inddex. In the US, active funds that beat the index are fewer. Also, while 5 year returns look alike for the index and the Franklin fund, the call should be about cost and whether you prefer a passive strategy.

thanks Vidya

Maam, Can we wait to get more clarity on the expense ratio, tracking error etc which is not known in the NFO period especially when one is invested in say PPFAS ?

If there is something you should wait for, it should be your view on whether S&P 500 is expensive now and needs to correct or it is ok. Expense ratio won’t change much except with AUM. As for tracking error, it will be tough to figure given that the index will be in dollar and the fund in INR. We won’t have running rupee converted index value (Unless somebody provides it). So the returns over time will always vary (in favour of the indian investment, if rupee depreciates). Thanks, Vidya

Please explain if S&P 500 INDEX FUND will be a better choice than ICICI US BLUECHIP or Nippon us opportunities fund.

That’s hard to predict. But with the S&P 500 fund you won’t have to worry about fund manager changes, or the stock selection outperforming the market. The majority of active US funds have lagged S&P 500 in the last ten years.

Will the MO S&P 500 Index Fund be treated like a debt fund for the capital gains taxation purpose since the constituent stocks are all listed in the US ?

Yes it will be treated like a debt fund for taxation.

Thanks for this wonderful article. I remember that I got into to Mutual funds around 2007 by reading your articles.

It’s there any Indian fund which tracks Nasdaq 100?

Thanks

Yes Motilal Oswal also runs a fund of funds that tracks Nasdaq 100.

Is this FoF or direct Index fund?

It is an index fund. Vidya

Article is well researched, written, thanks Aarati!

One question is, isn’t a 0.5% expense ratio high for an index fund?

Dear Prime

I wud appreciate if u cud also include tax treatment of this ETF in India for that wud make a difference in our investment decision.

This is an open end index fund not ETF. It will be treated like a debt fund for taxation with LTCG after 3 years with indexation and STCG at your slab rate before 3 years.

Dont you think this is a huge differentiator for Indian investors when it comes to the cost of investing. If you are investing in the Indian Index Fund (ETF or Index Mutual Funds), the taxation is as per the current equity taxation rules.

However, if opted this fund, because of your taxation, you may end up in adding more expenses in the form of tax.

Kindly advise.

So debt funds don’t have equity-like tax. What is their role in the portfolio? Diversification and hedge? Same applies here. It is not either or. thanks, Vidya

Yes it is somewhat high. But as there’s no local alternate investing still makes sense.

Any index not easy to contruct has and remember the cost they have to incur in currency too. Many indian index funds have more expense ratio than this. Vidya

Yes, but it’s an new index fund which reflects S&P 500 but with increase in AUM, the expense ratio will get reduced in future as people tends to believe for diversification purpose mainly. Also, people diversify by only 10 to 15%.

Very good detailed write up. If an investor already have about 12% US exposure through fund like PPLTE, does this new index fund required? Thanks for the above article.

Good question. PPLTEF gives you exposure to US companies but hedges against currency moves. So you get just one of the benefits of US investing. We suggest you add say 5% in this fund.

Nice review. Should we wait to see the performance of this fund for few quarters and then decide?

Hello Sir, thanks. It’s an index fund. So you don’t particularly need to unless youa re worried about whether it is the right time to enter the US. thanks, Vidya

Yes you could. But make sure you don’t wholly miss the market fall!

Hi

Interesting review and the conclusion is very clear for an investor who has no exposure to global equities.

However, if one is already invested (along with a running SIPs) in Motilal Oswal Nasdaq 100 as well as Edelweiss US technology Equity FOF – then what? What makes more sense, should one of them be replaced with S&P 500 OR no action to be taken OR this one to be added without changing asset allocation?

Thanks

Thanks. This is like choosing between a sector fund and a diversified equity fund. The latter offers lower return potential but with far lower risk..Would suggest replacing Edelweiss Tech fund with S&P 500.

Comments are closed.