Your stock portfolio would typically have one of these two approaches to investing: a concentrated portfolio approach (8-10 stocks) or a more diversified one (15-20). Consequently, a portfolio may have 5% to 12% allocation to a single stock depending on the portfolio size.

There is a lot of academic research material available on diversified vs. concentrated portfolio and how much diversification should one consider in a portfolio. Robert G Hagstrom in his book “Warren Buffett Portfolio” has given clear insights on concentrated vs diversified portfolios and beyond what size the benefit of diversification begins to fade away

You can also read the article by Aarati Krishnan on how to build a stock portfolio

Whatever be your approach, when it comes to the actual performance of your portfolio, you just need to get two things right to hold a winning stock portfolio.

They are:

- Riding the winners

- Cutting the losers

But this is easier said than done. In reality, it is the most difficult thing to practice. This is because stock market reactions, stock specific events and behavioural biases push investors to get rid of winners early and hold on to losers until it is too late.

The best results of this approach can be seen in stock portfolios of successful investors where one stock or few stocks form significant share of their portfolio over a longer period of time. Please note that this does not mean that they took concentrated exposures. It became concentrated over time.

This article will be an attempt to help you understand how to hold a winning portfolio – one where you manage to hold on to the winners while cutting down on the losers without dela

Winning stock portfolio: Riding the winners

This is the most critical aspect for a portfolio to outperform as only a few stocks in many portfolios typically deliver unexpectedly high returns, while a good number go wrong. While you may identify good stocks, the question is always about how long to hold on to them.

How long to ride the winners?

The most renowned practitioner of long-term investing, Warren Buffett, once said “our favourite holding period is forever”.

According to him, so long as an investment in a company is doing well, backed by growth along with quality of growth, the idea should be to hold them in the portfolio for a long period of time. Quality of growth refers to the ability of a company to grow its earnings with high capital efficiency (RoCE) for an extended period of time.

Let us take a random portfolio (concentrated) of 8 stocks and see how it performs if we allow winners to ride. Assume that higher risk/ lower capitalisation stocks have been given lower weights in the portfolio.

In the context of this discussion, we are considering a rising market scenario, which has been the case most of the time in our stock market. The period considered is only 3 years – just for the sake of illustrating – although your focus should be a much longer term.

In the illustration above you can see how winners can make a big change to the portfolio! Stock A with 15% initial allocation grew to 25% at the end of 3 years as it delivered 3.4 times. Stock Z, on the other hand reduced from 10% allocation to 3% as it did not deliver. The underperformers automatically end up with lower weights as the portfolio grows.

Quite often, we see this “riding the winners” strategy playing out well in individual investors’ portfolio than in fund portfolios. This is either due to a concentrated approach or because individual investors allow the stocks to gain concentration with time, without trimming them. On the other hand, fund portfolios generally start with very low allocation or keep trimming their allocation in a stock beyond a certain point. Mutual funds are also constrained by the fact they have a cap on individual stock holding.

In Rakesh Jhunjhunwala’s portfolio as of 31st December 2021, post the stellar listing of Star Health and Metro Brands, these two stocks along with Titan formed 66% of his portfolio. In the case of renowned investor Warren Buffett’s, Apple formed 47% of his portfolio after quadrupling in 4 years.

But did they start with such high allocation to those stocks? NO. It is the approach of “riding the winners” that allowed such stocks to form a disproportionate share of their portfolios.

But sitting and watching such huge profits, when there is a risk of them evaporating in a correction, may not be easy. It is important to take a balanced view. If the winners have become far better companies than in the beginning with significant tailwinds (positive changes in industry/ business/ management) in their favour, it may still be worthy of retaining them at higher allocation than in the beginning. But what if you bought a stock at 20/30 PE and it is trading at 100 PE now?

PE re-rating is a definite case with all big winners and in such a case it merits trimming the position as well. If it is a commodity stock, it requires even more attention in terms of knowing the commodity cycle. Consequently, laying an upper cap of 15-25% of the portfolio versus original allocation of 5-12% (depending on portfolio size) can help to trim some positions while still riding them. This is a better approach than having absolute return targets alone.

Motilal Oswal 13th wealth creation study that discusses about Great, Good & Gruesome businesses may help you get an idea on how to assess if a good company is getting better. This, in conjunction with other wealth creation studies such as the 17th WC study on Economic Moat, 19th WC study on Growth and 24th WC study on Management Integrity can provide significant insights to assess improvement of companies. You can get all wealth creation studies in the below link: Motilal Oswal Private Wealth (motilaloswalpwm.com)

Of-course such higher allocation may not be acceptable from a diversification and risk-management point of view. But it is a trade-off that an investor has to make.

Charlie Munger once remarked;

“The academics have done a terrible disservice to intelligent investors by glorifying the idea of diversification. Because I just think the whole concept is literally almost insane. It emphasises feeling good about not having your investment results depart very much from average investment results”.

When it comes to decision making, here’s an example to highlight. Rakesh Jhunjhunwala, at one point of time, owned 10% of equity shares of TITAN which he brought down over a period of time to 5% now. Still the stock is 33% of his portfolio. Being an investor who respects valuations, he trimmed his positions in last few years, but the stock continued to surprise. As it gained size, the narrative only got better in the market leading to acceptance by a large pool of investors.

So, starting with a diversified portfolio of stocks with disciplined allocation and allowing the winners to ride the portfolio could work in your favour.

Getting rid of behavioural biases

Having pointed out the benefit of “riding the winners” and sticking to an allocation plan to ride them, let’s get into the toughest part of dealing with it, the behavioural biases. Market corrections and the uncertainties or some random chain of events can force investors to get out of the winners. Let us look at some of those behavioural biases.

#1 Risk aversion/loss aversion

What if you are sitting at 10X returns in a stock and it suddenly falls 30% ? This is where the real test happens in ‘riding the winners’. And surviving such tests makes a big difference. Many studies suggest that 95% of investors exit due to risk aversion/loss aversion and only 5% hang around for long. Many of the top wealth creators had gone through phases of significant corrections of 30-60% during their journey - be it Infosys or ICICI Bank or Bajaj finance or Larsen & Toubro. Those who held through such periods, built wealth.

#2 Paying attention to price movements

Investors have a habit of frequently checking their portfolios. The more frequently you check, the more you will find the urge to react to the ups and downs of the market.

Paying more attention to earnings growth, future prospects and valuation of companies than market price movements can help ride the winners better. This may be the reason why the biggest wealth creators from stocks are Promoters followed by HNI investors and ESOP holders while stock analysts come at the end (as an analyst I am forced to deal with market noises and new ideas that can tempt me to react to the ups and downs of the market).

ESOP holders may not be in touch with markets even as trust and confidence in a brand that they are familiar with, helps them overcome the urge to react to price fluctuations.

All put together, riding the winners calls for multiple qualities in an investor from understanding the businesses and valuations to surviving adverse circumstances and staying away from market noises through several market cycles. It is difficult, but there is no short cut to achieve superior returns. The next best option is to settle for market returns.

Winning stock portfolio: Cutting down on losers

When should you exit a stock that is underperforming? This is undoubtedly the next most difficult part in portfolio management. While you may pick every stock with the intention of generating returns, a few calls will definitely go wrong. It is important to have a plan to cut down such losers.

Let’s take the earlier illustration again. How much is the loss on the biggest loser (Stock Z) as a % of the portfolio? It is 2% on the portfolio value at the end of 3 years. But if you look at the individual stock it is 40% down from its cost! We tend to look at this huge absolute loss (loss aversion) and that prevents us from taking any further decision on the stock, leaving it to drag the portfolio. But, this can only lead to bad end results, as explained further.

When the original investment thesis on a stock is no longer valid or things start going downhill for a company there is little point in sticking to a stock. The steady decline in a stock price may be due to adverse government policies, corporate actions, growth disappointment, increasing competition, faulty capital allocation decisions, change in business cycles, cash flow issues, scams and so on. Acquisitions and diversifications are also other key factors to watch out for. It is important to understand the impact of such events:

- Whether such events are material enough to alter the long-term thesis of the company that you held to.

- Or whether they are temporary issues in the business cycle or industry that a company can tide over.

Emotional decision to hold on to losers can lead to permanent loss of capital. In the above illustration, the loser stock might have given warning sign earlier itself when the absolute loss was only 20% or 30%.

We have seen instances of investors losing 50%-90% of their capital starting from the tech boom in 2000 to the infra/capex boom in 2008 and more recently the new tech boom. Let’s take some examples of such boom and bust.

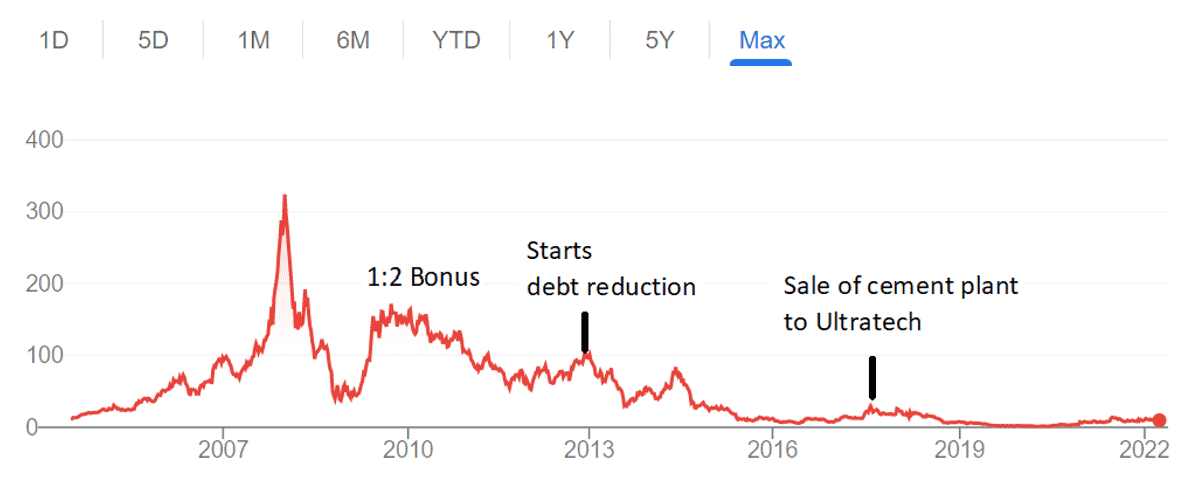

Below is the chart of JP Associates, once considered an infrastructure behemoth. From being a construction company, it diversified into power, real estate, BOT projects and cement, all on debt. Infrastructure was a fascinating story post Y2K. The stock of this company was also fancied then. While it did crash like most other stocks in 2008, the stock rallied a good bit as the 1:2 bonus issue in 2009 made investors believe in the story and stay put (may be an idea borrowed from the bonus issue of Reliance Power! Read our article on what bonus issue really means here).

Since then, the debt reduction plan in 2013 and finally the sale of cement plants saw relief rallies in the stock. If investors blindly trusted the short market rallies and held or even averaged, they would have lost more ultimately. As the company reduced debt and market cheered, only the sceptics knew that there was little value left in the assets as the valuable ones were sold. The debt reduction distracted the vital fact that what was left in the company were assets that could not be sold! So, the future business was at risk!

Here’s another example: Below is the chart of HCC (Hindustan Construction), the architect of Bandra-Worli sea link, often referred to as an engineering marvel. Here too, when a debt-ridden company issues bonus shares, investors hang around with hopes But things went downhill as its mega luxury real estate project, Lavasa, ended badly.

Being a new entrant in to stock market in 2007, I was also fascinated by the infrastructure stories until a senior investor asked me two questions:

- what is the probability that the order book will get executed and on time?

- what is the guarantee that they will receive money upon execution of all orders?

These exactly turned out to be the pain points for many infrastructure companies later on.

Unlike DHFL or Suzlon or Yes Bank that lost 90% of value in just a year, the stocks we mentioned earlier took longer time to wipe out investors’ wealth. But the end result was the same.

The above examples are instances of stock calls going fundamentally wrong. Even if your pick was not a bad one, it now makes sense to ponder over the quantum of losses. If you lose 50% or more on a stock, then you need to make 100% returns to recoup the capital itself (Rs.100 to Rs.50 is 50% while back to Rs. 100 requires 100% gain). This emphasises the importance of taking a review of losers as early as possible.

But the good news is that in a portfolio approach, the pain is much lower as a it still offers significant leeway to cut the loser and re-invest the money somewhere else.

Sometimes, your portfolio itself will show which ones need to be reviewed to pare exposures. You may see in the illustration above that each of those losing stocks have just become 3-5% of the portfolio while the overall portfolio has doubled. So, the tail often reflects the ones to be taken for review to cut down exposure.

Having pointed out the importance of cutting down on losers, what may stand against doing it are few behavioural biases as follows:

- Sunk cost fallacy: It describes our tendency to follow through on an endeavour if we have already invested time, effort, or money into it. In the case of a poorly performing stock, since a lot of money is invested already, we may have tendency to put more money into it and average down the cost.

- Loss Aversion: It is a cognitive bias, which explains why individuals feel the pain of loss twice as intensively than the equivalent pleasure of gain. As a result, we may have a tendency to hold on to loss making investments rather than booking the losses. Over a period of time, this may lead to a long tail of loss-making stocks that act as a drag on returns.

- Confirmation bias: Confirmation bias is the tendency to search for, interpret, favour, and recall information in a way that confirms or supports one's prior beliefs or values. It causes us to only take the information that is consistent with your theory and discard everything that does not align with it and finally holding on to loss making investments. In the age of social media, you will find enough information that may support your bias.

Cutting losers requires you to first get rid of the loss aversion bias taking into account any change in your thesis of the company. While riding the winners will give upside to the portfolio, cutting the losers is critical to get rid of unproductive investments that may be a drag on returns.

As famous investor and hedge fund manager George Soros once said; "It's not whether you're right or wrong, but how much money you make when you're right and how much you lose when you're wrong”.